How Short-Dated Speculation is Rewriting U.S. Equity Markets and Volatility Surfaces

Trading the Retail Volatility Boom

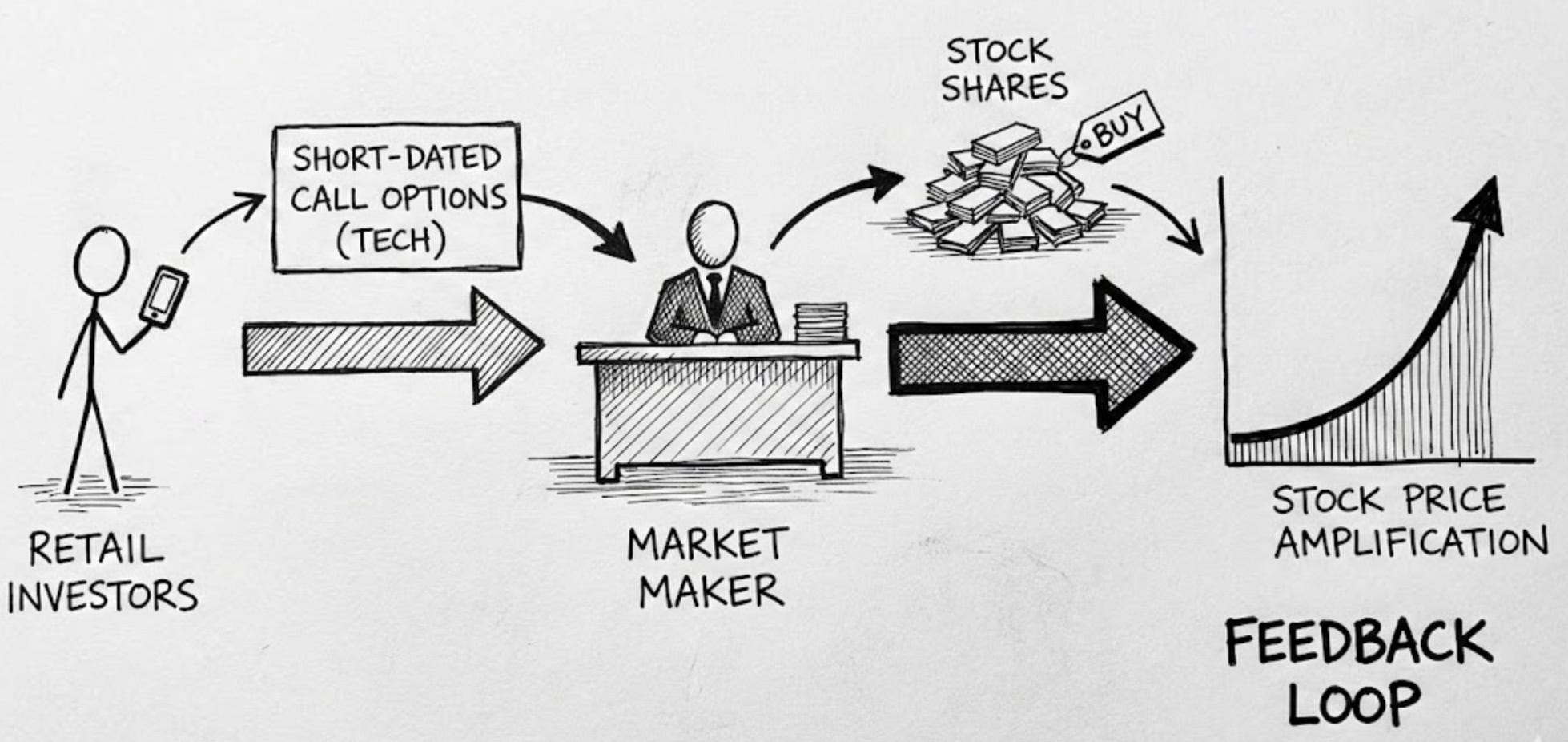

U.S. single-stock options trading has undergone a seismic shift since late 2019, marked by explosive volume growth that has reshaped derivatives markets in ways previously unseen. This surge, reaching nearly three times last year’s levels by the second quarter of 2020, far outpaced the normalization observed in index and ETF options following the initial COVID-19 panic. Unlike traditional institutional activity focused on hedging and positioning, this boom reflects a wave of speculative, retail-driven trading, concentrated in short-dated calls on large-cap technology and consumer discretionary stocks. What began as a response to zero-commission brokerages and lockdown boredom has evolved into a persistent force, distorting option pricing, volatility surfaces, and even underlying stock movements.

The data used in the article covers the period up to 2023. The study was conducted using data collected from the beginning of the COVID-19 pandemic through 2023.