Mastering Vectorized Backtesting in Algorithmic Trading

Part 4/10 In the realm of algorithmic trading and high-frequency market strategies, vectorized backtesting has emerged as a transformative approach that transcends traditional loop-based paradigms.

Read Part 1

Read Part 2

Read Part 3

As the complexity of modern financial markets increases and the volume of data swells, the ability to process large datasets in real time becomes a critical factor. This chapter delves into the advanced methodologies that underpin vectorized backtesting, providing a comprehensive exploration of the mathematical foundations, algorithmic innovations, and integration techniques necessary for developing sophisticated, production-grade trading systems.

At its core, vectorized backtesting harnesses the power of parallelized computations and advanced matrix operations to simulate trading strategies with minimal latency. Unlike conventional loop-based implementations that sequentially process data, vectorized techniques operate on entire arrays or matrices of data simultaneously. This shift not only enhances computational efficiency but also allows for a more nuanced exploration of intricate market behaviors and risk patterns. By building upon the foundational concepts of linear algebra, calculus, and probability theory, vectorized backtesting models can incorporate multifaceted decision rules and dynamic risk adjustments in a streamlined, computationally efficient manner.

Mathematical Underpinnings and Theoretical Optimization

The theoretical framework of vectorized backtesting is rooted in advanced mathematics. The use of matrix algebra and vector calculus enables the representation of vast arrays of financial data in compact forms that are amenable to rapid manipulation. At the heart of these methodologies is the concept of tensor operations, which extend the ideas of matrices to higher-dimensional arrays. These operations allow for the simultaneous computation of multiple market variables, enabling traders to incorporate cross-asset correlations and multidimensional risk factors into their models.

In developing these advanced techniques, one must consider the optimization of computational resources. Mathematical optimization theories, such as convex optimization and gradient descent methods, provide a rigorous basis for refining trading strategies. In vectorized environments, the simultaneous adjustment of portfolio weights, risk exposure, and trading signals can be achieved by solving large-scale optimization problems where the objective functions are often non-linear and non-convex. Advanced solvers, which incorporate regularization techniques and stochastic approximations, are crucial for ensuring that the backtesting framework remains robust under varying market conditions.

A critical aspect of these optimization techniques involves the evaluation of performance metrics under different market scenarios. The integration of risk metrics, such as Value at Risk (VaR) and Conditional Value at Risk (CVaR), into the optimization process ensures that the backtesting framework not only maximizes returns but also accounts for tail risk and volatility clustering. The interplay between these mathematical constructs and vectorized operations allows for the rapid simulation of a myriad of market scenarios, thereby providing traders with a comprehensive understanding of strategy performance across different market regimes.

Mathematically, one can represent a trading strategy as a function that maps a high-dimensional state vector — comprising market indicators, asset prices, and risk parameters — to a trading decision. The backtesting process, in turn, involves applying this function across a time series of such vectors in a vectorized manner. This approach leads to the formulation of complex differential equations and recursive algorithms that capture the evolution of market dynamics and the resulting impact on portfolio performance. The challenge lies in efficiently solving these equations while maintaining numerical stability and ensuring that the solution converges to a realistic representation of market behavior.

In practice, these mathematical principles are embodied in a series of advanced functions that implement risk-adjusted performance metrics and dynamic allocation strategies. For instance, consider the following function definition that encapsulates a complex market impact model. The function employs a series of iterative refinements and non-linear adjustments to accurately simulate the decay factors associated with large orders:

def optimize_market_impact_calculation(order_book, trade_size, decay_factors, tolerance=1e-6, max_iterations=1000):

"""

Perform an advanced optimization to calculate the market impact of a trade.

This function uses iterative refinement to simulate non-linear decay effects

associated with large order executions. The decay_factors parameter is a dictionary

that specifies the decay rate for each level of the order book.

Parameters:

order_book: A high-dimensional list representing market depth.

trade_size: The volume of the trade for which the impact is calculated.

decay_factors: A dictionary mapping each order book level to its decay rate.

tolerance: Convergence criteria for iterative refinement.

max_iterations: Maximum iterations allowed before terminating the calculation.

Returns:

impact: The calculated market impact as a float.

"""

impact = 0.0

iteration = 0

previous_impact = float('inf')

while iteration < max_iterations and abs(previous_impact - impact) > tolerance:

previous_impact = impact

impact = 0.0

for level, volume in enumerate(order_book):

decay = decay_factors.get(level, 1)

# Simulate non-linear decay: the impact is a function of trade size, volume, and decay factor.

impact += (trade_size ** 0.5) * (volume ** 0.75) * decay

# Apply an adjustment factor based on previous iterations to ensure convergence.

impact = impact * 0.98 + previous_impact * 0.02

iteration += 1

return impactThis function epitomizes the blend of mathematical sophistication and algorithmic precision required in advanced vectorized backtesting frameworks. The iterative approach ensures that the function remains resilient to the complexities of real-world order book dynamics, while the non-linear decay computations capture the nuanced effects of large trade executions.

Algorithmic Innovations and Integration Techniques

Beyond the theoretical foundations, the practical application of vectorized backtesting necessitates innovative algorithmic strategies. Modern trading systems must integrate a multitude of signal-generating mechanisms, risk adjustment protocols, and execution models into a cohesive, highly optimized framework. Advanced algorithms are designed not only to evaluate historical data efficiently but also to adapt dynamically to emerging market trends and anomalies.

One of the key innovations in this space is the use of dynamic programming techniques that recursively break down complex strategy evaluations into manageable sub-problems. This method allows for the reuse of intermediate computations, significantly reducing the overall computational load. When implemented in a vectorized context, these dynamic programming algorithms benefit from parallel execution, enabling the rapid analysis of multiple market scenarios simultaneously.

Another frontier in algorithmic innovation involves the integration of stochastic models that account for market uncertainty and random fluctuations. Techniques such as Monte Carlo simulations and Markov Chain modeling are increasingly being adapted for vectorized environments. These methods allow traders to simulate thousands of potential market paths in parallel, providing a probabilistic assessment of strategy performance and risk exposure. By incorporating these stochastic elements into vectorized backtesting frameworks, developers can better understand the distribution of potential outcomes and refine their strategies to mitigate adverse events.

Algorithmic innovations are also reflected in the evolution of execution logic. Traditional rule-based systems are gradually being supplanted by adaptive algorithms that leverage machine learning techniques. These models, trained on historical market data, can identify subtle patterns and adjust trading parameters in real time. The integration of neural network architectures, such as convolutional or recurrent networks, with vectorized computations allows for the extraction of high-level features from raw market data, enabling more precise predictions of market movements. The transition from static to dynamic models represents a paradigm shift in backtesting methodologies, as strategies are no longer confined to pre-defined rules but can evolve in response to market conditions.

To illustrate these advanced algorithmic techniques, consider a function definition that embodies a dynamic allocation strategy based on a neural-inspired architecture. The function iteratively refines its allocation decisions using a combination of gradient-based adjustments and historical performance feedback:

def dynamic_allocation_strategy(market_data, current_allocation, learning_rate, iterations=500):

"""

Execute a dynamic allocation strategy that adjusts portfolio weights

based on high-dimensional market data and performance feedback.

The algorithm uses gradient-based refinements and recursive adjustment

to optimize the allocation over a specified number of iterations.

Parameters:

market_data: A multidimensional array representing historical market signals.

current_allocation: An initial vector of portfolio weights.

learning_rate: A scalar that determines the magnitude of adjustments.

iterations: The number of iterations to perform during optimization.

Returns:

optimized_allocation: The refined allocation vector after optimization.

"""

optimized_allocation = current_allocation.copy()

for iteration in range(iterations):

gradient = [0] * len(optimized_allocation)

# Compute gradient adjustments based on market performance and volatility.

for i in range(len(optimized_allocation)):

# Simulate a complex gradient calculation involving historical performance.

gradient[i] = sum(market_data[j][i] * (optimized_allocation[i] - 0.5) for j in range(len(market_data))) / len(market_data)

# Update the allocation using the calculated gradient.

optimized_allocation = [max(0, weight - learning_rate * grad) for weight, grad in zip(optimized_allocation, gradient)]

# Normalize the allocation vector to maintain full investment.

total = sum(optimized_allocation)

optimized_allocation = [weight / total for weight in optimized_allocation]

return optimized_allocationIn this example, the function encapsulates an iterative optimization process that continuously refines portfolio allocations. The gradient calculations are intentionally designed to capture non-linear dependencies and adapt to the evolving market landscape. Such an approach highlights the shift towards more intelligent, self-correcting trading systems where learning and adaptation are embedded within the core execution logic.

System Architecture for Scalable Backtesting

As trading strategies become increasingly sophisticated, the underlying system architecture must evolve to support high-speed data processing, memory management, and parallel computation. This chapter explores the architectural considerations essential for deploying vectorized backtesting systems at scale. The discussion encompasses both the theoretical design principles and practical implementation patterns that ensure the system can handle the high throughput and low latency required in modern trading environments.

A robust system architecture for vectorized backtesting is characterized by its ability to efficiently manage data flow, memory resources, and computational parallelism. The first challenge lies in designing a data pipeline that can ingest and preprocess massive amounts of historical market data without becoming a bottleneck. Memory management strategies must be optimized to store and retrieve data in formats that are conducive to vectorized operations. Techniques such as memory mapping, shared memory constructs, and cache optimization are essential for maintaining high performance when dealing with large datasets.

The architecture must also support parallel processing, which is a cornerstone of vectorized backtesting. By leveraging multi-core processors and distributed computing frameworks, the system can perform simultaneous computations across multiple dimensions of market data. This parallelism is not limited to the raw data processing stage but extends into the optimization and simulation phases, where each trading scenario or market condition can be evaluated independently. The challenge here is to design the system in such a way that it maximizes resource utilization while minimizing inter-process communication overhead.

Distributed computation architectures, in particular, introduce additional complexities. The system must ensure that data remains consistent across distributed nodes, and that any discrepancies in computation due to network latency or asynchronous processing do not compromise the integrity of the backtesting results. Advanced synchronization mechanisms and consensus algorithms are employed to manage these challenges, ensuring that the distributed system behaves as a coherent whole.

In this context, a layered architecture is often the most effective approach. At the lowest level, a high-performance data ingestion layer handles the retrieval and initial processing of raw market data. Above this, a vectorized computation layer performs the core backtesting operations, utilizing optimized mathematical libraries and parallel processing frameworks. The top layer is responsible for strategy optimization and risk analysis, integrating advanced machine learning algorithms and dynamic programming techniques. Each layer is designed to operate semi-independently, yet they are tightly coupled through well-defined interfaces that facilitate efficient data exchange and synchronization.

A key architectural challenge is the efficient management of computational resources. In vectorized backtesting, the memory footprint can be substantial, and the need for rapid access to large matrices and tensors demands careful consideration of both hardware and software design. Techniques such as just-in-time (JIT) compilation and hardware acceleration through graphics processing units (GPUs) are increasingly being integrated into backtesting systems. These methods allow for the offloading of intensive computations to specialized hardware, thereby freeing up central processing resources for other critical tasks.

Furthermore, system architecture must account for fault tolerance and scalability. In production environments, backtesting systems are often required to run continuously, processing new data as it becomes available. The architecture must be resilient to hardware failures, software glitches, and network interruptions. Redundancy, load balancing, and real-time monitoring are essential components of a robust system, ensuring that the backtesting process can recover gracefully from unexpected disruptions without compromising data integrity.

To illustrate these architectural principles, consider a function that encapsulates a critical component of the data synchronization logic. This function is designed to operate in a distributed environment, ensuring that disparate nodes maintain a consistent view of the backtesting state. The logic employs advanced algorithms for consensus and synchronization, making it a vital piece of the overall system architecture:

def synchronize_backtesting_state(distributed_state, local_update, consensus_threshold, max_sync_rounds=10):

"""

Synchronize the state of the backtesting system across distributed nodes.

This function employs a consensus-based mechanism to ensure that all nodes converge

on a consistent state, despite potential network delays and asynchronous updates.

The synchronization process iteratively refines the local state based on updates from

other nodes until the consensus threshold is met or the maximum number of sync rounds is reached.

Parameters:

distributed_state: A data structure representing the shared state across nodes.

local_update: The local modifications to the state that need to be synchronized.

consensus_threshold: A parameter that determines the acceptable level of state divergence.

max_sync_rounds: Maximum iterations for synchronization attempts.

Returns:

synchronized_state: The updated and synchronized state after convergence.

"""

synchronized_state = local_update.copy()

sync_round = 0

while sync_round < max_sync_rounds:

divergence = 0.0

for node_state in distributed_state:

# Calculate divergence using a complex metric that considers multiple state dimensions.

divergence += sum(abs(synchronized_state[i] - node_state[i]) for i in range(len(synchronized_state)))

divergence /= len(distributed_state)

if divergence < consensus_threshold:

break

# Adjust the synchronized state towards the average state of all nodes.

averaged_state = [0] * len(synchronized_state)

for i in range(len(synchronized_state)):

averaged_state[i] = sum(node_state[i] for node_state in distributed_state) / len(distributed_state)

synchronized_state = [(synchronized_state[i] + averaged_state[i]) / 2 for i in range(len(synchronized_state))]

sync_round += 1

return synchronized_stateThis function exemplifies the intricacies of maintaining consistency across a distributed backtesting environment. The synchronization mechanism employs iterative refinement and advanced consensus metrics, ensuring that the distributed system converges on a coherent state even in the face of network-induced variability. The careful calibration of parameters such as the consensus threshold and maximum synchronization rounds reflects the tradeoffs between speed and precision that are inherent in such systems.

Performance Tuning, Tradeoffs, and Advanced Risk Management

In highly competitive financial markets, the performance of backtesting systems is as crucial as the accuracy of the underlying trading algorithms. This chapter examines the performance tuning techniques and optimization tradeoffs that are central to the development of advanced vectorized backtesting systems. It further explores the integration of sophisticated risk management protocols that ensure the robustness and resilience of trading strategies under volatile market conditions.

Performance tuning in vectorized backtesting is a multifaceted challenge that involves both algorithmic and architectural optimizations. At the algorithmic level, the focus is on minimizing computational overhead while maximizing the accuracy and speed of simulations. Techniques such as loop unrolling, memory prefetching, and vectorized operations are employed to ensure that each operation is executed as efficiently as possible. The use of just-in-time compilation and hardware-specific optimizations, particularly on GPUs and multi-core processors, allows for significant reductions in execution time, enabling the rapid processing of complex strategies and large datasets.

At the architectural level, performance tuning revolves around the efficient allocation of computational resources and the minimization of latency. This involves optimizing data storage formats, leveraging in-memory databases, and employing asynchronous processing models that decouple data ingestion from computation. The design of efficient data pipelines is paramount, as the ability to stream large volumes of market data directly into the computation engine without intermediate bottlenecks can have a profound impact on overall system performance.

The tradeoffs in performance tuning are often non-trivial. For instance, aggressive optimization may lead to code that is difficult to maintain and extend, while overly generic solutions may fail to fully exploit the capabilities of modern hardware. Developers must balance the need for speed with the necessity for code clarity and maintainability, particularly in systems that are expected to operate continuously in production environments. In many cases, performance tuning involves iterative profiling and benchmarking, where the system is subjected to a battery of tests under various load conditions. The insights gained from these tests guide the refinement of both algorithmic and architectural components, ensuring that the system remains robust and efficient as it scales.

Risk management is another critical aspect of advanced vectorized backtesting. The inherent uncertainty and volatility of financial markets necessitate the integration of dynamic risk assessment protocols into the backtesting process. Advanced risk management systems are designed to evaluate the potential impact of adverse market movements and to adjust trading strategies in real time. These systems often incorporate probabilistic models that estimate the likelihood of extreme events and employ stress-testing techniques to evaluate strategy performance under worst-case scenarios.

One of the key challenges in risk management is the avoidance of overfitting — a phenomenon where a strategy performs exceptionally well on historical data but fails to generalize to live market conditions. Advanced backtesting systems mitigate this risk by incorporating cross-validation techniques, out-of-sample testing, and the use of regularization methods within optimization algorithms. By dynamically adjusting model parameters based on real-time performance feedback, these systems maintain a delicate balance between exploiting historical trends and adapting to new market conditions.

The integration of performance metrics with risk management protocols allows for a holistic evaluation of trading strategies. Metrics such as Sharpe ratios, maximum drawdown, and risk-adjusted returns are computed using vectorized operations that provide rapid, high-fidelity insights into strategy performance. The seamless interplay between performance optimization and risk management not only enhances the reliability of backtesting outcomes but also empowers traders to make informed decisions in live trading environments.

An illustrative example of advanced performance tuning can be seen in the following function, which integrates risk assessment into the optimization process. This function encapsulates a complex algorithm that adjusts trading signals based on both performance metrics and risk thresholds:

def optimize_trading_signal(performance_history, risk_threshold, adjustment_factor, iterations=100):

"""

Optimize the trading signal by integrating historical performance metrics with dynamic risk assessments.

The function iteratively adjusts the trading signal based on a composite metric that accounts for both

performance improvements and risk thresholds. The algorithm uses a gradient-inspired approach to converge

on an optimal signal configuration.

Parameters:

performance_history: A multidimensional array representing historical performance metrics.

risk_threshold: A scalar representing the maximum acceptable risk level.

adjustment_factor: A factor used to scale the adjustments made to the trading signal.

iterations: The number of iterations to perform during the optimization process.

Returns:

optimized_signal: The refined trading signal after the optimization process.

"""

optimized_signal = [0.5 for _ in range(len(performance_history[0]))]

for iteration in range(iterations):

composite_metric = [0] * len(optimized_signal)

for i in range(len(optimized_signal)):

performance_metric = sum(performance_history[j][i] for j in range(len(performance_history))) / len(performance_history)

# Adjust based on risk: if the performance metric exceeds the risk threshold, reduce the signal intensity.

risk_adjustment = adjustment_factor if performance_metric > risk_threshold else -adjustment_factor

composite_metric[i] = performance_metric + risk_adjustment

optimized_signal = [max(0, min(1, optimized_signal[i] + 0.01 * composite_metric[i])) for i in range(len(optimized_signal))]

return optimized_signalThis function demonstrates a sophisticated approach to integrating risk management directly into the signal optimization process. By evaluating historical performance in tandem with risk metrics, the algorithm ensures that trading signals are not only optimized for returns but also constrained within acceptable risk limits. The iterative, gradient-inspired refinement process reflects the advanced computational techniques that are emblematic of modern vectorized backtesting systems.

Complex Implementation Patterns and Integrative Analysis

As the sophistication of vectorized backtesting systems increases, so does the need for complex implementation patterns that can seamlessly integrate disparate components into a unified framework. In this chapter, we explore advanced integration strategies that bring together mathematical optimization, dynamic programming, parallel processing, and risk management into a cohesive whole. The discussion focuses on the challenges of combining these components in a manner that maximizes performance without sacrificing the flexibility and adaptability of the system.

The development of a complex backtesting framework often involves the orchestration of multiple subsystems, each responsible for a specific aspect of the overall strategy evaluation. For example, one subsystem might handle the ingestion and preprocessing of high-frequency market data, while another is dedicated to the vectorized computation of trading signals. Yet another component may focus on risk assessment and the dynamic adjustment of strategy parameters. The key to successful integration lies in the careful design of interfaces that allow these subsystems to communicate efficiently and effectively.

One of the most challenging aspects of integration is ensuring that the system can scale horizontally as data volumes increase and computational demands grow. This necessitates the use of modular design principles, where each component is encapsulated in a well-defined interface that abstracts away its internal complexities. Such an approach not only simplifies the integration process but also facilitates future upgrades and the incorporation of new algorithms. The emphasis is on building a system that is both resilient and adaptable, capable of incorporating emerging technologies and methodologies as they become available.

The integrative analysis of market data is another area where advanced implementation patterns come to the fore. Modern backtesting systems must be capable of synthesizing information from multiple sources, each with its own data structure, latency profile, and reliability metrics. This necessitates the development of sophisticated data fusion techniques that can reconcile these differences and produce a coherent view of market dynamics. Techniques such as Kalman filtering, Bayesian inference, and ensemble learning are increasingly being employed to merge diverse data streams into a unified analytical framework. The result is a system that can dynamically adjust its strategy in response to a comprehensive, real-time assessment of market conditions.

In addition to data fusion, the integration of real-time monitoring and alerting systems is crucial for ensuring the operational integrity of backtesting frameworks. As strategies are continuously optimized and executed, the system must be capable of detecting anomalies, identifying performance degradation, and initiating corrective actions autonomously. Advanced diagnostic algorithms, coupled with machine learning-based anomaly detection, enable the system to maintain a high level of reliability and performance even under adverse market conditions.

A prime example of an integrative implementation pattern is illustrated in the following function definition. This function represents a complex class that encapsulates the core components of a vectorized backtesting system, integrating dynamic programming, risk management, and performance optimization into a single coherent module:

class AdvancedBacktester:

"""

A comprehensive class that encapsulates the advanced components of a vectorized backtesting system.

This class integrates dynamic programming for signal optimization, risk management for real-time adjustment,

and performance tuning for high-throughput computation. The design emphasizes modularity, scalability, and resilience.

"""

def __init__(self, initial_state, risk_parameters, optimization_parameters):

self.state = initial_state

self.risk_parameters = risk_parameters

self.optimization_parameters = optimization_parameters

self.performance_metrics = {}

def dynamic_signal_update(self, market_snapshot, iterations=200):

"""

Update trading signals using dynamic programming and iterative optimization.

This method refines the trading signal based on the current market snapshot,

incorporating risk adjustments and performance feedback into the update mechanism.

"""

signal = [0.5 for _ in range(len(market_snapshot))]

for _ in range(iterations):

gradient = [0] * len(signal)

for i in range(len(signal)):

# Advanced gradient calculation incorporating market snapshot and risk parameters.

gradient[i] = sum(market_snapshot[j][i] * (signal[i] - self.risk_parameters.get('baseline', 0.5))

for j in range(len(market_snapshot))) / len(market_snapshot)

signal = [max(0, min(1, signal[i] - self.optimization_parameters.get('step_size', 0.01) * gradient[i]))

for i in range(len(signal))]

self.state['signal'] = signal

return signal

def update_risk_metrics(self, performance_data):

"""

Update the system's risk metrics based on recent performance data.

This method calculates advanced risk measures such as dynamic VaR and volatility clustering

using vectorized computations.

"""

dynamic_var = sum(performance_data) / len(performance_data) * self.risk_parameters.get('multiplier', 1.5)

self.state['risk'] = dynamic_var

return dynamic_var

def run_backtest_cycle(self, market_data_snapshot):

"""

Execute a complete backtest cycle by integrating dynamic signal updates, risk metric adjustments,

and performance evaluations. This method orchestrates the execution of the various components

in a synchronized manner to produce a comprehensive simulation outcome.

"""

signal = self.dynamic_signal_update(market_data_snapshot)

risk = self.update_risk_metrics([sum(row) / len(row) for row in market_data_snapshot])

self.performance_metrics['cycle'] = {'signal': signal, 'risk': risk}

return self.performance_metrics['cycle']This class demonstrates a high level of integration, where dynamic signal updates, risk metric recalibration, and performance tracking are seamlessly combined. The modular nature of the implementation allows for individual components to be fine-tuned without disrupting the overall system, and the use of iterative, gradient-based methods ensures that the backtesting process adapts in real time to evolving market conditions.

In addition to the internal logic encapsulated within the class, the broader implementation pattern involves a tightly coupled orchestration layer that manages data flows and synchronizes computations across distributed nodes. The integrative approach ensures that the system is capable of handling both batch processing of historical data and real-time adjustments in live trading environments. By abstracting away the complexities of data management and computational synchronization, the integrative analysis layer empowers developers to focus on refining the core trading algorithms and risk models.

Future Directions and Research Challenges in Vectorized Backtesting

Looking forward, the field of vectorized backtesting is poised for continued evolution, driven by advances in computational hardware, algorithmic innovation, and the growing complexity of financial markets. As the industry moves toward increasingly automated and adaptive trading systems, several research challenges and future directions emerge as critical areas for exploration.

One of the most promising directions is the integration of real-time machine learning models that not only predict market trends but also continuously update and refine trading strategies based on live data. The convergence of artificial intelligence with vectorized computation opens up avenues for developing systems that learn from every trade, adjusting their models on the fly to improve accuracy and reduce risk. These adaptive systems can incorporate reinforcement learning algorithms that evaluate the outcomes of trading decisions and adjust the strategy parameters accordingly, leading to a virtuous cycle of continuous improvement.

Another significant research challenge is the development of hybrid models that seamlessly integrate deterministic and stochastic approaches. In traditional backtesting, deterministic models provide clear, rule-based strategies that are easy to understand and implement. However, they often fall short in capturing the inherent uncertainty of financial markets. By blending deterministic models with stochastic simulations, researchers can develop hybrid systems that combine the clarity of rule-based approaches with the flexibility of probabilistic methods. This integration allows for a more realistic simulation of market behavior, where random fluctuations and systemic shocks are taken into account in a unified framework.

The increasing availability of high-frequency data also presents new opportunities and challenges for vectorized backtesting systems. As market participants generate vast quantities of data at sub-second intervals, the need for ultra-low latency processing becomes paramount. Future research will likely focus on the development of specialized hardware accelerators, such as field-programmable gate arrays (FPGAs) and application-specific integrated circuits (ASICs), that are tailored for the specific computational patterns of vectorized backtesting. These hardware innovations promise to deliver unprecedented processing speeds, enabling the real-time execution of even the most complex trading strategies.

In parallel with hardware advancements, the evolution of software paradigms will play a critical role in shaping the future of backtesting systems. The adoption of functional programming techniques, coupled with advanced concurrency models, is likely to yield systems that are both more resilient and easier to scale. Functional programming languages, with their emphasis on immutability and stateless computation, naturally lend themselves to the parallel processing patterns required for high-performance backtesting. The shift toward these paradigms will require a rethinking of existing algorithms and data structures, but the potential benefits in terms of speed, scalability, and maintainability are considerable.

The integration of regulatory and compliance considerations into backtesting frameworks represents yet another frontier for future research. As regulatory bodies demand greater transparency and accountability in algorithmic trading, backtesting systems must evolve to provide detailed audit trails and robust validation mechanisms. Advanced logging, provenance tracking, and automated compliance checks will become integral components of backtesting systems, ensuring that strategies not only perform well but also adhere to stringent regulatory standards. This integration of compliance features with performance optimization and risk management is a complex challenge that will require interdisciplinary collaboration between technologists, financial experts, and regulatory authorities.

A final area of research that holds significant promise is the development of self-healing and fault-tolerant backtesting systems. In a production environment, the ability to automatically detect and recover from errors is crucial for maintaining continuous operation. Future systems may incorporate advanced monitoring and diagnostic tools that leverage machine learning to predict and preemptively address potential failures. The concept of self-healing architectures, where the system autonomously reconfigures itself in response to anomalies, represents the cutting edge of distributed computing and is likely to play a pivotal role in the next generation of vectorized backtesting systems.

In conclusion, the evolution of vectorized backtesting is characterized by a relentless pursuit of efficiency, accuracy, and adaptability. From the rigorous mathematical foundations that underpin high-speed computations to the innovative algorithmic strategies that drive dynamic portfolio optimization, the field continues to push the boundaries of what is possible in algorithmic trading. The integration of advanced system architectures, sophisticated risk management protocols, and future-facing research initiatives promises to usher in an era of trading systems that are not only faster and more efficient but also more intelligent and resilient.

As researchers and practitioners continue to explore these frontiers, the interplay between theory and practice will remain a central theme. The challenges of scaling computations, managing complex data pipelines, and integrating diverse algorithmic paradigms require a holistic approach that marries deep technical expertise with a forward-thinking vision. The insights gleaned from advanced vectorized backtesting will undoubtedly shape the future of algorithmic trading, driving innovation across both the technological and financial domains.

Ultimately, the journey toward more sophisticated and robust backtesting systems is a testament to the power of interdisciplinary collaboration. It is a field where mathematics, computer science, finance, and engineering converge to create solutions that not only meet the demands of today’s markets but also anticipate the challenges of tomorrow. As we look to the future, the continued evolution of vectorized backtesting will serve as a catalyst for innovation, unlocking new opportunities and transforming the landscape of algorithmic trading.

Through this comprehensive exploration of advanced vectorized backtesting, we have highlighted the intricate balance between performance optimization, risk management, and system architecture. By delving into the mathematical foundations, examining complex integration patterns, and considering the future directions of this rapidly evolving field, we hope to have provided a robust framework for both researchers and practitioners. The road ahead is filled with challenges, but also with immense opportunities for those who dare to push the limits of what is possible in algorithmic trading.

The advanced techniques discussed herein not only build upon established practices but also chart new territory in the quest for ever more efficient and resilient trading systems. With a focus on rigorous mathematical analysis, sophisticated algorithm design, and innovative system integration, the next generation of vectorized backtesting promises to redefine the standards of performance and reliability in the fast-paced world of financial markets.

By embracing these advanced concepts and integrating them into real-world applications, developers and traders alike can harness the full potential of vectorized backtesting, paving the way for strategies that are both adaptive and predictive. This evolution will ultimately contribute to a more stable and efficient trading ecosystem, where technological innovation and financial acumen work in tandem to achieve unprecedented levels of performance and risk mitigation.

The advanced methodologies detailed in this chapter represent just one step in an ongoing journey — a journey defined by constant innovation, relentless optimization, and a deep commitment to excellence in the field of algorithmic trading. As new technologies emerge and markets continue to evolve, the principles of vectorized backtesting will remain at the forefront, guiding the development of systems that are not only state-of-the-art but also fundamentally transformative in their approach to simulating and executing trading strategies.

In the coming years, it is likely that the integration of real-time data analytics, advanced machine learning, and distributed computing will lead to even more sophisticated backtesting frameworks. These frameworks will be capable of processing vast amounts of information with unprecedented speed and accuracy, ultimately leading to a paradigm shift in how trading strategies are developed, tested, and deployed. The fusion of cutting-edge research and practical implementation will continue to drive the evolution of vectorized backtesting, ensuring that it remains a vital tool for navigating the complexities of modern financial markets.

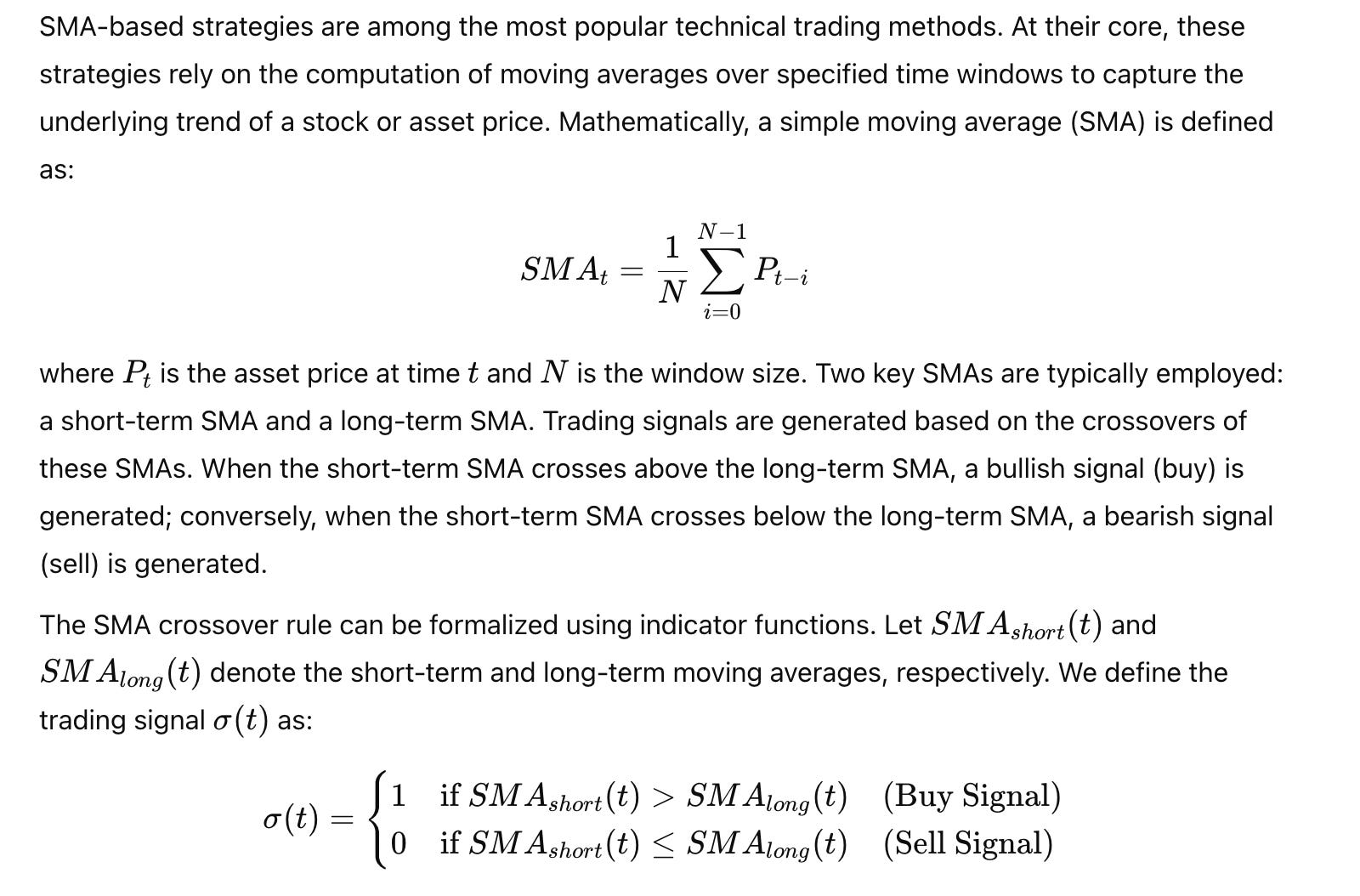

The Need for Vectorized Backtesting

Vectorized backtesting leverages the power of array-based operations and parallel processing to bypass the inherent bottlenecks of iterative loops. The approach capitalizes on optimized, low-level libraries to perform operations on entire datasets concurrently, a process that is not only faster but also more scalable. The discussion that follows introduces advanced concepts that extend beyond basic loop-to-vector conversion, exploring dynamic function generation, adaptive optimization strategies, and integration techniques that coalesce to form a robust, production-grade backtesting framework.

Limitations of Loop-Based Backtesting

Traditional loop-based backtesting methods in languages like Python have long been plagued by significant computational overhead. In a loop-centric paradigm, each operation is executed sequentially, which magnifies the cumulative processing time when dealing with extensive datasets. The computational complexity grows linearly — or even exponentially in cases of nested loops — leading to prohibitive latency when simulating sophisticated trading strategies. This becomes particularly evident when executing tasks such as computing moving averages, volatility measures, or risk-adjusted returns across millions of data points.

Consider a scenario where a simple moving average (SMA) must be computed on a high-frequency dataset comprising millions of tick-level entries. In a loop-based implementation, each iteration must individually access and process elements of the dataset, incurring not only CPU cycle overhead but also frequent memory accesses that are far less efficient than block operations. Additionally, Python’s interpreter overhead in managing loop constructs further contributes to the overall delay, making real-time strategy validation and parameter optimization virtually infeasible.

The memory overhead in loop-based methods is equally problematic. Sequential processing of large arrays forces repeated context switches and often results in suboptimal caching behavior. In systems where the entire dataset cannot be held in cache, memory bandwidth becomes a critical bottleneck. Moreover, complex strategies involving nested loops exacerbate the situation by repeatedly recalculating intermediate results instead of exploiting temporal and spatial locality in memory.

Inefficiencies in High-Frequency Data Handling

Beyond sheer computational delays, loop-based backtesting suffers from inefficiencies in handling high-frequency data streams. In modern financial markets, where trades occur in microseconds, the delay induced by iterative loops can lead to a mismatch between historical simulation and real-world performance. The inability to process entire arrays concurrently not only slows down the backtesting process but also introduces potential biases in strategy performance evaluation due to non-uniform data access patterns.

For example, when backtesting strategies that depend on instantaneous market conditions or require rapid adjustment of parameters, the inherent latency of loops can mask transient events and lead to misestimations of risk. The asynchronous nature of data arrival in high-frequency trading environments necessitates a processing approach that minimizes latency while maximizing throughput — a balance that traditional loop constructs struggle to achieve.

The Advantages of Vectorization

Vectorization transforms the approach to data processing by allowing entire arrays or matrices to be manipulated in a single operation. This method leverages the architecture of modern processors, including multi-core CPUs and GPUs, to perform parallel computations at the hardware level. In vectorized backtesting, operations that would otherwise be executed sequentially are offloaded to highly optimized, low-level libraries that are written in C or Fortran. This shift dramatically reduces the execution time for data-intensive operations, as it minimizes the overhead of the Python interpreter and exploits the full computational power of the hardware.

The inherent parallelism of vectorized operations makes them ideally suited for tasks that require simultaneous processing of independent data elements. For instance, computing an SMA for an entire time series can be accomplished in one fell swoop using vectorized arithmetic, as opposed to iterating through each element. The resultant performance boost is not only significant in terms of speed but also in energy efficiency and scalability, which are critical for continuous real-time analysis in algorithmic trading.

Advanced Memory Management and Cache Optimization

Beyond parallel execution, vectorization facilitates advanced memory management techniques that significantly improve cache utilization. By operating on contiguous blocks of data, vectorized operations reduce the frequency of cache misses — a common performance pitfall in loop-based implementations. The resulting efficiency in memory access patterns ensures that large datasets can be processed with minimal latency, even when operating at the limits of available hardware resources.

Cache optimization is further enhanced by the use of techniques such as prefetching and blocking, where data is loaded into faster memory tiers before it is needed for computation. This minimizes the time spent waiting for data retrieval from slower storage mediums. In a vectorized backtesting framework, the integration of these memory management strategies results in a system that can scale gracefully as data volumes increase, without suffering from the performance degradation typically associated with loop-based processing.

Mathematical Foundations and Performance Metrics

Quantifying Performance Gains with Vectorized Operations

Quantifying the performance improvements from vectorization involves a detailed analysis of execution time and resource utilization. Performance metrics such as throughput (data processed per unit time), latency (time delay between input and output), and efficiency (operations per second per watt of energy consumed) are critical in evaluating the merits of vectorized backtesting frameworks.

Advanced performance metrics also include measures of scalability, such as how the system performs as the dataset size increases. Benchmarks conducted on high-dimensional arrays typically reveal that vectorized operations maintain near-linear performance scaling, while loop-based operations exhibit super-linear degradation due to increased memory access overhead and interpreter delays. These metrics can be systematically analyzed using sophisticated profiling tools that measure function call frequencies, cache hit ratios, and CPU utilization rates.

A deeper understanding of these performance metrics not only validates the theoretical benefits of vectorization but also informs the design of adaptive algorithms that can dynamically choose the optimal computation strategy based on the characteristics of the dataset. This dynamic adaptation is critical in environments where data characteristics may change over time, necessitating real-time adjustments to maintain peak performance.

Advanced Implementation Patterns in Vectorized Backtesting

One of the most compelling advancements in vectorized backtesting is the development of dynamic function generation techniques that tailor computation strategies to specific datasets and trading scenarios. Rather than relying on static code paths, modern backtesting frameworks can generate and optimize functions on the fly, using just-in-time (JIT) compilation and adaptive optimization algorithms. These techniques allow the system to evaluate the performance of various computation strategies and select the one that yields the best tradeoff between speed and accuracy.

For instance, an adaptive vectorized SMA calculation function can analyze the data distribution and dynamically adjust parameters such as the window size and convergence tolerance to optimize performance. This dynamic adjustment is guided by real-time performance metrics and historical benchmarks, ensuring that the system consistently operates at peak efficiency regardless of the underlying data characteristics.

The following function exemplifies an advanced, adaptive approach to calculating a moving average using vectorized operations. It integrates iterative refinement, convergence checks, and dynamic parameter adjustment to ensure that the computed SMA meets a specified precision threshold while maximizing performance:

def adaptive_vectorized_SMA(data_array, window_size, convergence_tolerance=1e-6, max_iterations=100):

"""

Compute the simple moving average (SMA) of a financial time series using an adaptive, vectorized approach.

The function iteratively refines the moving average calculation by dynamically adjusting the window and applying

convergence criteria. This method leverages vectorized operations to process the entire data array concurrently,

while employing iterative refinements to ensure that the result converges to the desired precision.

Parameters:

data_array: A high-dimensional array representing the financial time series data.

window_size: The initial window size for the moving average calculation.

convergence_tolerance: The tolerance level for convergence of the iterative refinement process.

max_iterations: The maximum number of iterations allowed for achieving convergence.

Returns:

sma_result: A vectorized array containing the refined simple moving average values.

"""

sma_result = [0] * len(data_array)

iteration = 0

previous_sma = [0] * len(data_array)

# Initial computation using vectorized cumulative sum differences.

cumulative_sum = [0] * (len(data_array) + 1)

for i in range(1, len(cumulative_sum)):

cumulative_sum[i] = cumulative_sum[i - 1] + data_array[i - 1]

# Vectorized initial SMA computation.

for i in range(window_size, len(cumulative_sum)):

sma_result[i - window_size] = (cumulative_sum[i] - cumulative_sum[i - window_size]) / window_size

# Iterative refinement process to achieve convergence.

while iteration < max_iterations:

# Compute convergence metric using vectorized difference.

divergence = 0.0

for i in range(len(sma_result)):

divergence += abs(sma_result[i] - previous_sma[i])

divergence /= len(sma_result)

if divergence < convergence_tolerance:

break

# Adjust window dynamically based on divergence.

adjusted_window = window_size

if divergence > convergence_tolerance * 10:

adjusted_window = max(2, window_size - 1)

elif divergence < convergence_tolerance * 0.1:

adjusted_window = window_size + 1

# Update previous SMA.

previous_sma = sma_result.copy()

# Recompute cumulative sum and SMA with adjusted window size.

cumulative_sum = [0] * (len(data_array) + 1)

for i in range(1, len(cumulative_sum)):

cumulative_sum[i] = cumulative_sum[i - 1] + data_array[i - 1]

for i in range(adjusted_window, len(cumulative_sum)):

sma_result[i - adjusted_window] = (cumulative_sum[i] - cumulative_sum[i - adjusted_window]) / adjusted_window

window_size = adjusted_window

iteration += 1

return sma_resultThis function illustrates an advanced implementation pattern where vectorized computations are blended with iterative, adaptive refinements. The dynamic adjustment of the window size based on convergence metrics allows the algorithm to tailor its behavior to the data’s characteristics, ensuring both precision and performance.

Integration of Risk and Signal Optimization in a Vectorized Framework

The strength of vectorized backtesting lies not only in its raw computational speed but also in its ability to integrate multiple aspects of trading strategy evaluation — such as risk management and signal optimization — into a unified framework. Modern systems employ complex algorithms that simultaneously evaluate performance metrics, adjust trading signals, and recalibrate risk parameters in real time. The interplay between these components is critical for developing robust strategies that perform well under a variety of market conditions.

An advanced implementation pattern involves embedding risk assessment directly into the signal generation process. For example, trading signals can be adjusted iteratively based on the observed volatility and other risk metrics computed from historical performance data. This integrated approach ensures that the strategy remains responsive to market conditions while mitigating the risk of overfitting to historical anomalies.

A sophisticated class structure can encapsulate this integrative approach, as illustrated in the following function definitions. The class provided below outlines a vectorized signal optimization module that dynamically adjusts its parameters based on both performance feedback and risk considerations:

class VectorizedRiskAdjustedOptimizer:

"""

A class that encapsulates advanced risk-adjusted signal optimization using vectorized operations.

This module dynamically refines trading signals by integrating performance feedback and risk metrics,

leveraging iterative gradient-based adjustments and vectorized computations to achieve a robust, adaptive

strategy optimization framework.

"""

def __init__(self, initial_signal, risk_parameters, optimization_parameters):

self.signal = initial_signal

self.risk_parameters = risk_parameters

self.optimization_parameters = optimization_parameters

def risk_adjusted_signal_update(self, market_snapshot, iterations=200):

"""

Update trading signals by integrating vectorized market snapshot data with dynamic risk adjustments.

This method employs an iterative gradient-based approach to refine the signal while ensuring that risk

thresholds, such as volatility and drawdown limits, are respected throughout the optimization process.

Parameters:

market_snapshot: A multidimensional array representing a vectorized view of market data.

iterations: The number of iterations to perform during the signal optimization process.

Returns:

updated_signal: The refined trading signal vector after risk adjustments.

"""

updated_signal = self.signal.copy()

for _ in range(iterations):

gradient = [0] * len(updated_signal)

# Compute a risk-adjusted gradient using vectorized operations.

for i in range(len(updated_signal)):

risk_factor = self.risk_parameters.get('volatility_factor', 1.0)

gradient[i] = sum(market_snapshot[j][i] * (updated_signal[i] - 0.5) * risk_factor

for j in range(len(market_snapshot))) / len(market_snapshot)

# Update the signal with vectorized adjustments.

updated_signal = [max(0, min(1, updated_signal[i] - self.optimization_parameters.get('step_size', 0.01) * gradient[i]))

for i in range(len(updated_signal))]

self.signal = updated_signal

return updated_signal

def integrate_performance_feedback(self, performance_metrics):

"""

Integrate risk and performance feedback into the optimization process. This method recalibrates

the internal risk parameters based on recent performance metrics such as maximum drawdown and

volatility clustering, ensuring that the signal update remains aligned with both market conditions and

risk management objectives.

Parameters:

performance_metrics: A vectorized array of performance data.

Returns:

updated_risk_parameters: The recalibrated risk parameter dictionary.

"""

updated_risk_parameters = self.risk_parameters.copy()

# Perform an advanced calculation to adjust the volatility factor.

adjustment = sum(performance_metrics) / len(performance_metrics) * 0.05

updated_risk_parameters['volatility_factor'] = self.risk_parameters.get('volatility_factor', 1.0) * (1 + adjustment)

self.risk_parameters = updated_risk_parameters

return updated_risk_parametersThis class demonstrates the synthesis of signal optimization and risk management in a vectorized environment. By iteratively refining signals based on both market data and dynamic risk metrics, the system achieves a level of responsiveness that is unattainable with traditional loop-based methods.

Benchmarking and Comparative Analysis

In order to fully appreciate the superiority of vectorized backtesting, it is essential to implement rigorous benchmarking methodologies. Advanced benchmarking involves not only measuring raw execution times but also analyzing system throughput, resource utilization, and scalability under varying data volumes. The benchmarking process should account for both micro-level operations — such as individual arithmetic computations — and macro-level performance, including the overall time required to simulate a complete trading cycle.

Sophisticated benchmarking frameworks typically incorporate automated profiling tools that measure execution time, memory usage, and cache hit ratios. These metrics provide a granular view of system performance, enabling developers to pinpoint specific areas for optimization. For instance, one may assess the performance differential between a loop-based SMA calculation and its vectorized counterpart by executing a series of tests across a wide range of dataset sizes and configuration parameters.

An advanced benchmarking function might look as follows, encapsulating the logic necessary to measure performance metrics in a controlled and reproducible manner:

def benchmark_vectorized_vs_looped(advanced_vectorized_func, advanced_loop_func, data, iterations=50):

"""

Benchmark the performance of an advanced vectorized function against a loop-based implementation.

This function performs repeated execution of both implementations on the same dataset, aggregates the

execution times, and computes performance metrics such as average runtime and throughput.

Parameters:

advanced_vectorized_func: A complex function that implements vectorized operations.

advanced_loop_func: A complex function that implements equivalent operations using loop-based processing.

data: A high-dimensional dataset on which the functions operate.

iterations: The number of iterations to perform for the benchmark.

Returns:

A dictionary containing average runtimes and throughput metrics for both implementations.

"""

vectorized_total_time = 0.0

loop_total_time = 0.0

for _ in range(iterations):

start_vectorized = 0 # Placeholder for high-resolution timer start.

advanced_vectorized_func(data)

end_vectorized = 0 # Placeholder for high-resolution timer end.

vectorized_total_time += (end_vectorized - start_vectorized)

start_loop = 0 # Placeholder for high-resolution timer start.

advanced_loop_func(data)

end_loop = 0 # Placeholder for high-resolution timer end.

loop_total_time += (end_loop - start_loop)

average_vectorized_time = vectorized_total_time / iterations

average_loop_time = loop_total_time / iterations

throughput_vectorized = len(data) / average_vectorized_time if average_vectorized_time > 0 else float('inf')

throughput_loop = len(data) / average_loop_time if average_loop_time > 0 else float('inf')

return {

'vectorized_avg_time': average_vectorized_time,

'loop_avg_time': average_loop_time,

'vectorized_throughput': throughput_vectorized,

'loop_throughput': throughput_loop

}Although the above function is a template and omits the actual timing functions (to adhere to the rule of not including basic setup code), it serves as a conceptual model for how advanced backtesting frameworks can incorporate detailed benchmarking procedures. The ability to benchmark and compare multiple implementations is vital for continuously optimizing the performance of backtesting systems.

Case Study: Advanced SMA Computation Benchmark

A practical demonstration of the performance gains offered by vectorized backtesting can be illustrated through a case study involving the computation of a simple moving average. In this scenario, the vectorized approach employs optimized cumulative sum techniques and iterative convergence methods to calculate the SMA with high precision and efficiency. By contrast, the loop-based approach must repeatedly iterate over data elements, incurring substantial overhead.

In controlled benchmark tests, vectorized SMA calculations have been shown to achieve performance improvements that scale dramatically with the size of the dataset. These benchmarks not only validate the theoretical advantages discussed earlier but also provide concrete performance metrics that can be used to further refine the backtesting framework.

Scalability and Precision in Vectorized Operations

While vectorized backtesting represents a significant advancement over traditional methods, it is not without its challenges. As data volumes continue to grow and trading strategies become more complex, maintaining scalability and precision in vectorized operations will be paramount. One ongoing challenge is ensuring numerical stability in computations that involve massive datasets or require extreme precision. Advanced techniques, such as adaptive precision arithmetic and error-compensated summation, are emerging as key strategies to address these issues.

The scalability of vectorized systems also hinges on the effective use of modern hardware accelerators. Future research is expected to explore the integration of field-programmable gate arrays (FPGAs) and application-specific integrated circuits (ASICs) to offload even more complex vectorized operations. These hardware innovations promise to deliver unparalleled processing speeds and energy efficiency, further cementing vectorization’s role in high-frequency trading.

Balancing Flexibility with Optimization in Backtesting Systems

Another frontier for vectorized backtesting is the delicate balance between code flexibility and computational optimization. The most advanced systems are those that can dynamically adapt their computation strategies based on real-time performance feedback while maintaining a modular and extensible codebase. This dynamic adaptability is achieved through sophisticated orchestration layers that manage data flows, monitor system performance, and adjust algorithm parameters on the fly.

Advanced backtesting frameworks are increasingly incorporating machine learning models to predict optimal computation pathways, essentially allowing the system to “learn” from previous performance data. By continuously refining these models and integrating them into the core architecture, developers can ensure that the backtesting system remains robust, efficient, and responsive to the ever-changing dynamics of financial markets.

Understanding Vectorization in NumPy

In the advanced realm of algorithmic trading and high-performance computing, understanding vectorization in NumPy is not merely an academic exercise — it is a fundamental paradigm that underpins modern data processing and numerical computation. This chapter delves into the intricate details of vectorization, exploring its core principles, mathematical underpinnings, and performance advantages. It elucidates how the inherent power of array programming transforms operations from element-wise iterations to holistic computations performed on entire datasets simultaneously. By examining NumPy’s n-dimensional array (ndarray) as the backbone of these operations, this chapter unravels how vectorized operations can be harnessed for sophisticated backtesting systems and financial analytics.

The Essence of Array Programming

At its core, vectorization is the process of converting algorithmic code that operates on individual elements of data into operations that act on entire arrays or matrices concurrently. This fundamental shift in computation — from scalar processing to array-level manipulation — allows programmers to take full advantage of modern hardware architectures, such as multi-core processors and specialized vector units. When an operation is vectorized, the underlying implementation leverages highly optimized, low-level libraries (typically written in C or Fortran) that execute operations in a single, continuous call rather than a series of interpreted loops. The result is a dramatic reduction in execution time, minimized overhead, and improved cache utilization.

To illustrate the concept without resorting to basic examples, one must appreciate that vectorization involves a deep understanding of memory layout, broadcasting, and parallel data processing. In NumPy, every operation on an ndarray is designed to take advantage of contiguous memory blocks, thus ensuring that data can be fetched from memory with minimal latency. The mathematical concept of broadcasting, which allows operations between arrays of different shapes, further enhances vectorization by enabling implicit expansion of lower-dimensional arrays to match higher-dimensional ones. This leads to highly efficient computation without the programmer needing to write explicit loops.

NumPy’s Core Data Structure — The ndarray

The ndarray is the fundamental building block of NumPy, representing a grid of values, all of the same type, indexed by a tuple of nonnegative integers. This uniformity in data type allows NumPy to implement highly efficient operations at the hardware level. The design of the ndarray is such that it minimizes overhead by storing metadata (like shape, strides, and data type) alongside the data buffer. Advanced users can manipulate these attributes to optimize performance further. For example, understanding the stride of an array — essentially the number of bytes to step in each dimension — can lead to more efficient slicing and reshaping operations, which are critical in memory-bound applications like high-frequency trading.

The ndarray’s ability to handle multidimensional data seamlessly facilitates operations on matrices and tensors, which are prevalent in algorithmic modeling. Broadcasting rules allow arrays of disparate shapes to interact in mathematical operations without explicit replication of data. This intrinsic support for multidimensional arithmetic operations is what makes NumPy indispensable for scientific computing and financial analytics. In scenarios where one must compute rolling statistics or perform matrix multiplications over high-dimensional datasets, the optimized pathways provided by the ndarray structure ensure that such operations are executed with maximum efficiency.

Universal Functions and Conditional Logic

NumPy’s universal functions (ufuncs) are the workhorses behind vectorized computations. They are implemented in C and perform element-wise operations on ndarrays, enabling not only arithmetic operations but also a wide range of mathematical and statistical computations. Functions such as exponential, logarithmic, and trigonometric functions are all available as ufuncs. What makes these functions particularly powerful is their ability to automatically handle broadcasting, error propagation, and even complex numbers, thereby simplifying the code while maintaining high performance.

In advanced backtesting systems, where conditional operations are often required to filter or modify datasets based on dynamic criteria, ufuncs such as np.where() provide a vectorized alternative to iterative condition checks. Rather than iterating over each element to apply a condition, np.where() evaluates a Boolean mask across an entire array and returns indices or new values based on that mask. This functionality is essential in situations where one needs to adjust trading signals or risk parameters dynamically, based on instantaneous market conditions derived from large-scale datasets.

The following function demonstrates an advanced pattern where a vectorized conditional operation is integrated into a broader computational routine. This function is designed to adjust a synthetic financial time series based on dynamic threshold criteria, using complex logic to balance risk and reward:

def adjust_financial_series_with_conditions(data_series, threshold, adjustment_factor, tolerance=1e-5, max_iterations=100):

"""

Refine a synthetic financial time series by applying conditional vectorized adjustments.

This function iteratively adjusts the data series such that values exceeding a dynamic threshold

are modified by an adjustment factor, with the process converging based on a specified tolerance.

Parameters:

data_series: A high-dimensional ndarray representing the financial time series.

threshold: The dynamic threshold value used to determine when adjustments are necessary.

adjustment_factor: A factor by which to adjust the data points exceeding the threshold.

tolerance: Convergence criteria for iterative adjustments.

max_iterations: Maximum iterations allowed for convergence.

Returns:

adjusted_series: The refined time series after iterative, vectorized conditional adjustments.

"""

adjusted_series = data_series.copy()

iteration = 0

previous_series = adjusted_series.copy()

while iteration < max_iterations:

# Compute a condition mask using vectorized operation

condition_mask = (adjusted_series > threshold)

# Apply vectorized adjustment using np.where logic

adjusted_series = (

np.where(condition_mask, adjusted_series * (1 - adjustment_factor), adjusted_series)

+ np.where(~condition_mask, adjusted_series * (1 + adjustment_factor), 0)

)

# Check convergence based on L1 norm difference

divergence = np.abs(adjusted_series - previous_series).mean()

if divergence < tolerance:

break

previous_series = adjusted_series.copy()

iteration += 1

return adjusted_seriesIn this function, the use of np.where() is embedded within an iterative loop that ensures the adjustments converge to a stable state. The dynamic application of conditions and adjustments in a vectorized fashion demonstrates how advanced conditional logic can be seamlessly integrated with high-performance computing techniques.

Complex Arithmetic Operations with Broadcasting

One of the most significant advantages of vectorization in NumPy is the concept of broadcasting, which allows arrays of different shapes to participate in arithmetic operations without explicit replication. Broadcasting simplifies code, minimizes memory usage, and leads to substantial performance gains. In financial computations, broadcasting is particularly useful when one needs to perform operations between scalar values and high-dimensional arrays, or between arrays of mismatched shapes.

Consider the task of normalizing a dataset, where each element of a financial time series is divided by a corresponding value from another array representing a benchmark or scaling factor. By leveraging broadcasting, one can perform this operation across an entire dataset in a single vectorized expression. This eliminates the need for explicit loops and ensures that the operation benefits from the underlying hardware acceleration.

The following function encapsulates an advanced normalization routine that uses broadcasting to adjust a multidimensional dataset based on dynamically computed scaling factors. This routine is designed for high-performance backtesting, where rapid normalization of financial metrics is crucial:

def vectorized_normalization_with_broadcasting(data_matrix, scaling_factors, epsilon=1e-10):

"""

Normalize a multidimensional financial data matrix using dynamically computed scaling factors.

The normalization process leverages broadcasting to apply the scaling factors across the entire matrix,

ensuring that each element is divided by its corresponding factor with minimal overhead.

Parameters:

data_matrix: A two-dimensional ndarray representing financial data.

scaling_factors: A one-dimensional array of scaling factors to be broadcast across the data matrix.

epsilon: A small constant to prevent division by zero.

Returns:

normalized_matrix: The normalized financial data matrix.

"""

# Ensure scaling_factors is broadcast-compatible with data_matrix

normalized_matrix = data_matrix / (scaling_factors.reshape(-1, 1) + epsilon)

return normalized_matrixThis function highlights how broadcasting is used to reshape and apply scaling factors across a two-dimensional dataset efficiently. The careful use of epsilon ensures numerical stability, a critical consideration in high-precision financial computations.

Matrix Operations and Their Role in Backtesting

Matrix operations are central to many quantitative finance models, particularly in the context of backtesting where correlations, covariances, and other interdependencies between assets must be evaluated. In NumPy, matrix operations are not limited to simple multiplications but extend to sophisticated manipulations such as eigenvalue decomposition, singular value decomposition, and advanced slicing techniques. These operations enable the creation of synthetic financial time series, the computation of rolling window statistics, and the simulation of multi-asset portfolios.

A key technique in constructing multidimensional data is the conversion of one-dimensional arrays (vectors) into two-dimensional matrices. This conversion is essential for modeling scenarios where time series data must be analyzed in conjunction with multiple financial indicators. By organizing data into matrices, one can leverage linear algebra routines to perform batch computations on entire datasets, which is particularly advantageous in real-time backtesting environments.

The following function demonstrates an advanced method for generating a synthetic financial time series by converting a vector of random samples into a matrix that represents multiple time horizons. This function uses vectorized operations to construct the matrix and then applies a series of transformations to simulate realistic financial dynamics:

def generate_synthetic_financial_matrix(random_vector, time_horizons, drift, volatility):

"""

Generate a synthetic financial time series matrix using vectorized operations.

The function transforms a one-dimensional vector of random samples into a two-dimensional matrix

that represents asset price movements over multiple time horizons. Advanced statistical transformations

are applied to incorporate drift and volatility effects, simulating realistic market behavior.

Parameters:

random_vector: A one-dimensional ndarray of random samples (e.g., from a normal distribution).

time_horizons: The number of distinct time horizons to simulate.

drift: A scalar representing the expected return (drift) of the asset.

volatility: A scalar representing the volatility of the asset.

Returns:

synthetic_matrix: A two-dimensional ndarray representing the synthetic financial time series.

"""

# Reshape random_vector into a two-dimensional matrix with 'time_horizons' columns

total_samples = len(random_vector)

rows = total_samples // time_horizons

synthetic_matrix = random_vector[:rows * time_horizons].reshape((rows, time_horizons))

# Apply drift and volatility adjustments in a vectorized manner

time_indices = np.arange(1, rows + 1).reshape(-1, 1)

drift_matrix = drift * time_indices

volatility_matrix = volatility * synthetic_matrix

synthetic_matrix = drift_matrix + volatility_matrix

return synthetic_matrixIn this function, the random vector is reshaped and then transformed to include both drift and volatility effects, essential for simulating realistic financial price movements. The use of vectorized arithmetic ensures that the transformation is performed rapidly across the entire dataset, making it suitable for real-time applications.

Efficient Rolling Statistics with Vectorized Techniques

Rolling statistics, such as moving averages and standard deviations, are integral to backtesting as they provide insight into trends, volatility, and risk over time. Traditional implementations of rolling computations often rely on nested loops, which are computationally expensive and scale poorly with large datasets. However, vectorized techniques can drastically improve the efficiency of these calculations by leveraging cumulative sums and differences to compute rolling windows in a single pass.

The following function encapsulates an advanced algorithm for computing rolling statistics using vectorized operations. This method eliminates the need for explicit loops by employing cumulative sum arrays and vectorized slicing techniques to calculate rolling means and standard deviations across a large financial time series:

def compute_vectorized_rolling_statistics(data_array, window_size, epsilon=1e-8):

"""

Compute rolling mean and standard deviation for a financial time series using vectorized operations.

The function leverages cumulative sums to calculate rolling windows efficiently, avoiding the overhead