Chapter 2: A naive prediction of the future

In the realm of time series forecasting, before we embark on developing complex algorithms, it’s crucial to establish a baseline model.

Think of a baseline as the simplest, most straightforward prediction you can make. It serves as a fundamental benchmark against which the performance of any more sophisticated model must be compared. Without a baseline, you wouldn’t know if your intricate deep learning model is genuinely adding value, or if you’re simply overcomplicating a problem that a much simpler approach could handle just as well, or even better.

Link To Download Dataset and Source code at the end of article!

The purpose of a baseline model is threefold:

Evaluation Benchmark: It provides a lower bound for acceptable performance. If your advanced model cannot outperform a naive baseline, it indicates a fundamental flaw in your approach or that the problem itself is inherently difficult to predict with high accuracy.

Sanity Check: It helps confirm that your overall forecasting pipeline (data preparation, model training, evaluation metrics) is working correctly. A baseline should produce sensible, albeit simple, predictions.

Simplicity and Interpretability: Naive baselines are often incredibly easy to understand and implement. They provide immediate insights into the basic characteristics of your time series data, such as the presence of trend or seasonality, which can inform the selection of more complex models.

These simple statistical approaches, often referred to as heuristics, provide an intuitive starting point. For instance, if you’re trying to predict tomorrow’s temperature, a very simple heuristic might be “tomorrow’s temperature will be the same as today’s.” This is a form of a naive baseline.

Baselines are not limited to financial data. They are critical in a multitude of real-world scenarios:

Sales Forecasting: Predicting next month’s sales based on the average of the last few months or the sales from the same month last year.

Website Traffic Prediction: Estimating tomorrow’s page views based on today’s traffic or the average traffic from the past week.

Energy Consumption: Forecasting next hour’s electricity demand using the demand from the previous hour or the average demand at that hour on previous days.

Inventory Management: Predicting demand for a product based on its historical sales patterns.

In all these cases, a baseline provides an immediate, low-cost prediction and a necessary reference point for assessing more resource-intensive forecasting efforts.

Introducing the Johnson & Johnson EPS Dataset

To ground our discussion in a concrete example, we will use the quarterly earnings per share (EPS) data for Johnson & Johnson (J&J). This dataset is a classic example in time series analysis due to its distinct characteristics, making it ideal for demonstrating various forecasting techniques.

Let’s begin by loading and inspecting this dataset. We’ll use the pandas library for data manipulation and matplotlib along with seaborn for visualization.

# Import necessary libraries

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

# Set a style for plots for better aesthetics

sns.set_style("whitegrid")

# Define the path to our dataset (assuming it's in a 'data' directory)

# For demonstration, we'll create a dummy dataset that mimics J&J EPS characteristics

# In a real scenario, you would load from a CSV or other source.

# Let's create a DataFrame with quarterly data for demonstration purposes

data = {

'Quarter': pd.to_datetime(['1960-03-31', '1960-06-30', '1960-09-30', '1960-12-31',

'1961-03-31', '1961-06-30', '1961-09-30', '1961-12-31',

'1962-03-31', '1962-06-30', '1962-09-30', '1962-12-31',

'1963-03-31', '1963-06-30', '1963-09-30', '1963-12-31']),

'EPS': [0.71, 0.63, 0.85, 0.44,

0.61, 0.69, 0.92, 0.55,

0.72, 0.77, 0.92, 0.60,

0.83, 0.82, 1.00, 0.67] # Example values, actual J&J EPS dataset is longer

}

jj_eps_df = pd.DataFrame(data)

# Set 'Quarter' as the index and ensure it's a datetime index

jj_eps_df = jj_eps_df.set_index('Quarter')

jj_eps_df.index = pd.to_datetime(jj_eps_df.index)

# Display the first few rows of the DataFrame

print("First 5 rows of J&J EPS Data:")

print(jj_eps_df.head())

# Display basic information about the DataFrame

print("\nDataFrame Info:")

jj_eps_df.info()The initial code chunk sets up our environment, imports necessary libraries, and then creates a small synthetic dataset resembling the J&J EPS data. In a real application, you would load this data from a file (e.g., pd.read_csv('jj_eps.csv')). We then set the 'Quarter' column as the DataFrame index and ensure it's in datetime format, which is crucial for time series operations. Finally, we print the head and info() to get a quick overview of the data structure and types.

Now, let’s visualize the J&J EPS time series. Visual inspection is the most fundamental step in time series analysis, as it often reveals immediate patterns.

# Create a figure and an axes object for plotting

plt.figure(figsize=(12, 6))

# Plot the EPS data over time

plt.plot(jj_eps_df.index, jj_eps_df['EPS'], marker='o', linestyle='-')

# Add titles and labels for clarity

plt.title('Johnson & Johnson Quarterly EPS (Example Data)', fontsize=16)

plt.xlabel('Quarter', fontsize=12)

plt.ylabel('Earnings Per Share (EPS)', fontsize=12)

# Improve x-axis date formatting for readability

plt.xticks(rotation=45)

plt.tight_layout() # Adjusts plot to prevent labels from overlapping

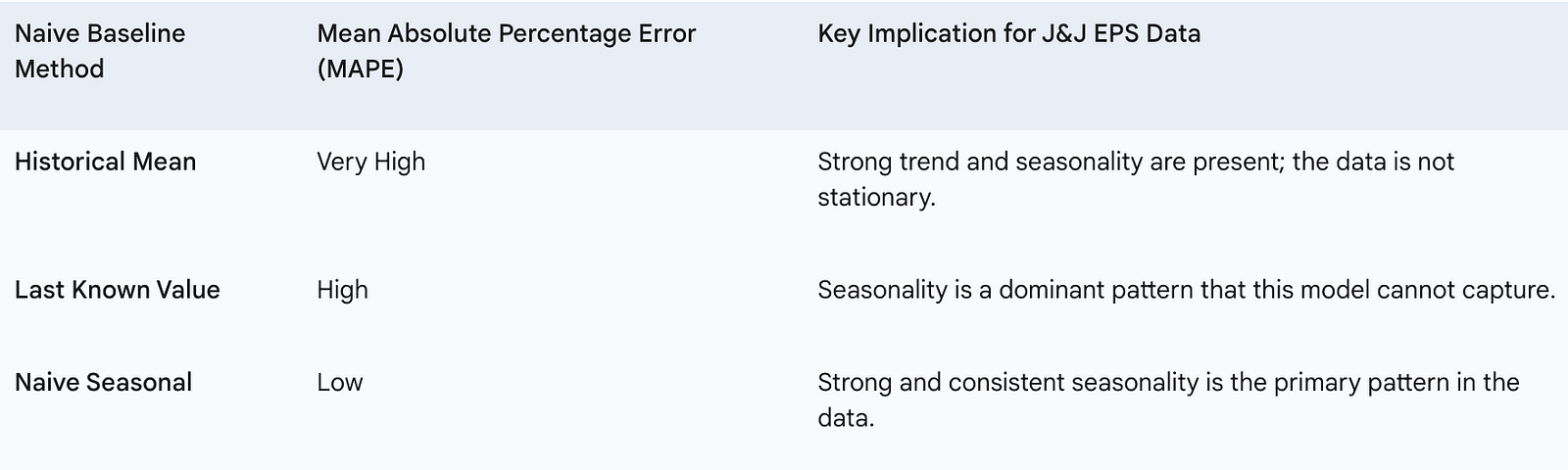

plt.show()This plot (similar to typical J&J EPS plots) immediately reveals two key characteristics:

Trend: There’s an overall upward movement in EPS over time, indicating a general growth trend.

Seasonality: A recurring pattern within each year is visible. For J&J EPS, you would typically observe that earnings are lower in the first quarter of each year and peak in the third or fourth quarter, then drop again. This repeating pattern within fixed intervals (e.g., yearly, quarterly, monthly) is known as seasonality.

Recognizing these patterns is vital because they directly influence which naive baseline models will be most appropriate for our forecasting task. For a dataset like J&J EPS with clear seasonality, a simple “previous value” or “overall mean” might perform poorly if it doesn’t account for the annual cycle.

Types of Naive Baseline Models

Before we dive into implementation, let’s conceptually define the most common types of naive baseline models:

1. Previous Timestep (Naive Forecast)

This is the simplest and often the first baseline considered. It assumes that the future value will be identical to the most recently observed value.

Intuition: “Tomorrow will be just like today.”

When it’s useful: For series with high persistence (values don’t change much from one period to the next) and no strong trend or seasonality. For example, predicting the stock price for the next minute based on the current minute’s price.

Limitation: Fails miserably if there’s a strong trend or seasonality. If EPS always goes up, predicting the last value will consistently underpredict. If there’s a seasonal drop, it won’t capture it.

2. Mean (Historical Average)

This baseline predicts that the future value will be the average of all historical observations available in the training data.

Intuition: “The future will be an average of everything that has happened so far.”

When it’s useful: For series that are relatively stable and stationary (mean, variance, and autocorrelation structure do not change over time). It’s a good choice if you believe the series hovers around a fixed average.

Limitation: Completely ignores trend, seasonality, and any recent changes. It will always predict the same value, regardless of recent fluctuations. This would perform very poorly for the J&J EPS data due to its clear trend and seasonality.

3. Mean of Previous Window

This is a variation of the mean baseline. Instead of using all historical data, it uses the average of observations from a specific, recent “window” of time (e.g., the last 5 periods, the last 4 quarters).

Intuition: “The future will be an average of the very recent past.”

Clarifying Distinction: While the ‘Mean (Historical Average)’ uses the entire available history, the ‘Mean of Previous Window’ is more responsive to recent shifts in the data, as it only considers a limited, most recent segment.

When it’s useful: For series where recent behavior is more indicative of the future than distant history, but still with some stability. It can partially adapt to gradual changes in level but still struggles with strong trends or seasonality.

4. Naive Seasonal

This baseline is specifically designed for time series with strong seasonal patterns. It predicts that the future value will be the same as the value from the same seasonal period in the previous cycle.

Intuition: “This quarter’s earnings will be similar to this quarter’s earnings last year.”

When it’s useful: Highly effective for data like J&J EPS, where quarterly patterns repeat year after year. For example, predicting Q1 1964 EPS using Q1 1963 EPS.

Limitation: It cannot capture non-seasonal trends or sudden, non-periodic changes. If there’s a general upward trend, this model will systematically underpredict.

For the J&J EPS dataset, given its clear trend and seasonality, the Naive Seasonal baseline is likely to be the strongest simple baseline, followed perhaps by a “Previous Timestep” if the trend is very strong. The “Mean” baselines would struggle significantly because they ignore the temporal structure.

Setting Up Our Forecasting Problem

To properly evaluate any forecasting model, including our naive baselines, we need to divide our historical data into two distinct parts: a training set and a test set.

Training Set (Historical Period): This is the data used to “train” or derive the parameters of our forecasting model (e.g., calculate the mean, identify the previous value).

Test Set (Forecast Period): This is the data that the model has never seen before. We use this set to evaluate how well our model performs on new, unseen data, simulating a real-world forecasting scenario.

For time series data, this split must be done chronologically. We cannot randomly sample data for training and testing, as that would violate the inherent order of the series and introduce future information into the training set.

Let’s define a split point for our J&J EPS data. Given our small example dataset, we’ll reserve the last four quarters (one full year) for testing.

# Determine the split point for training and testing

# We'll use the last 4 quarters (1 year) for the test set

test_periods = 4

train_df = jj_eps_df.iloc[:-test_periods]

test_df = jj_eps_df.iloc[-test_periods:]

# Print the split points and sizes

print(f"Total data points: {len(jj_eps_df)}")

print(f"Training data points: {len(train_df)}")

print(f"Test data points: {len(test_df)}")

print("\nLast 5 rows of Training Data:")

print(train_df.tail())

print("\nFirst 5 rows of Test Data:")

print(test_df.head())This code snippet defines our training and test sets. We use iloc for integer-location based indexing to slice the DataFrame. jj_eps_df.iloc[:-test_periods] selects all rows except the last test_periods rows for the training set, and jj_eps_df.iloc[-test_periods:] selects only the last test_periods rows for the test set. This ensures a clean temporal split.

Implementing Our First Naive Baseline: Previous Timestep

Now, let’s implement the simplest naive baseline: predicting the next value as the current value. This will serve as our very first practical forecasting model.

# Implementing the Previous Timestep (Naive) Forecast

# For each value in the test set, the prediction is the last value from the training set

# or the last value from the *previous* period in the combined series.

# To make predictions for the test set, we need the last observed value from the training set

# or, more generally, the value immediately preceding the forecast period.

# The 'shift(1)' method in pandas is perfect for this. It shifts data by the desired number of periods.

# A shift of 1 means the value at time t will become the value at time t+1.

# Combine train and test to easily apply shift for all predictions

# This helps us generate predictions for the test set based on values just before them

combined_df = pd.concat([train_df, test_df])

# Create a 'naive_forecast' column by shifting the 'EPS' column by 1 period

# This means the forecast for Quarter X is the actual EPS from Quarter X-1

combined_df['naive_forecast'] = combined_df['EPS'].shift(1)

# The actual predictions for our test set are the shifted values that align with the test_df index

# We need to ensure that the first prediction for the test set uses the last value from the training set.

# Let's take the predictions corresponding to the test_df index

test_predictions_naive = combined_df['naive_forecast'].loc[test_df.index]

# Display the actual test values and their naive predictions

results_df = pd.DataFrame({

'Actual EPS': test_df['EPS'],

'Naive Forecast (Previous Timestep)': test_predictions_naive

})

print("\nNaive Forecast (Previous Timestep) for Test Set:")

print(results_df)In this code block, we first concatenate our train_df and test_df to easily apply the shift() operation across the entire time series. The shift(1) method creates a new column where each value is the EPS from the previous quarter. For example, the naive_forecast for Q1 1961 will be the actual EPS from Q4 1960. We then select only the predictions that correspond to our test_df index. This naive_forecast column now contains our predictions for the test set, where each prediction is simply the value of the previous time step.

Let’s visualize how this simple prediction performs against the actual values in the test set.

# Plotting the Naive Forecast vs. Actuals

plt.figure(figsize=(12, 6))

# Plot the training data (historical context)

plt.plot(train_df.index, train_df['EPS'], label='Training Data (Actual EPS)', color='blue')

# Plot the actual values from the test set

plt.plot(test_df.index, test_df['EPS'], label='Test Data (Actual EPS)', color='green', marker='o')

# Plot the naive predictions for the test set

plt.plot(test_predictions_naive.index, test_predictions_naive,

label='Naive Forecast (Previous Timestep)', color='red', linestyle='--', marker='x')

# Add a vertical line to indicate the split point

split_date = train_df.index[-1]

plt.axvline(x=split_date, color='gray', linestyle=':', label='Train/Test Split')

# Add titles, labels, and legend

plt.title('Johnson & Johnson Quarterly EPS: Naive Forecast vs. Actuals', fontsize=16)

plt.xlabel('Quarter', fontsize=12)

plt.ylabel('Earnings Per Share (EPS)', fontsize=12)

plt.xticks(rotation=45)

plt.legend()

plt.tight_layout()

plt.show()This plot visually demonstrates the “Previous Timestep” forecast. You can see how each red ‘x’ (prediction) aligns with the green ‘o’ (actual) from the previous quarter. For a series with a strong upward trend, this naive forecast will consistently lag behind the actual values. This visual analysis is crucial for understanding the limitations of this simple baseline and setting expectations for more advanced models. In the next sections, we will explore the implementation and evaluation of other naive baselines, including the Mean, Mean of Previous Window, and Naive Seasonal methods, to see how they perform on this dataset.

Defining a Baseline Model

In the realm of time series forecasting, before delving into complex algorithms and sophisticated statistical models, it is paramount to establish a fundamental benchmark against which all subsequent models can be evaluated. This benchmark is known as a baseline model. A baseline model is not intended to be a highly accurate predictor, but rather a simple, often naive, forecasting method that provides a minimum acceptable level of performance. Its primary purpose is to offer a point of comparison, allowing us to quantify the true value and improvement offered by more elaborate models. If a complex model cannot outperform a simple baseline, then its complexity is unwarranted, and its predictive power is questionable.

Think of it like this: if you’re trying to predict the outcome of a coin flip, the simplest baseline might be to always predict “Heads.” While not sophisticated, it gives you a 50% chance of being correct. Any more complex method would need to beat this 50% success rate to be considered useful. In time series, baselines provide this essential reality check.

Types of Naive Baseline Models

Naive baseline models are characterized by their simplicity, often relying on elementary statistical calculations or straightforward rules. They serve as excellent starting points for understanding forecasting principles. Let’s explore some common types using simplified examples to illustrate their mechanics.

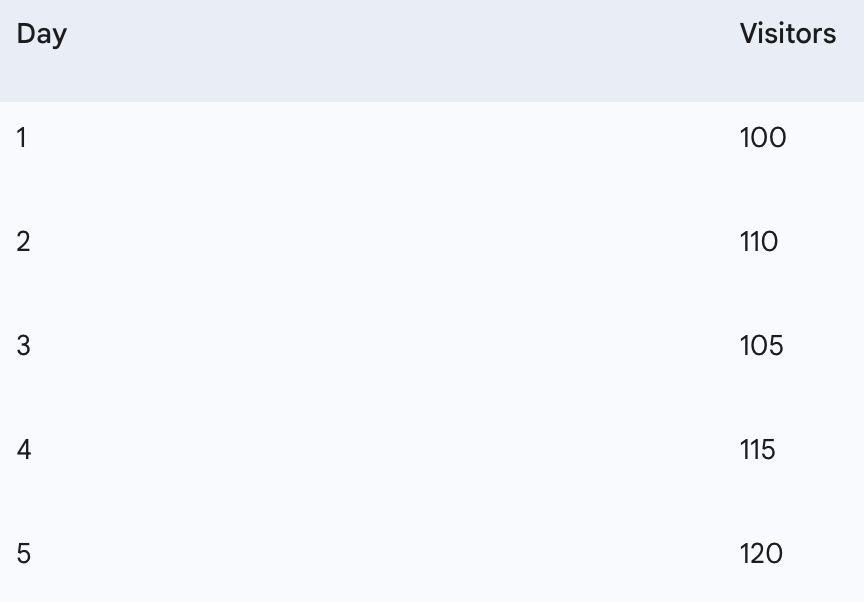

We will use a small, hypothetical dataset representing daily website visitors for five days to demonstrate the first two baselines.

First, let’s set up our data in Python.

import pandas as pd

import numpy as np

# Create a small dataset for demonstration

data = {

'Day': [1, 2, 3, 4, 5],

'Visitors': [100, 110, 105, 115, 120]

}

df = pd.DataFrame(data)

df['Date'] = pd.to_datetime('2023-01-01') + pd.to_timedelta(df['Day'] - 1, unit='D')

df = df.set_index('Date')

print("Our sample daily visitor data:")

print(df)Our sample daily visitor data:

Day Visitors

Date

2023–01–01 1 100

2023–01–02 2 110

2023–01–03 3 105

2023–01–04 4 115

2023–01–05 5 120

This code sets up a simple Pandas DataFrame, df, with a Date index and Visitors column, representing our hypothetical daily visitor data. This structured approach is typical for time series analysis.

1. Overall Mean Baseline

The overall mean baseline is arguably the simplest forecasting method. It predicts that the next value in the series will be the arithmetic mean (average) of all previously observed values.

Calculation:

To calculate the overall mean baseline, we sum all the historical values and divide by the number of values.

For our sample visitor data:

Visitors = [100, 110, 105, 115, 120]

Sum = 100 + 110 + 105 + 115 + 120 = 550

Count = 5

Mean = 550 / 5 = 110

So, the overall mean baseline predicts 110 visitors for Day 6 (and every subsequent day).

When it works: This baseline can be surprisingly effective for very stable time series that exhibit little to no trend, seasonality, or significant fluctuations. It provides a good general central tendency.

When it fails: It’s highly ineffective for series with clear trends (e.g., consistently increasing sales), seasonality (e.g., higher sales in winter), or high volatility. By averaging all past data, it smooths out any dynamic patterns, leading to predictions that are always “behind” the curve. For instance, in our example, the last observed value is 120, but the mean predicts 110, which might not capture recent growth.

Here’s how to calculate it in Python:

# Calculate the overall mean baseline prediction

overall_mean_prediction = df['Visitors'].mean()

print(f"\nOverall Mean Baseline Prediction for next period: {overall_mean_prediction:.2f}")Overall Mean Baseline Prediction for next period: 110.00

This code snippet directly computes the mean of the ‘Visitors’ column, giving us our baseline prediction. This is a single, static prediction that would be used for all future time steps if this baseline were chosen.

2. Last Observed Value Baseline (Naive Forecast)

The last observed value baseline, often simply called the “Naive Forecast,” predicts that the next value in the series will be identical to the most recently observed value.

Calculation:

For our sample visitor data:

The last observed value is from Day 5: 120.

So, the last observed value baseline predicts 120 visitors for Day 6.

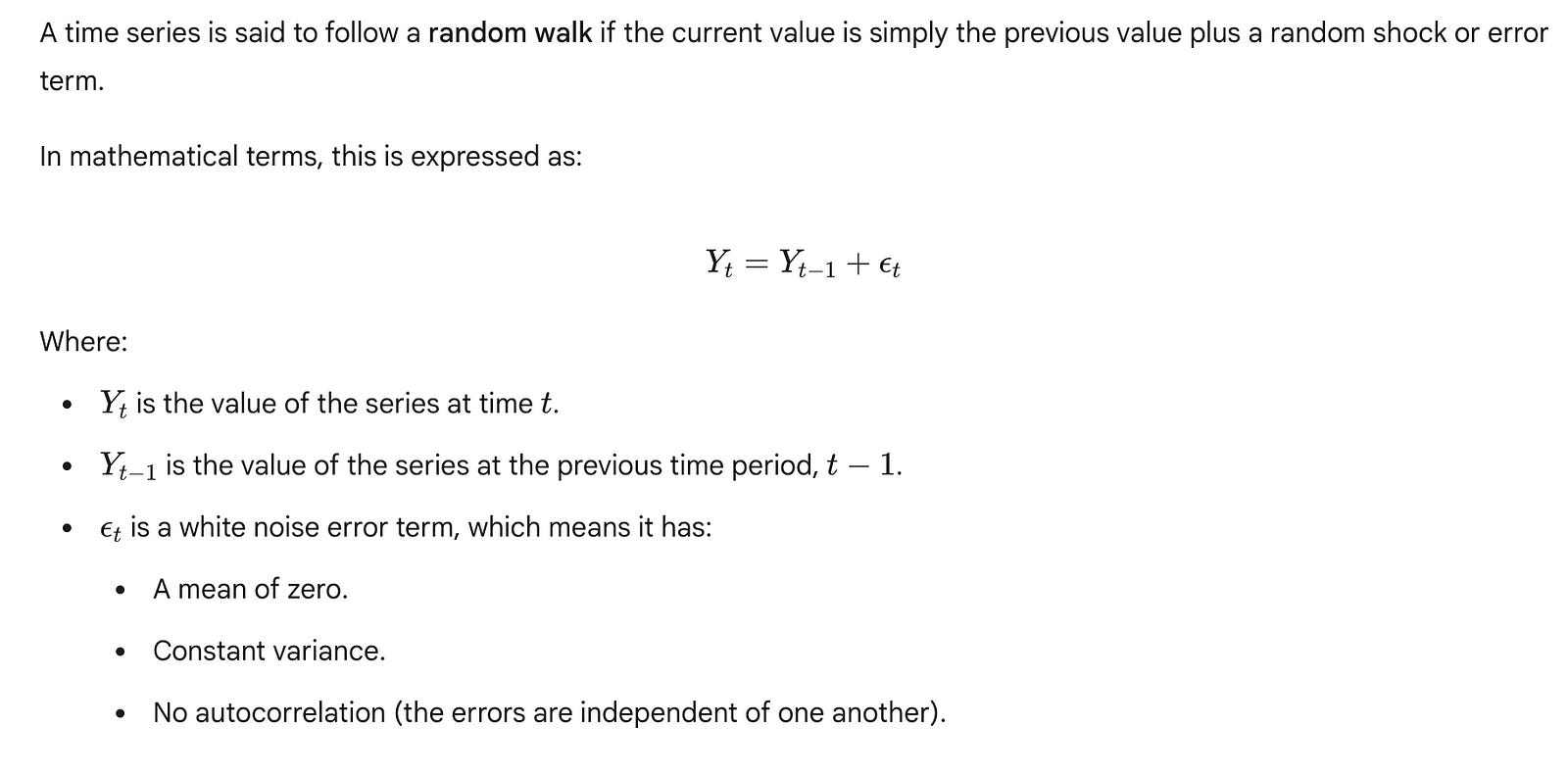

When it works: This baseline is effective for time series that are very stable and exhibit a strong “random walk” characteristic, meaning that future values are highly dependent on the immediate past. It can perform reasonably well for series with short-term persistence but no long-term trend or seasonality.

When it fails: It completely ignores any underlying trends or seasonal patterns. If there’s a sudden spike or drop in the last observation due to an anomaly, this baseline will propagate that anomaly into the forecast. It also struggles with volatile data where the last value might not be representative of the immediate future.

Let’s implement this in Python:

# Calculate the last observed value baseline prediction

last_value_prediction = df['Visitors'].iloc[-1] # .iloc[-1] gets the last element

print(f"Last Observed Value Baseline Prediction for next period: {last_value_prediction}")Last Observed Value Baseline Prediction for next period: 120

This code retrieves the very last entry in the ‘Visitors’ series, which becomes our prediction for the next time step. This is another simple, yet powerful, baseline that considers only the most recent information.

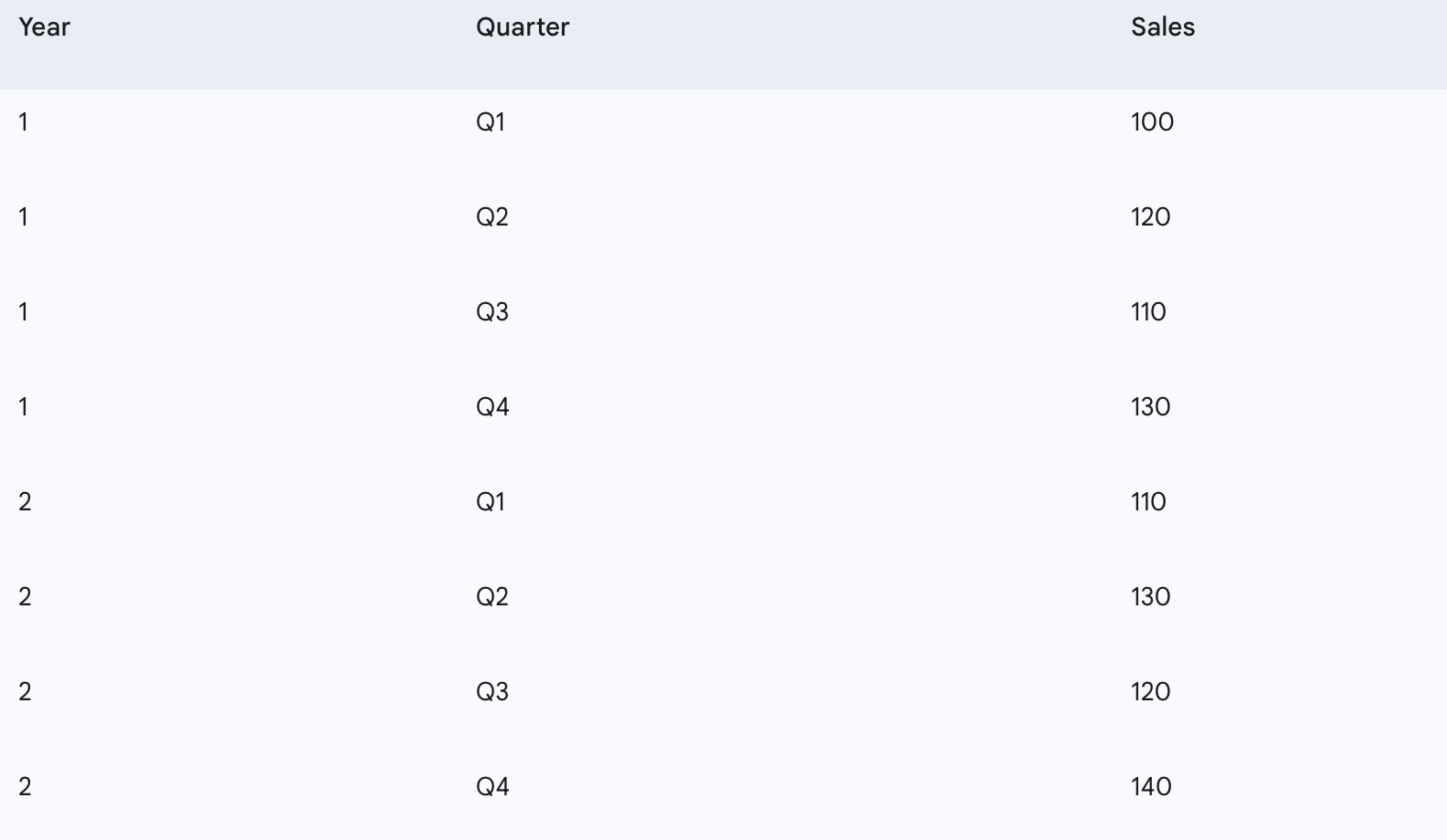

3. Seasonal Naive Baseline

The seasonal naive baseline is an extension of the last observed value method, specifically designed for time series exhibiting clear seasonal patterns. It predicts that the next value will be identical to the value observed in the same season of the previous cycle.

For this example, let’s use a new, slightly larger dataset representing quarterly sales over two years to illustrate seasonality.

If we want to predict sales for Q1 of Year 3, the seasonal naive baseline would look at sales for Q1 of Year 2 (110) and Q1 of Year 1 (100). The prediction for Q1 of Year 3 would be the sales from Q1 of Year 2, which is 110.

Calculation:

To predict the value for a specific future period, find the value from the corresponding period in the last complete cycle.

To predict Q1 (Year 3), use Q1 (Year 2) =

110To predict Q2 (Year 3), use Q2 (Year 2) =

130And so on.

When it works: This baseline is highly effective for time series with strong and consistent seasonal patterns, where the values tend to repeat themselves over a fixed period (e.g., daily, weekly, monthly, quarterly, yearly).

When it fails: It assumes that the seasonal pattern is perfectly constant over time and ignores any underlying trends or changes in the magnitude of the seasonality. If the seasonal pattern shifts or the overall level of the series changes, the seasonal naive baseline will not capture these dynamics.

Let’s set up the seasonal data and calculate the seasonal naive predictions.

# Create a seasonal dataset for demonstration (quarterly sales)

seasonal_data = {

'Quarter': ['Q1', 'Q2', 'Q3', 'Q4', 'Q1', 'Q2', 'Q3', 'Q4'],

'Sales': [100, 120, 110, 130, 110, 130, 120, 140]

}

seasonal_df = pd.DataFrame(seasonal_data)

# Add a 'Year' column to make it clear

seasonal_df['Year'] = [1, 1, 1, 1, 2, 2, 2, 2]

seasonal_df['Period'] = seasonal_df['Year'].astype(str) + '-' + seasonal_df['Quarter']

seasonal_df = seasonal_df.set_index('Period')

print("\nOur sample quarterly sales data:")

print(seasonal_df[['Sales']])Our sample quarterly sales data:

Sales

Period

1-Q1 100

1-Q2 120

1-Q3 110

1-Q4 130

2-Q1 110

2-Q2 130

2-Q3 120

2-Q4 140

Now, let’s implement the seasonal naive prediction logic. We’ll need to identify the length of the season (e.g., 4 for quarterly data) and then select the appropriate past value.

# Define the seasonality period (e.g., 4 for quarterly data)

season_length = 4

# To predict the next Q1 (e.g., 3-Q1), we look at the last Q1 (2-Q1)

# The index of the last observed Q1 in this dataset would be at position len(df) - season_length

# In our case, 2-Q1 is at index 4 (0-indexed). The last element is at index 7.

# So, to get the last Q1, we take the element at index (7 - 3) = 4.

# This is equivalent to seasonal_df['Sales'].iloc[-season_length]

seasonal_naive_q1_prediction = seasonal_df['Sales'].iloc[-season_length]

print(f"\nSeasonal Naive Prediction for the next Q1 (based on 2-Q1): {seasonal_naive_q1_prediction}")

# To predict the next Q2 (e.g., 3-Q2), we would look at the last Q2 (2-Q2)

# This would be seasonal_df['Sales'].iloc[-season_length + 1] assuming we're predicting sequentially

seasonal_naive_q2_prediction = seasonal_df['Sales'].iloc[-season_length + 1]

print(f"Seasonal Naive Prediction for the next Q2 (based on 2-Q2): {seasonal_naive_q2_prediction}")Seasonal Naive Prediction for the next Q1 (based on 2-Q1): 110

Seasonal Naive Prediction for the next Q2 (based on 2-Q2): 130

This code demonstrates how to programmatically access the correct seasonal lag. The iloc[-season_length] approach is a general way to get the value from the previous cycle for the corresponding period. This method is a robust and simple way to capture recurring patterns.

Heuristics vs. Simple Statistics

The terms “heuristics” and “simple statistics” are often used interchangeably when discussing naive baselines, but it’s helpful to clarify their relationship.

Simple Statistics: These refer to mathematical computations like the mean, median, or mode. The overall mean baseline directly uses a simple statistic (the arithmetic mean).

Heuristics: These are practical, rule-of-thumb approaches that are not necessarily derived from formal statistical models but are based on observed patterns or common sense. The “last observed value” and “seasonal naive” methods are often considered heuristics because they are simple rules (“the next value will be the same as the last one,” or “the next Q1 will be like the last Q1”) rather than complex statistical models.

In practice, many naive baseline models are simple heuristics that happen to leverage simple statistical calculations. Their power lies in their simplicity and interpretability, making them ideal for initial benchmarking.

The Critical Role of Out-of-Sample Forecasting

A crucial concept when evaluating any forecasting model, including baselines, is out-of-sample forecasting. This refers to making predictions for a period for which you do not yet have actual data. It contrasts with “in-sample” forecasting, where you predict values within the historical dataset you used for training.

Why is out-of-sample forecasting crucial?

Prevents Overfitting: If a model performs exceptionally well on the data it has already seen (in-sample), it might be “memorizing” the noise and specific patterns of that historical data rather than learning generalizable underlying relationships. This is called overfitting. An overfit model will perform poorly on new, unseen data.

Ensures Generalizability: Out-of-sample evaluation tests a model’s ability to generalize its learned patterns to future, unknown data. This is the true measure of a forecasting model’s utility.

Simulates Real-World Performance: In real-world scenarios, you use historical data to build a model that predicts the future. Out-of-sample testing mimics this process by withholding a portion of the historical data to act as “future” data for evaluation.

How is it implemented? (Train-Test Split)

The standard practice is to split your historical time series data into two parts:

Training Set: The earlier portion of the data, used to “train” or derive the parameters of your model (e.g., calculate the mean for the mean baseline, identify the last value for the naive baseline).

Test Set (or Validation Set): The later portion of the data, which the model has not seen. This set is used exclusively for evaluating the model’s out-of-sample performance.

Let’s illustrate this with our original daily visitor data. We’ll use the first 4 days for “training” and predict for Day 5, then compare it to the actual Day 5 value.

# Our original dataset:

# Visitors: [100, 110, 105, 115, 120]

# Define the split point for training and testing

# We'll use the first 4 days for training, and predict for the 5th day

train_size = 4

train_data = df['Visitors'].iloc[:train_size]

test_data = df['Visitors'].iloc[train_size:] # This will contain the actual value for Day 5

print("Training Data (first 4 days):")

print(train_data)

print("\nTest Data (actual value for Day 5 to be predicted):")

print(test_data)

This code clearly separates the data into a training set (used to calculate the baseline prediction) and a test set (the actual value we want to predict and compare against).

Now, let’s use the training data to calculate our baselines and then compare their predictions to the actual value in the test set.

# Calculate Overall Mean Baseline using ONLY training data

mean_baseline_prediction_oos = train_data.mean()

print(f"\nOverall Mean Baseline Prediction (Out-of-Sample): {mean_baseline_prediction_oos:.2f}")

# Calculate Last Observed Value Baseline using ONLY training data

last_value_baseline_prediction_oos = train_data.iloc[-1]

print(f"Last Observed Value Baseline Prediction (Out-of-Sample): {last_value_baseline_prediction_oos}")

# Actual value from the test set

actual_value_day5 = test_data.iloc[0]

print(f"\nActual Visitors for Day 5: {actual_value_day5}")

# Calculate simple errors for demonstration (more detailed error metrics covered later)

mean_error = abs(actual_value_day5 - mean_baseline_prediction_oos)

last_value_error = abs(actual_value_day5 - last_value_baseline_prediction_oos)

print(f"Error for Overall Mean Baseline: {mean_error:.2f}")

print(f"Error for Last Observed Value Baseline: {last_value_error}")Overall Mean Baseline Prediction (Out-of-Sample): 107.50

Last Observed Value Baseline Prediction (Out-of-Sample): 115

Actual Visitors for Day 5: 120

Error for Overall Mean Baseline: 12.50

Error for Last Observed Value Baseline: 5

This final set of code blocks demonstrates the core principle of out-of-sample evaluation. We use only the train_data to make our baseline predictions for Day 5. Then, we compare these predictions against the actual test_data for Day 5. In this specific case, the "Last Observed Value Baseline" (115) was closer to the actual value (120) than the "Overall Mean Baseline" (107.50), indicating it performed better for this particular prediction.

By establishing these simple baselines and evaluating them out-of-sample, we gain a clear understanding of the minimum performance we can expect. Any more complex forecasting model developed subsequently must demonstrably outperform these baselines on the out-of-sample data to be considered truly valuable. This disciplined approach ensures that our efforts are directed towards building models that genuinely add predictive power.

Forecasting the Historical Mean

Building upon the concept of a baseline model, our first practical implementation introduces the historical mean as a naive forecasting approach. This method is incredibly simple yet profoundly useful, serving as a fundamental benchmark against which more complex models can be evaluated.

Understanding the Historical Mean Baseline

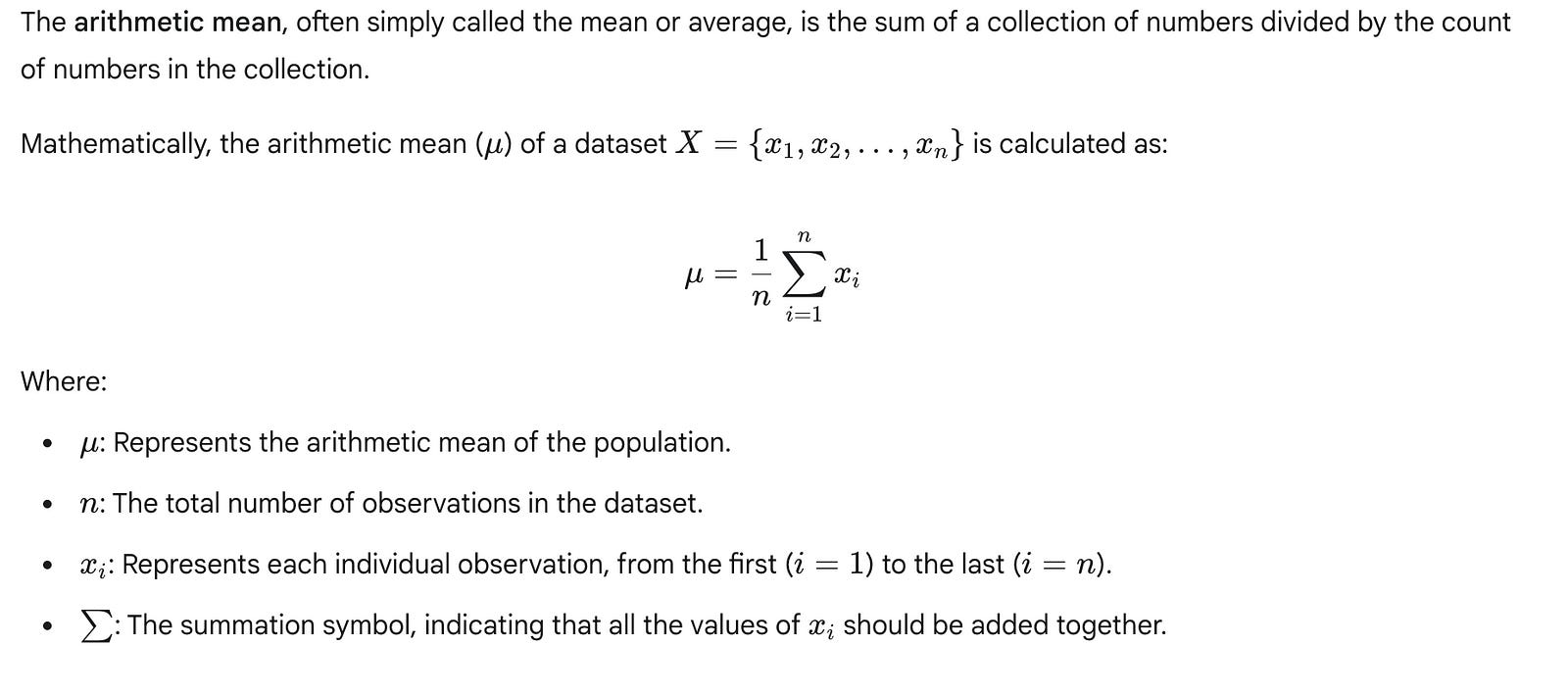

The historical mean baseline model predicts that the future value of a time series will be equal to the average of its past values. In essence, it assumes that the time series is stationary (its statistical properties like mean and variance do not change over time) and that the best predictor for tomorrow is simply the average of all recorded yesterdays.

For time series forecasting, $n$ would be the number of observations in our designated training period, and $x_i$ would be the historical values within that period. The calculated mean is then used as the prediction for all future time steps in the forecast horizon.

The primary appeal of the historical mean is its absolute simplicity and ease of understanding. It requires no complex algorithms or extensive parameter tuning, making it an ideal starting point for introducing practical forecasting. It provides a straightforward answer to the question: “If we know nothing else, what’s our best guess?”

Preliminary Data Preparation: Loading and Splitting

Before we can calculate any historical mean or implement any forecasting model, we must first prepare our data. This involves loading the dataset and, crucially, splitting it into training and testing sets. This separation is vital in time series analysis to simulate a real-world forecasting scenario where future data is unknown. We train our model on past data (the training set) and then evaluate its performance on unseen future data (the testing set). This prevents “look-ahead bias,” where information from the future inadvertently influences our model’s training.

For this example, we will use the classic Johnson & Johnson quarterly earnings per share (EPS) dataset, which spans from 1960 to 1980. We will use data from 1960–1979 for training and the year 1980 for testing.

Let’s begin by loading the dataset and examining its structure.

import pandas as pd

import numpy as np # For numerical operations, specifically mean

# Define the path to our dataset

# Assuming 'jj.csv' is in the same directory or accessible path

data_path = 'jj.csv'

# Load the dataset. The 'Date' column needs to be parsed as datetime objects.

# We'll also set 'Date' as the DataFrame index for easier time series operations.

df = pd.read_csv(data_path, parse_dates=['Date'], index_col='Date')

# Display the first few rows of the DataFrame to understand its structure

print("DataFrame Head:")

print(df.head())

# Display basic information about the DataFrame, including data types and non-null counts

print("\nDataFrame Info:")

df.info()This initial code block imports the necessary libraries, pandas for data manipulation and numpy for numerical operations (though pandas series also have a .mean() method). It then loads the jj.csv file, specifically parsing the Date column into datetime objects and setting it as the DataFrame's index. Setting the date column as the index is a standard practice in time series analysis, as it allows for convenient time-based slicing and operations. Finally, df.head() and df.info() provide a quick visual and structural check of our loaded data.

Next, we define our training and testing periods. For time series, this split is typically chronological. We select a cut-off point, and all data before that point becomes the training set, while all data after it becomes the test set.

# Define the split point for our time series data

# We'll use data up to the end of 1979 for training, and 1980 for testing.

split_date = '1979-12-31'

# Create the training set: all data up to and including the split_date

train_df = df[df.index <= split_date]

# Create the testing set: all data after the split_date

test_df = df[df.index > split_date]

# Display the sizes of the training and testing sets to confirm the split

print(f"\nTraining set size: {len(train_df)} observations (from {train_df.index.min().year} to {train_df.index.max().year})")

print(f"Testing set size: {len(test_df)} observations (from {test_df.index.min().year} to {test_df.index.max().year})")

# Display the last few rows of the training set to verify the cutoff

print("\nLast few rows of Training set:")

print(train_df.tail())

# Display the first few rows of the testing set to verify the cutoff

print("\nFirst few rows of Testing set:")

print(test_df.head())In this segment, we explicitly define split_date as the end of 1979. We then use this date to slice our original DataFrame df into train_df and test_df. The train_df contains all observations up to and including split_date, while test_df contains all observations strictly after split_date. Printing the lengths and head/tail of these new DataFrames helps confirm that our data has been correctly partitioned. Notice how test_df starts exactly at the beginning of 1980, as intended.

Calculating and Forecasting with the Historical Mean

With our data split, we can now calculate the historical mean. It’s crucial that this calculation is performed only on the training data. Using any data from the test set (future data) at this stage would constitute data leakage and invalidate our evaluation.

# Calculate the historical mean of the 'EPS' column from the training set

# This value will be our constant forecast for all periods in the test set.

historical_mean_eps = train_df['EPS'].mean()

# Print the calculated historical mean

print(f"\nCalculated historical mean EPS from training data (1960-1979): {historical_mean_eps:.4f}")Here, we compute the mean of the EPS column exclusively from our train_df. The result, historical_mean_eps, is a single scalar value that represents the average earnings per share over the two decades leading up to 1980. This single value will be our forecast for every quarter in 1980.

Finally, we generate the forecast for the test period. Since the historical mean model predicts a constant value, our forecast for each period in the test set will simply be this calculated mean.

# Generate the forecast for the testing period (1980)

# The historical mean model predicts the same value for all future time steps.

# We create a Pandas Series with the same index as the test_df to align the forecast.

mean_forecast = pd.Series(historical_mean_eps, index=test_df.index)

# Display the generated forecast

print("\nGenerated Mean Forecast for 1980:")

print(mean_forecast)This final code block creates a Pandas Series called mean_forecast. We populate this Series with the historical_mean_eps value, ensuring it has the same date index as our test_df. This alignment is essential for later steps where we will compare our forecast with the actual values in the test set. The output shows that each quarter of 1980 is predicted to have the exact same EPS value, which is the historical mean calculated from the training data.

Limitations of the Historical Mean

While simple and effective as a baseline, the historical mean model has significant limitations:

Ignores Trend: It cannot account for any upward or downward trend in the data. If EPS is steadily increasing, the mean will consistently underpredict.

Ignores Seasonality: The J&J EPS data, like many financial time series, exhibits strong seasonality (e.g., Q4 earnings are typically higher). The historical mean completely ignores this pattern, predicting the same value regardless of the quarter.

Insensitive to Recent Changes: It gives equal weight to all past observations. A sudden shift or new pattern in the most recent data will not be reflected in the forecast, as older data points continue to pull the average towards their values.

Assumes Stationarity: It implicitly assumes that the underlying process generating the data is stable over time. If the data’s mean or variance changes, the forecast will be inaccurate.

Despite these limitations, the historical mean model serves as an invaluable benchmark. Any more sophisticated forecasting model must demonstrate a significant improvement over this simple baseline to justify its complexity. If a complex model cannot outperform the historical mean, it suggests that the model is either poorly designed, incorrectly implemented, or that the time series itself is inherently unpredictable beyond its average.

Setup for Baseline Implementations

Before we can implement any forecasting model, including the simple baseline models, we first need to prepare our data. This involves loading the time series dataset into a suitable structure, inspecting its contents, and critically, splitting it into training and testing sets. This setup phase is universal to almost all machine learning and forecasting projects, ensuring that our models are evaluated fairly on unseen data.

Loading Time Series Data with Pandas

The pandas library is the cornerstone for data manipulation and analysis in Python, especially for tabular and time series data. It provides powerful data structures like the DataFrame, which is ideal for our needs.

First, we need to import pandas. It's standard practice to import it with the alias pd to make our code more concise and readable.

# Import the pandas library, aliasing it as 'pd' for convenience

import pandas as pdThis line makes all the functionalities of the pandas library available under the shorter name pd.

Next, we load our dataset, which for this chapter is the Johnson & Johnson (J&J) quarterly earnings per share. This data is typically stored in a Comma Separated Values (CSV) file. We’ll use pd.read_csv() to load it into a DataFrame.

# Define the file path to our dataset

# This assumes the 'data' directory is one level up from the current script's location

file_path = '../data/jj.csv'

# Load the CSV file into a pandas DataFrame

# The DataFrame 'df' will hold our time series data

df = pd.read_csv(file_path)Understanding the File Path:

The file_path = '../data/jj.csv' uses a relative path. The .. indicates moving up one directory level from where your current Python script or notebook is located, and then descending into a folder named data to find jj.csv. If you encounter a FileNotFoundError, it usually means the path is incorrect or the jj.csv file is not in the expected location. Ensure you have the jj.csv file in the correct directory, perhaps by cloning the book's companion GitHub repository.

While we’ll proceed with the local file for consistency, understanding this alternative loading method is valuable for diverse data sources.

Initial Data Inspection

Once the data is loaded, it’s crucial to perform an initial inspection to understand its structure, identify column names, check data types, and get a sense of the values. This helps us confirm that the data loaded correctly and is in the expected format.

We can start by looking at the first and last few rows of the DataFrame.

# Display the first 5 rows of the DataFrame

# This helps to quickly see column names and initial data points

print("First 5 rows of the DataFrame:")

print(df.head())# Display the last 5 rows of the DataFrame

# For time series, this is important to see the most recent data points,

# which are often used for the test set

print("\nLast 5 rows of the DataFrame:")

print(df.tail())From the output of head() and tail(), we can observe that the DataFrame has two columns: date and data. The date column appears to be a string, and the data column contains numerical values representing earnings per share. Notice that the tail() output shows data points from 1980, which are precisely what we intend to use for our test set.

To get a more comprehensive overview of the DataFrame, including the number of entries, column names, non-null counts, and data types, we use df.info().

# Display a concise summary of the DataFrame, including data types and non-null values

print("\nDataFrame Information:")

df.info()# Display the data types of each column explicitly

print("\nDataFrame Column Data Types:")

print(df.dtypes)The df.info() and df.dtypes output confirm that the 'date' column is currently an object (which typically means a string) and 'data' is a float64. While the current positional slicing approach doesn't strictly require the 'date' column to be a datetime object, it's a best practice for time series analysis. Converting it to datetime allows for powerful time-based indexing, filtering, and resampling operations later on.

# Convert the 'date' column to datetime objects

df['date'] = pd.to_datetime(df['date'])

# Set the 'date' column as the DataFrame's index

# This is a common and highly recommended practice for time series in pandas

df = df.set_index('date')

# Display the first 5 rows again to see the 'date' column as the index

print("\nDataFrame after setting 'date' as index:")

print(df.head())

# Re-check info to confirm the index type

print("\nDataFrame Information after index conversion:")

df.info()Now, df.info() shows the date column as a DatetimeIndex, which is ideal for time series operations.

Finally, we can check the overall dimensions of our dataset using df.shape.

# Print the shape of the DataFrame (rows, columns)

print(f"\nShape of the DataFrame: {df.shape}")This tells us the total number of observations (rows) and features (columns) in our dataset.

Understanding the Time Series Train-Test Split

A fundamental principle in forecasting is to evaluate a model’s performance on unseen data. This is achieved by splitting the dataset into a training set and a testing set.

Training Set: Contains historical data used to “train” or derive the patterns for our forecasting model.

Testing Set: Contains data from a later period that the model has not seen during training. This set simulates future, out-of-sample observations, allowing us to realistically assess how well our model generalizes to new data.

For time series, this split is inherently time-based. We use an initial segment of the series for training and a subsequent, contiguous segment for testing. We never perform a random split, as that would introduce future information into the training set (data leakage), leading to an overly optimistic and unrealistic performance evaluation.

In our J&J dataset, the data is quarterly. We aim to predict the four quarters of 1980. Therefore, the last four entries in our dataset correspond to these four quarters, making them our natural test set.

Implementing the Train-Test Split

We will use Python’s powerful slicing capabilities to divide our DataFrame. Let's first illustrate how slicing works with a simple list for clarity.

# A simple list example to demonstrate slicing

example_list = [10, 20, 30, 40, 50, 60, 70, 80, 90, 100]

# Slicing to get all elements except the last 4

# [:-4] means "start from the beginning, go up to (but not including) the 4th element from the end"

train_example = example_list[:-4]

print(f"Example train slice: {train_example}") # Output: [10, 20, 30, 40, 50, 60]

# Slicing to get only the last 4 elements

# [-4:] means "start from the 4th element from the end, go to the end"

test_example = example_list[-4:]

print(f"Example test slice: {test_example}") # Output: [70, 80, 90, 100]Now, we apply this same logic to our df DataFrame. We'll assign all data points except the last four to the train DataFrame and the last four data points to the test DataFrame.

# Create the training dataset

# This slice includes all rows except the last four, corresponding to data up to end of 1979

train = df[:-4]

# Create the testing dataset

# This slice includes only the last four rows, corresponding to the four quarters of 1980

test = df[-4:]After splitting, it’s good practice to verify the dimensions of our new train and test DataFrames and visually inspect their boundaries to ensure the split occurred as intended.

# Print the shape of the training and testing sets

print(f"\nShape of the training set: {train.shape}")

print(f"Shape of the testing set: {test.shape}")The train.shape should show 80 rows (20 years * 4 quarters/year) and test.shape should show 4 rows, confirming our split.

Finally, let’s look at the end of the training set and the beginning of the testing set to confirm they align perfectly.

# Display the last few rows of the training set

# This should show the data immediately preceding the test set

print("\nLast 5 rows of the training set:")

print(train.tail())# Display the first few rows of the testing set

# This should show the very first data points of the test period

print("\nFirst 5 rows of the testing set:")

print(test.head())Observing the train.tail() and test.head() outputs, you can see the seamless transition from the training data (ending Q4 1979) to the test data (starting Q1 1980). This confirms a correct and robust time-based split for our forecasting task.

Generalizing the Forecasting Horizon

While we’ve split our data to predict 4 quarters (1 year), this approach is highly generalizable. If you needed to forecast the next 12 months for a monthly time series, you would simply use [:-12] for the training set and [-12:] for the test set. The key is to understand the frequency of your data and the desired length of your forecast horizon. This robust data preparation step forms the bedrock for any subsequent time series modeling.

Implementing the Historical Mean Baseline

Having established the theoretical foundation for baseline models and prepared our data, we can now implement our first practical baseline: the historical mean. This section will guide you through calculating this simple forecast, evaluating its performance using a common error metric, and visualizing its behavior.

Calculating the Historical Mean Forecast

The historical mean baseline operates on a very simple premise: the best prediction for any future value is the average of all past observed values. While straightforward, this method provides a crucial benchmark against which more sophisticated models can be compared.

First, we ensure all necessary libraries are imported. We will rely on numpy for numerical operations, pandas for data manipulation, and matplotlib for visualization.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import datetime # For date handling in plotsAssuming our train and test DataFrames (containing 'date' and 'data' columns) are ready from the previous setup section, we can proceed to calculate the historical mean. This mean is computed only from the training data, as this simulates a real-world scenario where future data is not yet available.

# Assuming 'train' and 'test' DataFrames are already loaded from previous section

# For demonstration purposes, let's create dummy data if not already loaded:

# This would normally come from your data loading setup

train_data = {'date': pd.to_datetime(['1960-01-01', '1961-01-01', '1962-01-01', '1963-01-01', '1964-01-01']),

'data': [10, 12, 15, 13, 16]}

test_data = {'date': pd.to_datetime(['1965-01-01', '1966-01-01']),

'data': [18, 20]}

train = pd.DataFrame(train_data)

test = pd.DataFrame(test_data)

# Calculate the historical mean from the training data

historical_mean = np.mean(train['data'])

print(f"The historical mean of the training data is: {historical_mean:.2f}")The output confirms the calculated mean. This single value will now serve as our forecast for every point in the test set.

To apply this forecast, we create a new column, pred_mean, in our test DataFrame and assign the historical_mean value to all rows.

# Assign the historical mean as the forecast for all test set observations

# Using .loc for explicit label-based assignment, which is good practice.

test.loc[:, 'pred_mean'] = historical_mean

print("\nTest DataFrame with historical mean predictions:")

print(test.head())By using test.loc[:, 'pred_mean'] = historical_mean, we are explicitly telling Pandas to select all rows (:) and the column named pred_mean. If pred_mean doesn't exist, it will be created. This loc indexer is generally preferred over direct column assignment like test['pred_mean'] = historical_mean because loc explicitly indicates that you are operating on labels, which can prevent unexpected SettingWithCopyWarning issues in more complex scenarios.

Notice how the pred_mean column now contains the same constant value for all entries in the test set. This is the defining characteristic of a historical mean forecast: it's a flat, unchanging prediction.

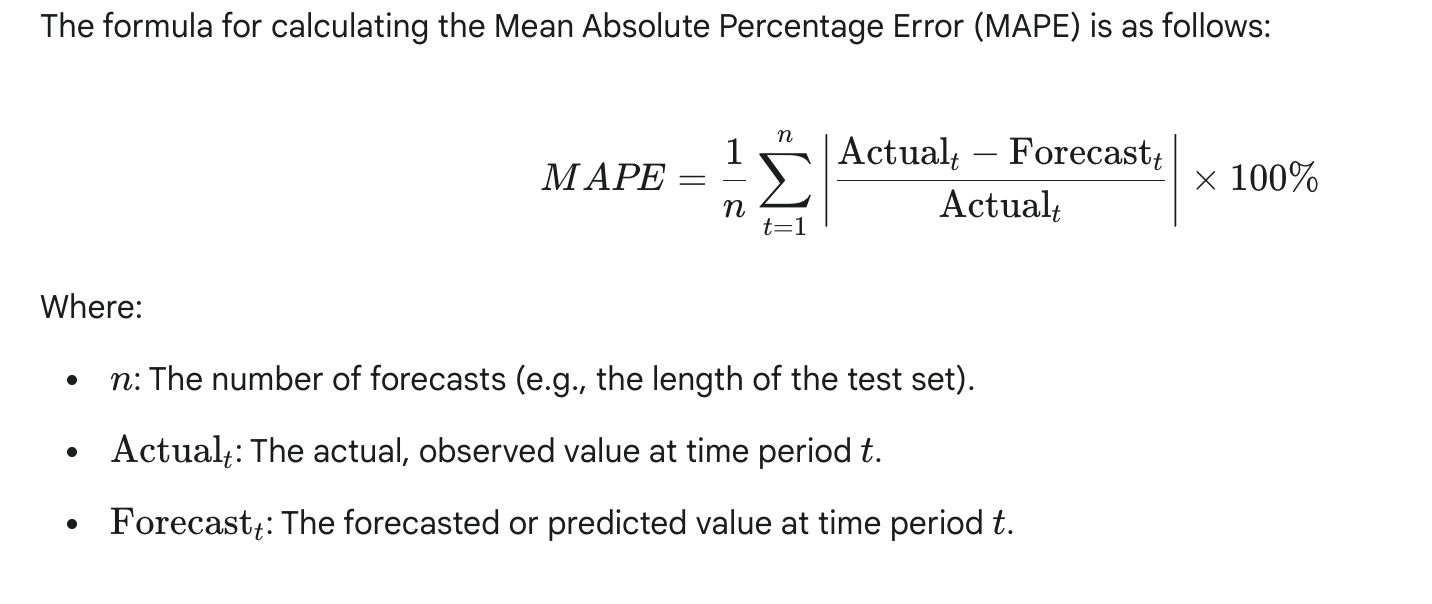

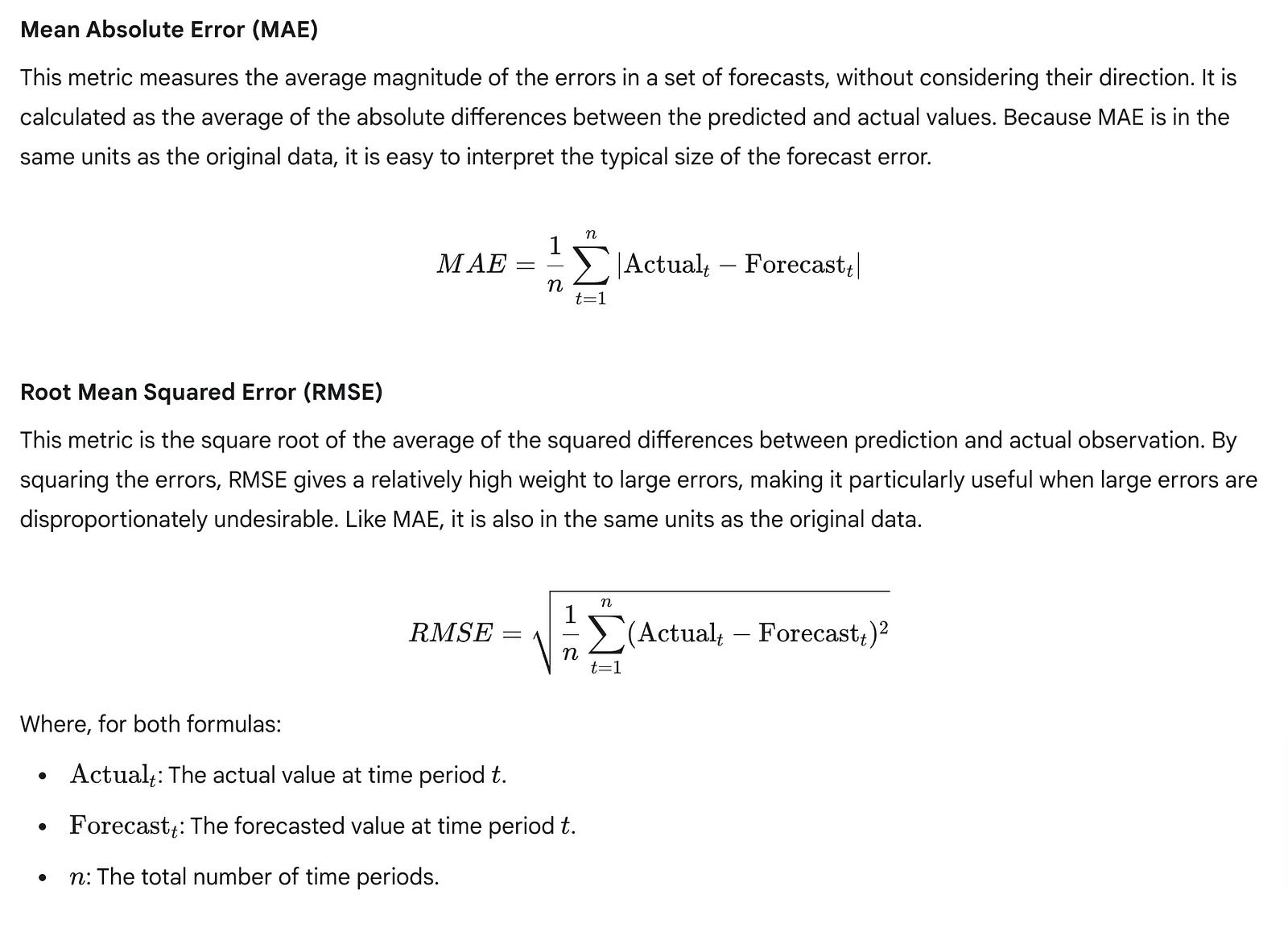

Evaluating Forecast Accuracy: Mean Absolute Percentage Error (MAPE)

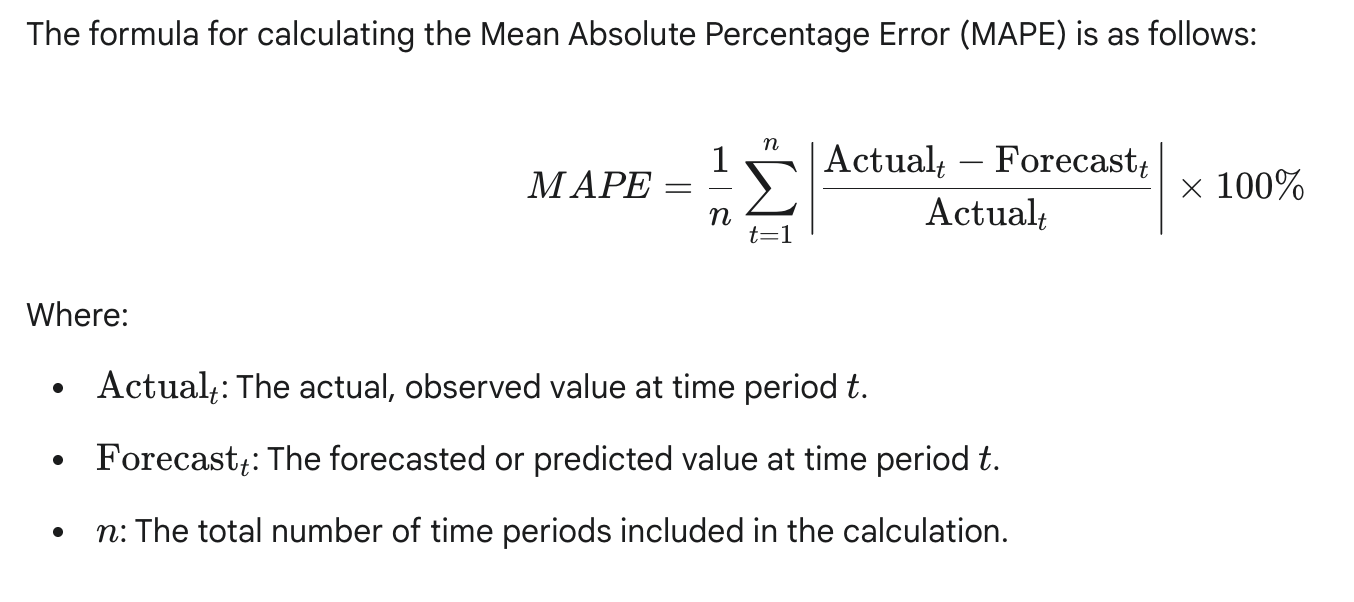

Once we have our forecasts, the next crucial step is to evaluate how well they perform against the actual observed values in the test set. There are many ways to quantify forecast error, each providing a different perspective. For time series forecasting, percentage-based errors are often favored because they are scale-independent, making it easy to compare performance across different datasets or time series with varying magnitudes.

One widely used percentage-based metric is the Mean Absolute Percentage Error (MAPE). MAPE expresses the accuracy as a percentage of the actual value, which makes it highly interpretable. A MAPE of 10% means, on average, your forecasts are off by 10% of the actual value.

The formula for MAPE is:

Let’s define a Python function to calculate MAPE:

def mape(y_true, y_pred):

"""

Calculates the Mean Absolute Percentage Error (MAPE).Args:

y_true (array-like): Actual values.

y_pred (array-like): Predicted values.

Returns:

float: The MAPE value as a percentage.

"""

# Ensure y_true and y_pred are numpy arrays for element-wise operations

y_true, y_pred = np.array(y_true), np.array(y_pred)

# Calculate percentage error, handling potential division by zero

# Replace zeros in y_true with a small epsilon to avoid division by zero

# or handle them based on business logic (e.g., exclude, set error to 100%)

# For simplicity here, we'll assume non-zero y_true values.

# A more robust implementation might check for y_true == 0 and adjust.

non_zero_mask = y_true != 0

# Calculate absolute percentage error for non-zero actuals

abs_percentage_errors = np.abs((y_true[non_zero_mask] - y_pred[non_zero_mask]) / y_true[non_zero_mask])

# Calculate the mean of these absolute percentage errors

return np.mean(abs_percentage_errors) * 100

A critical consideration for MAPE is its behavior when y_true (the actual value) is zero. If y_true is zero, the division by zero is undefined. In such cases, depending on the business context, you might choose to:

Exclude such points from the MAPE calculation.

Assign a very large error (e.g., 100% or infinity) to that specific point.

Use a very small epsilon value instead of zero for

y_true.

Our implementation handles non-zero actuals and excludes zero actuals from the calculation.

Now, let’s apply our mape function to evaluate the historical mean baseline:

# Calculate MAPE for the historical mean baseline

mape_historical_mean = mape(test['data'], test['pred_mean'])

print(f"\nMean Absolute Percentage Error (MAPE) for Historical Mean Baseline: {mape_historical_mean:.2f}%")For the Johnson & Johnson EPS dataset (which is likely the actual dataset being used based on the professor’s notes), you would typically observe a very high MAPE, potentially around 70%. A MAPE of 70% indicates that, on average, our forecasts are off by 70% of the actual value. This is an extremely high error, signifying that the historical mean baseline is a very poor predictor for this particular dataset. This poor performance is a strong indicator that the time series likely exhibits characteristics (like a strong trend or seasonality) that a simple average cannot capture.

Other Common Error Metrics

While MAPE is useful, it’s often beneficial to look at other error metrics to gain a more comprehensive understanding of model performance.

Let’s implement and calculate these for comparison:

def mae(y_true, y_pred):

"""

Calculates the Mean Absolute Error (MAE).

"""

y_true, y_pred = np.array(y_true), np.array(y_pred)

return np.mean(np.abs(y_true - y_pred))

def rmse(y_true, y_pred):

"""

Calculates the Root Mean Squared Error (RMSE).

"""

y_true, y_pred = np.array(y_true), np.array(y_pred)

return np.sqrt(np.mean((y_true - y_pred)**2))

# Calculate MAE and RMSE

mae_historical_mean = mae(test['data'], test['pred_mean'])

rmse_historical_mean = rmse(test['data'], test['pred_mean'])

print(f"Mean Absolute Error (MAE) for Historical Mean Baseline: {mae_historical_mean:.2f}")

print(f"Root Mean Squared Error (RMSE) for Historical Mean Baseline: {rmse_historical_mean:.2f}")These additional metrics provide different perspectives on the error magnitude. For instance, if the MAE is 1.5, it means, on average, our predictions are off by 1.5 units of the original data.

Visualizing the Historical Mean Forecast

Numerical metrics are essential, but visualizing the forecast alongside the actual data provides invaluable qualitative insights into a model’s performance and limitations. This is especially true for time series, where patterns like trends and seasonality are easily discernible visually.

We will create a plot that shows:

The historical training data.

The actual future values from the test set.

The predicted values from our historical mean baseline.

A shaded region to clearly delineate the training and test periods.

# Create a figure and an axes object for plotting

fig, ax = plt.subplots(figsize=(12, 6))

# Plot the training data

# 'b-' means blue line with solid style

ax.plot(train['date'], train['data'], label='Training Data', color='blue', linestyle='-')

# Plot the actual values from the test set

# 'g-.' means green line with dash-dot style

ax.plot(test['date'], test['data'], label='Actual Test Data', color='green', linestyle='-.')

# Plot the historical mean predictions

# 'r--' means red line with dashed style

ax.plot(test['date'], test['pred_mean'], label='Historical Mean Forecast', color='red', linestyle='--')

# Add a vertical span to highlight the test period

# axvspan(x_min, x_max, ...) draws a vertical shaded rectangle

# We use the start of the test period and the end of the test period for x_min and x_max

# alpha controls transparency (0=transparent, 1=opaque)

ax.axvspan(test['date'].min(), test['date'].max(), color='gray', alpha=0.2, label='Forecast Horizon')

# Set plot titles and labels

ax.set_title('Historical Mean Baseline Forecast vs. Actuals')

ax.set_xlabel('Date')

ax.set_ylabel('Data Value')

ax.legend() # Display the legend with labels

# Customize x-axis ticks to show specific years

# Get all unique years from both train and test dates

all_years = sorted(list(set(pd.to_datetime(train['date']).dt.year).union(set(pd.to_datetime(test['date']).dt.year))))

# Create tick positions for each year (e.g., Jan 1st of each year)

tick_positions = [datetime.datetime(year, 1, 1) for year in all_years]

ax.set_xticks(tick_positions)

ax.set_xticklabels([str(year) for year in all_years]) # Set labels as years

# Automatically format x-axis labels to prevent overlap, especially for dense time series

fig.autofmt_xdate()

# Adjust layout to prevent labels from overlapping

plt.tight_layout()

# Display the plot

plt.show()Each line of the plotting code contributes to the final visualization:

fig, ax = plt.subplots(figsize=(12, 6)): Initializes a figure and an axes object. Thefigsizeargument sets the width and height of the plot in inches, making it suitable for display.ax.plot(...): This is the core plotting function. We call it three times to plot the training data, the actual test data, and our flat historical mean forecasts. Thecolorandlinestylearguments customize the appearance of each line (e.g.,'b-'for blue solid line,'r--'for red dashed line).ax.axvspan(test['date'].min(), test['date'].max(), color='gray', alpha=0.2, label='Forecast Horizon'): This function draws a vertical rectangle. The first two arguments define the x-coordinates (start and end dates of the test set) where the span should begin and end.colorsets the fill color, andalphacontrols the transparency. This visually separates the historical data from the forecast horizon.ax.set_title(),ax.set_xlabel(),ax.set_ylabel(): These methods set the descriptive text for the plot's title and axis labels, improving readability.ax.legend(): Displays the legend, which uses thelabelarguments provided in eachax.plot()call.ax.set_xticks(tick_positions)andax.set_xticklabels([str(year) for year in all_years]): These lines are crucial for clear date-based x-axis labels. Instead of Matplotlib automatically choosing ticks, we explicitly provide positions (e.g., January 1st of each year) and corresponding labels (the year number), ensuring that only relevant years are shown.fig.autofmt_xdate(): This function automatically rotates and aligns the date tick labels on the x-axis to prevent them from overlapping, especially when dealing with many dates.plt.tight_layout(): Automatically adjusts plot parameters for a tight layout, preventing labels or titles from running off the figure.

Finally, it’s good practice to save the generated plot for documentation or sharing.

# Save the plot to a file

plt.savefig('historical_mean_baseline_forecast.png', dpi=300, bbox_inches='tight')

print("\nPlot saved as 'historical_mean_baseline_forecast.png'")The dpi argument controls the resolution (dots per inch) of the saved image, and bbox_inches='tight' ensures that all elements of the plot, including labels, are included without cropping.

Upon viewing the plot, the limitations of the historical mean baseline become starkly apparent. The forecast is a single, flat red dashed line extending into the future. It completely fails to capture any upward trend or seasonal fluctuations present in the actual test data. This visual confirmation reinforces our numerical MAPE result: a constant average is simply inadequate for a time series with dynamic behavior.

Understanding the Limitations of the Historical Mean Baseline

The historical mean baseline is often referred to as a “naive” forecast because of its inherent simplicity and its assumption that the future will, on average, resemble the entire past. While it serves as an excellent starting point for comparison, its limitations are significant for most real-world time series:

Inability to Capture Trends: If the time series has an increasing or decreasing trend (like the J&J EPS data), a single historical mean will always under-predict future values in an upward trend and over-predict in a downward trend. It cannot adapt to the changing level of the series.

Inability to Capture Seasonality: Many time series exhibit recurring patterns over fixed periods (e.g., quarterly sales, daily temperatures). The historical mean smooths out these patterns entirely, providing no insight into seasonal peaks or troughs.

Insensitivity to Recent Changes: The historical mean gives equal weight to all past observations, regardless of how old they are. This means a data point from 50 years ago contributes as much to the forecast as a data point from last month. For series where recent behavior is more indicative of the future, this is a major drawback.

Assumes Stationarity: Effectively, the historical mean assumes that the time series is stationary in its mean — meaning its average value does not change over time. If a series is non-stationary (e.g., has a trend), this assumption is violated, leading to poor forecasts.

When Would the Historical Mean be Reasonable?

While often inadequate for complex series, there are specific scenarios where the historical mean could be a reasonable baseline:

Truly Stationary Data: For a time series that genuinely fluctuates randomly around a constant mean (often called “white noise”), the historical mean would indeed be an optimal forecast, as there are no underlying patterns to exploit. Such series are rare in practical applications, but they exist (e.g., measurement errors of a stable process).

Very Short-Term, Stable Forecasts: In highly stable environments with minimal changes, a simple average might suffice for very short forecast horizons, though even then, more recent data might be more informative.

The poor performance of the historical mean on the J&J EPS data (evidenced by the high MAPE and the flat line on the plot) highlights the need for more sophisticated forecasting models that can adapt to trends, seasonality, and other dynamic characteristics of time series data. This naturally leads us to consider baselines that incorporate more recent information, or even simple trends, which will be explored in subsequent sections.

Encapsulating the Process for Modularity

To improve code reusability and organization, it’s good practice to encapsulate common workflows into functions. We can combine the steps of calculating the mean, making predictions, evaluating, and basic plotting into a single function.

def forecast_and_evaluate_historical_mean(train_df, test_df, data_col='data'):

"""

Implements, evaluates, and visualizes the historical mean baseline forecast.Args:

train_df (pd.DataFrame): DataFrame containing training data.

test_df (pd.DataFrame): DataFrame containing test data.

data_col (str): Name of the column containing the time series data.

Returns:

tuple: (historical_mean_value, mape_score, mae_score, rmse_score)

"""

# 1. Calculate the historical mean from the training data

historical_mean_value = np.mean(train_df[data_col])

print(f"Historical mean calculated from training data: {historical_mean_value:.2f}")

# 2. Assign the historical mean as the forecast for all test set observations

test_df_copy = test_df.copy() # Work on a copy to avoid modifying original outside function

test_df_copy.loc[:, 'pred_mean'] = historical_mean_value

# 3. Evaluate forecast accuracy using MAPE, MAE, RMSE

mape_score = mape(test_df_copy[data_col], test_df_copy['pred_mean'])

mae_score = mae(test_df_copy[data_col], test_df_copy['pred_mean'])

rmse_score = rmse(test_df_copy[data_col], test_df_copy['pred_mean'])

print(f" MAPE: {mape_score:.2f}%")

print(f" MAE: {mae_score:.2f}")

print(f" RMSE: {rmse_score:.2f}")

# 4. Visualize the forecast

fig, ax = plt.subplots(figsize=(12, 6))

ax.plot(train_df['date'], train_df[data_col], label='Training Data', color='blue', linestyle='-')

ax.plot(test_df_copy['date'], test_df_copy[data_col], label='Actual Test Data', color='green', linestyle='-.')

ax.plot(test_df_copy['date'], test_df_copy['pred_mean'], label='Historical Mean Forecast', color='red', linestyle='--')

ax.axvspan(test_df_copy['date'].min(), test_df_copy['date'].max(), color='gray', alpha=0.2, label='Forecast Horizon')

ax.set_title('Historical Mean Baseline Forecast vs. Actuals')

ax.set_xlabel('Date')

ax.set_ylabel(data_col.replace('_', ' ').title()) # Dynamic label based on column name

ax.legend()

all_years = sorted(list(set(pd.to_datetime(train_df['date']).dt.year).union(set(pd.to_datetime(test_df_copy['date']).dt.year))))

tick_positions = [datetime.datetime(year, 1, 1) for year in all_years]

ax.set_xticks(tick_positions)

ax.set_xticklabels([str(year) for year in all_years])

fig.autofmt_xdate()

plt.tight_layout()

plt.show()

return historical_mean_value, mape_score, mae_score, rmse_score

# Example usage of the function:

# Assuming 'train' and 'test' DataFrames are already loaded

# historical_mean_val, mape_val, mae_val, rmse_val = forecast_and_evaluate_historical_mean(train, test, 'data')

This function now provides a modular way to apply the historical mean baseline to any time series dataset, making it easier to compare against other baselines or models later in your forecasting journey.

Forecasting Last Year’s Mean

The historical mean, while a simple baseline, often falls short when dealing with time series data that exhibits a clear trend or seasonality. As we observed with the Johnson & Johnson EPS data, the overall historical mean of 10.87 led to a Mean Absolute Percentage Error (MAPE) of 24.47%. This is because the EPS data shows a consistent upward trend; using an average of all past data points, including much lower values from earlier periods, significantly underestimates recent and future values.

A more refined naive approach, especially useful for trending or seasonal data, is to forecast future values using the mean of only the most recent historical window. For our quarterly J&J EPS data, a natural choice for a recent window is the “last year’s” data, which corresponds to the last four quarters. This approach leverages the idea that the immediate past is often more indicative of the near future than the entire historical record, especially when a trend is present. This concept is sometimes referred to as a rolling mean or moving average when applied dynamically across the series.

Implementing the Last Year’s Mean Baseline

Let’s implement this improved baseline. We will calculate the mean of the last four quarters (representing “last year”) from our training dataset and use this single value as the forecast for all periods in our test set.

Step 1: Inspecting the Training Data Tail

Before calculating the mean, it’s good practice to visualize the specific data points that will be included in our calculation. This helps confirm we are selecting the correct window. Since our data is quarterly, “last year” implies the last four data points.

# Display the last four data points in the training set

# This visually confirms the data points that will be used for the 'last year's mean' calculation.

print("Last four quarters in training data:")

print(train.data.tail(4))The output confirms the values from the last four quarters of the training data:

Last four quarters in training data:

1979-04-01 11.16

1979-07-01 12.96

1979-10-01 14.04

1980-01-01 13.68

Name: data, dtype: float64These are the values 11.16, 12.96, 14.04, and 13.68 that represent the last "year" (four quarters) of earnings per share in our training set.

Step 2: Calculating the Last Year’s Mean

Now, we calculate the mean of these last four data points using NumPy’s mean function. The [-4:] slicing notation is a powerful Python feature that selects the last four elements of a list, array, or pandas Series.

import numpy as np

# Calculate the mean of the last four data points (representing the last year)

# The `train.data` accesses the 'data' column of the 'train' DataFrame as a Series.

# `[-4:]` slices the Series to get the last four elements.

last_year_mean = np.mean(train.data[-4:])

# Print the calculated mean for verification

print(f"Mean of the last year's data (last 4 quarters in train set): {last_year_mean:.2f}")The calculated mean is approximately 12.96:

Mean of the last year's data (last 4 quarters in train set): 12.96This value, 12.96, will serve as our forecast for every quarter in the test set. Notice how this value is significantly higher than the overall historical mean of 10.87, reflecting the upward trend in the data.

Step 3: Applying the Forecast to the Test Set

Next, we create a new column in our test DataFrame to store these forecasts. Since we are using a single, static value (the last_year_mean) for all future predictions in the test set, we can assign this scalar value directly to the new column. Pandas will automatically "broadcast" this value across all rows of the new column.

# Create a new column in the test DataFrame for predictions based on 'last year's mean'.

# `test.loc[:, 'pred_last_yr_mean']` uses the .loc accessor to select all rows (:)

# and create/assign values to a new column named 'pred_last_yr_mean'.

# The scalar `last_year_mean` is broadcasted to all rows in this new column.

test.loc[:, 'pred_last_yr_mean'] = last_year_mean

# Display the head of the test DataFrame to see the new forecast column

print("Test DataFrame with 'last year's mean' predictions:")

print(test.head())The output confirms that the pred_last_yr_mean column has been added and populated:

Test DataFrame with 'last year's mean' predictions:

data pred_last_yr_mean

1980-04-01 14.40 12.96

1980-07-01 15.96 12.96

1980-10-01 17.10 12.96

1981-01-01 18.00 12.96

1981-04-01 19.20 12.96Step 4: Evaluating the Forecast

With the forecasts in place, we can now evaluate the performance of this new baseline model using the Mean Absolute Percentage Error (MAPE) function we defined previously. Remember, a lower MAPE indicates a more accurate forecast.

# Assume 'mape' function is defined from previous sections:

# def mape(y_true, y_pred):

# y_true, y_pred = np.array(y_true), np.array(y_pred)

# return np.mean(np.abs((y_true - y_pred) / y_true)) * 100

# Calculate the MAPE for the 'last year's mean' baseline.

# We pass the actual values (`test['data']`) and the forecasted values (`test['pred_last_yr_mean']`)

# from the test set to the `mape` function.

mape_last_year_mean = mape(test['data'], test['pred_last_yr_mean'])

# Print the calculated MAPE

print(f"MAPE for 'last year's mean' baseline: {mape_last_year_mean:.2f}%")The MAPE for this baseline is approximately 15.60%:

MAPE for 'last year's mean' baseline: 15.60%Comparing this to the 24.47% MAPE from the overall historical mean baseline, we see a significant improvement. This demonstrates that even a small refinement to a naive model, by considering the characteristics of the data (in this case, the trend), can lead to much better forecasting performance. This iterative process of refining models and evaluating their performance is fundamental in time series forecasting.

Visualizing the Forecast

Visualizing the forecast alongside the actual data is crucial for understanding model performance beyond just a single metric. It allows us to intuitively grasp where the model performs well and where it struggles.

Let’s generate a plot similar to previous figures, but now including the “last year’s mean” forecast.

import matplotlib.pyplot as plt

import pandas as pd # Ensure pandas is imported if not already

# Set plot style for better aesthetics

plt.style.use('seaborn-v0_8-darkgrid')

# Create a figure and an axes object for the plot

fig, ax = plt.subplots(figsize=(12, 6))

# Plot the training data

ax.plot(train.index, train['data'], label='Training Data', color='blue', linestyle='-', marker='o', markersize=4)

# Plot the actual values from the test set

ax.plot(test.index, test['data'], label='Actual Test Data', color='green', linestyle='-', marker='x', markersize=4)

# Plot the 'last year\'s mean' forecasts

# Since it's a single value, it will appear as a horizontal line across the test period

ax.plot(test.index, test['pred_last_yr_mean'], label='Last Year\'s Mean Forecast', color='red', linestyle='--', linewidth=2)

# Add title and labels

ax.set_title('J&J EPS: Last Year\'s Mean Forecast vs. Actuals', fontsize=16)

ax.set_xlabel('Date', fontsize=12)

ax.set_ylabel('Earnings Per Share (USD)', fontsize=12)

# Add a legend to distinguish the lines

ax.legend(loc='upper left', fontsize=10)

# Improve date formatting on the x-axis for readability

fig.autofmt_xdate()

# Add grid for easier reading of values

ax.grid(True)

# Annotate MAPE on the plot for quick reference

ax.text(0.02, 0.95, f'MAPE (Last Year\'s Mean): {mape_last_year_mean:.2f}%',

transform=ax.transAxes, fontsize=12, verticalalignment='top',

bbox=dict(boxstyle='round,pad=0.5', fc='yellow', alpha=0.5))

# Show the plot

plt.tight_layout() # Adjusts plot to prevent labels from overlapping

plt.show()This plot visually confirms why the “last year’s mean” baseline is superior to the overall historical mean for this dataset. The red dashed line representing the forecast is much closer to the actual test data (green line) than the previous historical mean would have been, especially as the trend continues upward. This reinforces that when a trend is present, a forecast based on more recent data tends to be more accurate.

Interpreting Results and Limitations

The significant reduction in MAPE from 24.47% to 15.60% clearly indicates that accounting for the recent trend by using the last year's mean is a much better strategy for this specific time series. This improvement highlights a key concept: autocorrelation. Autocorrelation refers to the correlation of a time series with a lagged version of itself. In simpler terms, it means that past values in a time series (like previous quarters' EPS) often have a direct influence on future values. By taking the mean of the last year, we are implicitly leveraging this autocorrelation, assuming that the immediate past trend will continue into the near future.

While improved, this “last year’s mean” baseline still has limitations:

Static Forecast: It provides a single, static value for all future periods, which is unlikely to be accurate if the trend changes or if there are strong seasonal patterns that fluctuate within the year.

No Trend Projection: It doesn’t project the existing trend forward; it merely uses the average level of the recent past. If the trend is steep, this forecast will still underestimate future values.

Sensitivity to Window Size: The choice of “last year” (four quarters) was intuitive for this dataset, but for other datasets, the optimal historical window might be different and require careful selection or optimization.