Forecasting Market Volatility: A New Era in Risk Management and Decision-Making

Leveraging Advanced Computational Models and Uncertainty Indices to Predict Financial Market Dynamics with Precision

Forecasting market volatility has become a cornerstone for understanding financial markets and managing risks effectively. Volatility measures the extent of price fluctuations in financial markets and is a critical indicator of risk for traders, investors, and policymakers. Accurate predictions of volatility allow investors to hedge against potential losses, optimize portfolio strategies, and make more informed financial decisions. Similarly, policymakers use volatility forecasts to assess the stability of financial systems and implement measures to mitigate systemic risks.

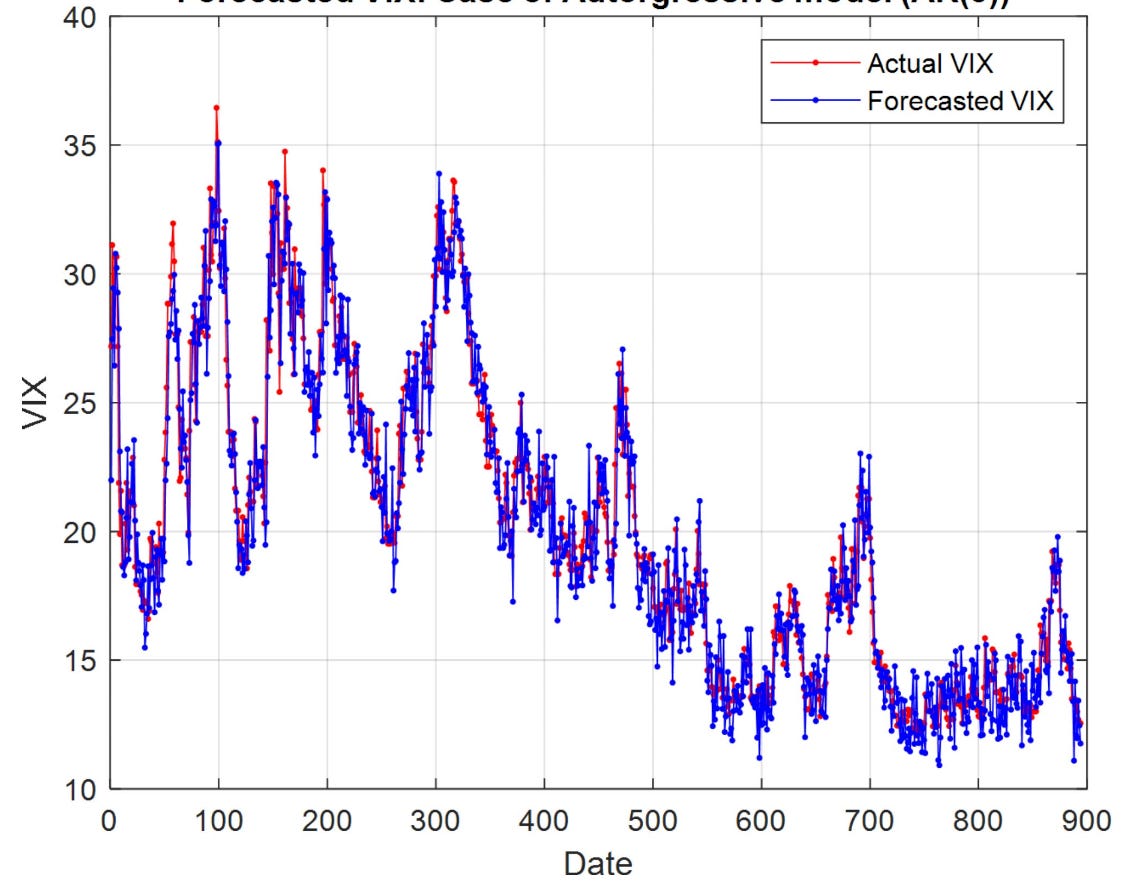

Among the various measures of volatility, implied volatility has gained prominence as a forward-looking indicator. The Chicago Board Options Exchange Volatility Index (VIX), often referred to as the “fear index,” represents market expectations of future volatility over the next 30 days. Unlike historical volatility, which relies on past price movements, implied volatility encapsulates market sentiment and anticipates future fluctuations, making it an indispensable tool for market participants. A higher VIX suggests increased uncertainty and fear in the market, typically during economic or geopolitical turbulence, while a lower VIX reflects investor confidence and stability.

Given its importance, understanding the factors that influence the VIX is critical. Traditionally, volatility prediction relied on historical price data and econometric models. However, these methods often fail to capture the full complexity of financial markets. Market behavior is shaped by various external factors, including fluctuations in commodity prices, geopolitical events, economic policies, and energy market shocks. These factors create uncertainty, which directly influences market volatility. Uncertainty indices such as the Crude Oil Volatility Index (OVX), Geopolitical Risk Index (GPR), Economic Policy Uncertainty Index (EPU), and Bloomberg Energy Index (BEI) measure these factors and provide valuable insights into their impact on financial markets. A key question arises: Can these uncertainty indices improve predictions of market volatility, especially as measured by the VIX?