I Need Money, That's Why I Wrote An Algorithm and taught it how to make

I Need Money, That's Why I Wrote An Algorithm and taught it how to make

It appears to be getting harder and harder to find extra profits in the markets. There are still fortunes to be made with a bit of human ingenuity and technical prowess. We will use this algorithm to capture one of the few remaining arbitrage strategies: volatility. Volatility arbitrage isn't as intimidating as it appears at first, so let's explore why it isn't as hard as you may think

Volatility Arbitrage

It is important to understand the relationship between option prices, Greeks, and volatility before you can understand volatility arbitrage. Delta and Implied Volatility (IV) are the two concepts to master.

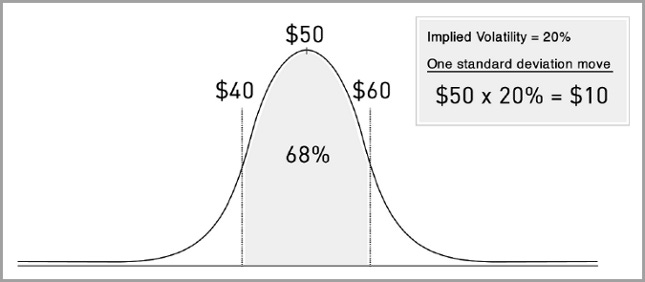

Implied Volatility

From now on, we will refer to implied volatility as IV. The market forecasts the price movement of a security over the life of an option. The market forecasts the price of an option by 90% by the time it expires, so if the IV of an option is 90%, it means that the price will increase or decrease by 90% by the expiration date.

An investor must pay a higher premium when the IV is high. As option writers must be compensated for their risks, so does their compensation need to increase.

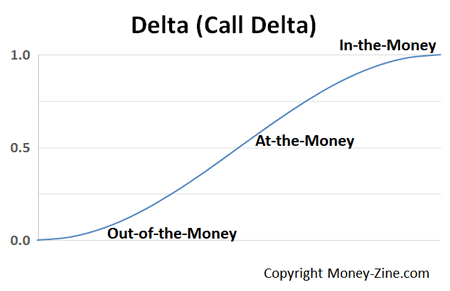

Delta

The delta is just one component of the many options greeks, but it is the most straightforward and useful. Delta is the difference between the option price and the stock price per change of $1. When the stock moves by $1, an option with a delta of .56 increases or decreases by $56. A call option's delta ranges from 0 to 1, while a put option's delta ranges from 0 to -1. There will be a need for this in the future.

Delta-Hedging

Arbitrage in this trade occurs as a result of the difference between Implied Volatility (IV) and Realized Volatility (RV). The trader's profit is the 5% difference between an option with a 95% IV and one that only moved by 90% by expiration. Delta-hedging allows the profit to be realized simultaneously.

Another simple concept is delta-hedging. In order to create a market-neutral position, a trader would short 56 shares of the underlying stock with a delta of .56, so that changes in the underlying would have an inverse effect on the call option. Trading delta-neutral positions until expiration allow the trader to earn the 5% premium mentioned above.