Quantitative Trading Model from Paper to Python: Building an Attention-BiLSTM Strategy for Gold and Bitcoin

A step-by-step tutorial on translating academic paper concepts—including temporal attention, streak-based position sizing, and greedy portfolio optimization—into production-ready Python code.

What This Article Builds

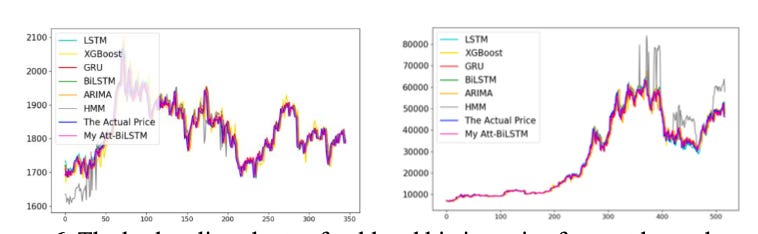

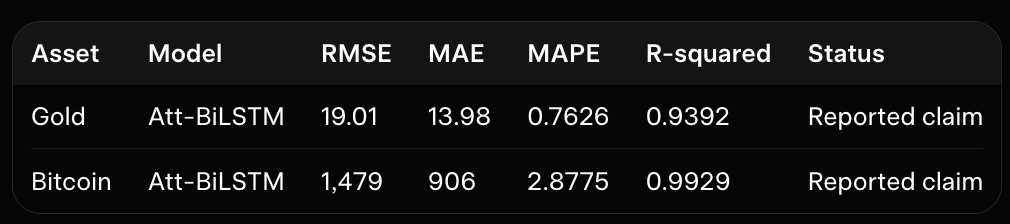

The paper proposes a quantitative trading pipeline for gold and Bitcoin. It combines price forecasting with an attention-enhanced bidirectional LSTM, position sizing based on empirical consecutive rises and declines, transaction-cost sensitivity analysis, and claimed use of VaR and a modified greedy algorithm for trading decisions. Several benchmark forecasting models are compared, with Att-BiLSTM reported as the best predictor. The trading results claim a final value of approximately $646 for a $500 gold allocation and $215,487 for a $500 Bitcoin allocation, although the backtest protocol and several model details are insufficiently specified.

The code is my implementation based on what the paper discusses. Download the source code using the button at the end of this article!

Also the code might have some errors, because I didn’t found anything online related to paper, everything is implemented by myself, so download it and understand. With article and the code.

This is the research paper I tried to implement: https://www.researchgate.net/publication/364569615_Research_on_Quantitative_Trading_Model

Our Book is out on openclaw:

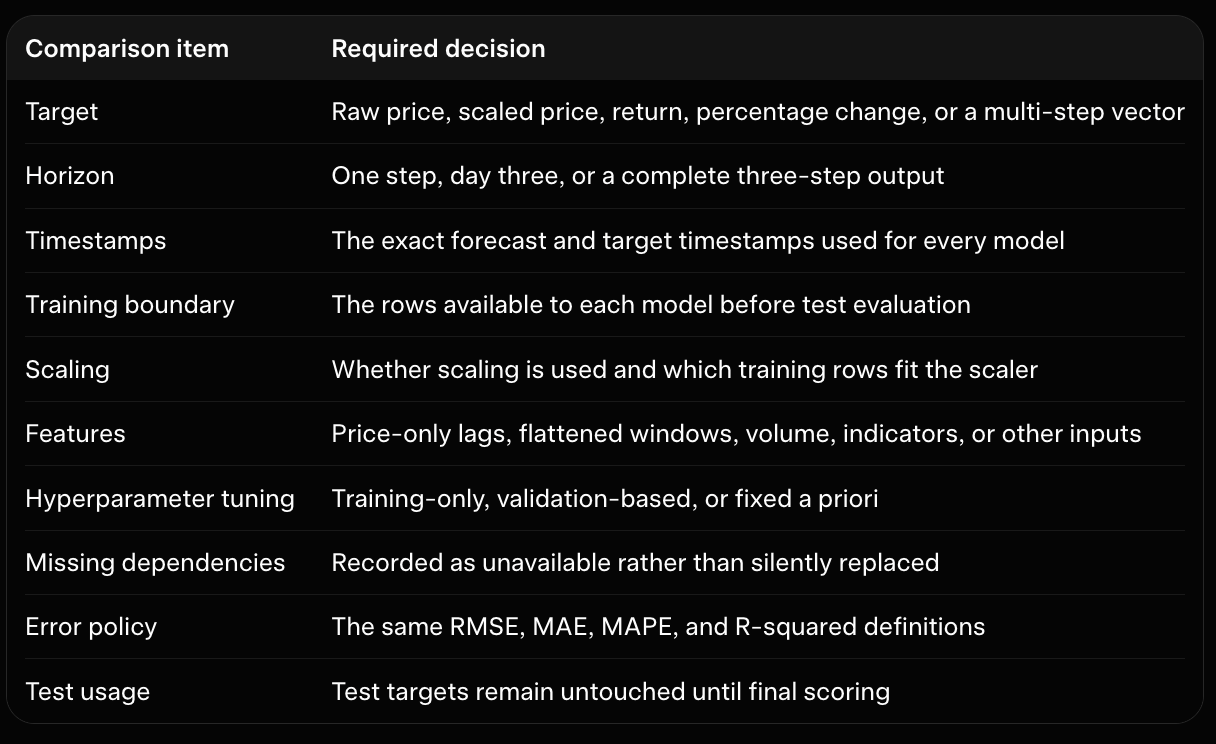

Implementation Assumptions

Historical gold and Bitcoin datasets are not supplied; the implementation will accept local CSV or pandas DataFrame inputs and include a deterministic synthetic-data generator for demonstrations only.

Prices are assumed to be positive, chronologically ordered observations with one row per asset and an explicit timestamp.

Standard simple return, (pt-p{t-1})/p_{t-1}, is used by default because the paper's printed denominator is ambiguous; the choice is configurable and documented.

The primary target is a one-step-ahead normalized price or return forecast. A three-step vector forecast option is supported because the paper's conclusion mentions three-day forecasts.

The primary forecasting model is an attention-enhanced BiLSTM with a configurable learned query vector, 20% dropout, MAE loss, and RMSprop optimizer.

The paper-style 70:30 chronological split is supported for comparison, while walk-forward evaluation is the preferred protocol for trading conclusions.

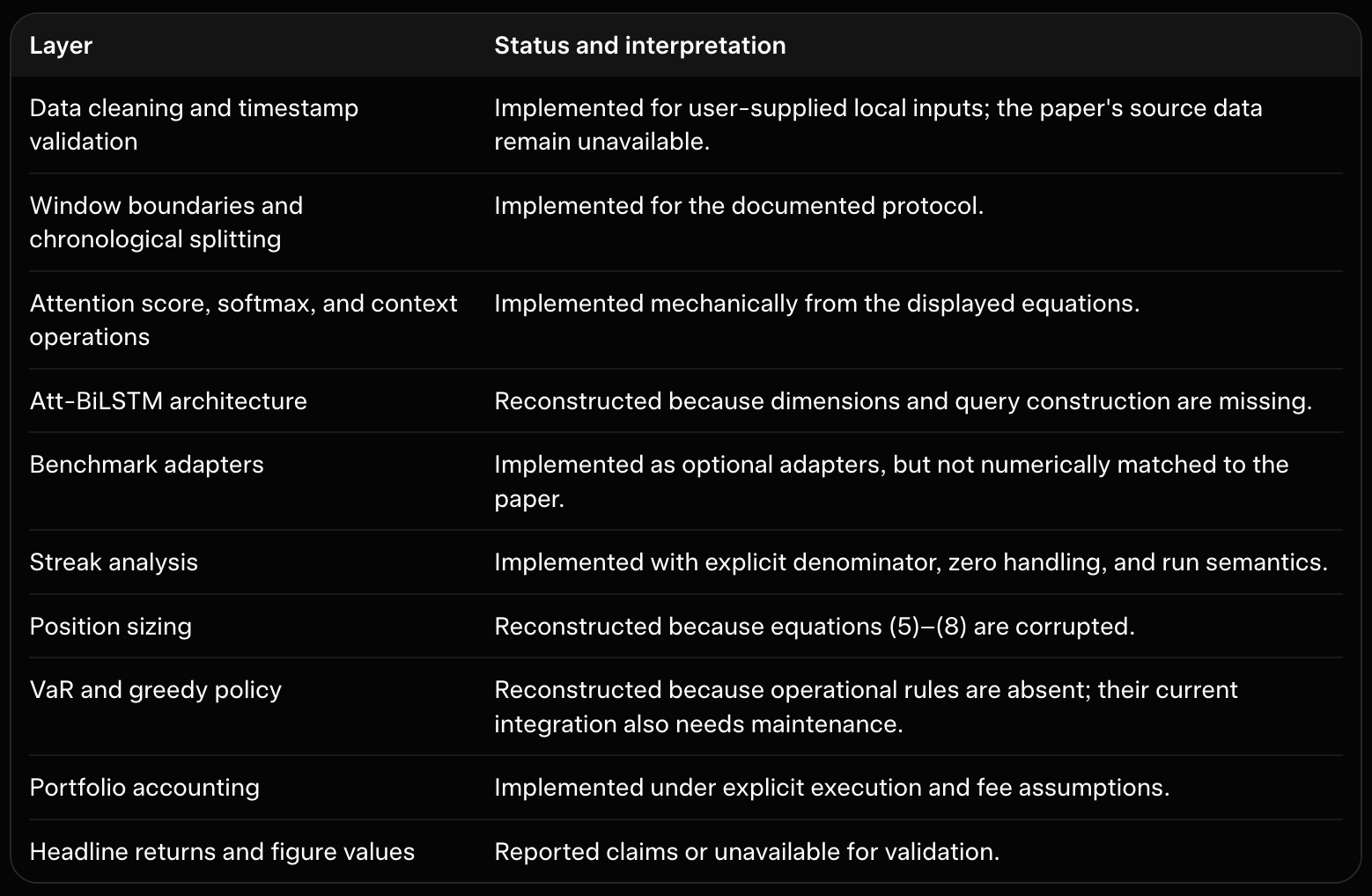

Equations (5) through (8), VaR operation, and the modified greedy algorithm are implemented as explicit reconstructions and will never be presented as exact reproductions.

Transaction fees apply to both buys and sells by default, use decimal rates such as 0.002 for 0.2%, and are configurable.

The backtest uses next-bar execution after a signal, finite position-addition levels, no leverage by default, and optional slippage.

The reported final values of approximately 646 USD for gold and 215487 USD for Bitcoin are recorded as unverified reference claims rather than expected test outputs.

Deep-learning, statistical, and optional benchmark dependencies are isolated so core data, sizing, risk, and backtesting components remain usable without every optional package installed.

1. The Paper’s Core Idea: Forecast Timing and Manage Position Size Separately

The paper is trying to answer two different trading questions:

When should the strategy trade?

How much capital should it deploy when it trades?

Those questions are related, but they are not the same problem. A forecasting model can estimate that gold or Bitcoin may rise, yet it does not automatically determine whether the strategy should invest $10, $100, or the entire available budget. Conversely, a position-sizing rule can specify how much to buy after a decline, but it needs a signal to decide whether buying is appropriate at that moment.

The implementation keeps these responsibilities separate. The forecasting component produces information about a possible future price. The signal layer converts that forecast into a buy, sell, add, or hold decision. The sizing layer proposes an amount. Risk control can reject or reduce that amount. Finally, the execution and accounting layer applies transaction costs, updates cash and holdings, and measures the resulting portfolio.

This separation is especially important because several parts of the paper are incompletely specified. The paper gives a broad design involving an attention-enhanced BiLSTM, consecutive-rise and decline analysis, exponential position sizing, VaR, and a modified greedy algorithm. It does not fully define every interface between those components. A modular Python implementation makes each interpretation visible instead of hiding assumptions inside one large trading function.

The complete data-to-portfolio flow

The project’s README presents the intended architecture as a pipeline:

local prices

-> cleaning and chronological split

-> leakage-safe sliding windows

-> forecast model

-> buy / sell / hold signal

-> finite exponential position-size schedule

-> historical VaR filter

-> reconstructed greedy action selection

-> next-bar execution with fees and slippage

-> portfolio valuation and performance metricsEach stage has a distinct responsibility:

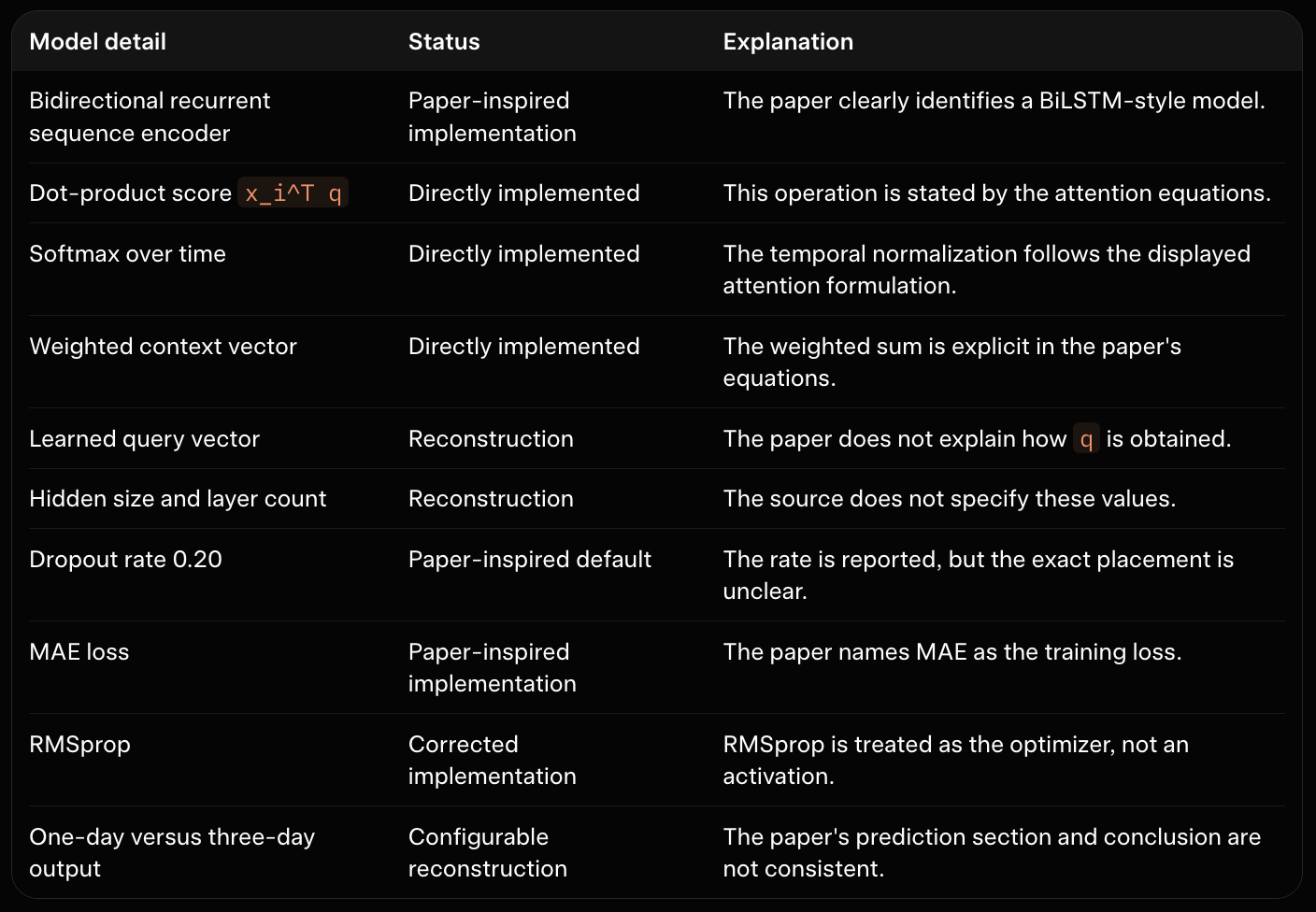

The paper’s primary model is the attention-enhanced BiLSTM, or Att-BiLSTM. It processes a historical sequence and uses temporal attention to produce a representation for forecasting. The input sequence is built from a sliding window, reported as 100 observations with stride one. The resulting prediction is not itself a trade: it must be aligned with a timestamp and passed to a decision policy.

The position-management component is conceptually independent of the neural network. It analyzes gains and declines, estimates statistics such as representative gain and decline magnitudes, and uses an exponential schedule to increase later additions. Because the paper’s position-sizing equations are corrupted or incomplete in the extracted source, the Python project treats this as a documented normalized exponential reconstruction rather than an exact transcription.

Why the boundaries matter

A single function that loads prices, trains a model, decides an order, and reports profit would be difficult to audit. It would also make it unclear whether future information entered the decision process. The generated package instead plans separate modules for data, models, streak analysis, sizing, risk, strategy, and backtesting.

For example, DataConfig makes the forecasting window explicit:

@dataclass

class DataConfig:

"""Configuration for local historical-price preparation."""

timestamp_column: str = "timestamp"

price_column: str = "price"

asset_column: Optional[str] = None

window_length: int = 100

stride: int = 1

return_definition: str = "simple"

zero_return_policy: str = "break"The values window_length=100 and stride=1 reflect the paper’s stated sliding-window setup. Other fields expose choices that the paper does not settle, such as how returns are defined and how zero returns affect streaks. Making these values configuration fields means a later experiment can record exactly which interpretation it used.

The data layer represents a cleaned asset as PriceData, a small object containing timestamps, prices, and an asset label. Its validation contract requires unique, increasing timestamps and finite positive prices. That contract is more than cosmetic. A negative or missing price can invalidate returns, position sizes, portfolio valuation, and risk calculations downstream.

The WindowedDataset object preserves temporal metadata in addition to arrays:

@dataclass(frozen=True)

class WindowedDataset:

"""Windowed samples and their temporal metadata."""

X: np.ndarray

y: np.ndarray

window_start: pd.DatetimeIndex

window_end: pd.DatetimeIndex

y_timestamp: pd.DatetimeIndex

feature_names: Tuple[str, ...] = ("price",)Keeping window_end and y_timestamp is important. A model prediction must be associated with the time at which its input information became available. The later backtest can then enforce the rule that a signal generated after the final input observation cannot fill at an earlier or identical timestamp.

Separating a forecast from an order

The paper’s forecasting section and trading section imply different horizons. The prediction tables appear to use a one-step setup, while the conclusion refers to forecasts for the next three days. The implementation therefore exposes the forecast horizon rather than assuming that those descriptions are identical.

Conceptually, a one-step window is:

\[ Xt = [z{t-99}, z{t-98}, \ldots, zt], \qquad yt = z{t+1}. \]

A three-step version is:

\[ yt = [z{t+1}, z{t+2}, z{t+3}]. \]

The forecast layer answers what the model predicts. A separate signal layer must decide how to interpret that prediction. For example, it might compare the terminal three-day forecast with the current price, or use a configured threshold before producing a buy signal. That rule is a strategy assumption, not a consequence of the neural network itself.

The same distinction applies to sizing. A positive forecast does not imply that the strategy should invest its full available balance. The sizing schedule may allocate one of several finite addition levels, subject to cash and exposure caps. The eventual order amount is therefore the result of several stages:

forecast

-> directional signal

-> candidate order amount

-> risk adjustment

-> selected feasible action

-> executed fillThis decomposition also makes it possible to compare alternatives. The same forecast can be evaluated with a flat allocation, the reconstructed exponential schedule, or a different risk limit. Likewise, the same sizing rule can be tested with Att-BiLSTM predictions or a simpler benchmark.

Offline and educational by design

The generated project is deliberately offline. It accepts local CSV files or deterministic synthetic data and does not connect to an exchange, download market data, handle credentials, or submit orders. This restriction is appropriate for a paper-to-code tutorial because it keeps the focus on data alignment, modeling assumptions, decision rules, and accounting.

Synthetic data are useful for demonstrating interfaces. For example, the data module includes a deterministic generator whose purpose is to provide repeatable price paths for checking window shapes and portfolio arithmetic. Such data are not evidence about gold or Bitcoin and cannot reproduce the paper’s reported outcomes.

The package initializer reinforces this design by avoiding model training or data loading during import:

"""Offline research components for the quantitative trading model paper."""

# Configuration is part of the lightweight public API. Heavy forecasting and

# benchmark dependencies are imported only by their respective modules.

from .config import (

BacktestConfig,

DataConfig,

ExecutionConfig,

FeeSensitivityConfig,

ForecastConfig,

SizingConfig,

SplitConfig,

VaRConfig,

validate_config,

)This side-effect-free structure lets a reader use data preparation, streak analysis, sizing, risk, or accounting utilities without installing PyTorch or every optional benchmark library. It also avoids implying that importing the package performs a market action.

What this architecture does—and does not—claim

The architecture provides a practical way to translate the paper’s major ideas into independently inspectable components. It directly reflects the clearly described mechanics, such as sliding windows and temporal attention, while making incomplete parts configurable and labeled as reconstructions.

It does not establish that the paper’s strategy is profitable or that the implementation reproduces its reported numbers. The paper’s approximate final values—$646 from a $500 gold allocation and $215,487 from a $500 Bitcoin allocation—remain unverified claims because the original data, dates, execution rules, risk settings, and position-sizing details are unavailable.

The useful starting point is therefore not a promise of matching those numbers. It is a disciplined contract between modules:

data provides only ordered historical observations;

forecasting uses a defined historical window;

signals use predictions and current state;

sizing uses a finite, explicit budget;

risk control uses pre-decision information;

execution occurs after the signal timestamp;

evaluation accounts for costs and reports portfolio behavior separately from forecast error.

That contract is the foundation for the remaining sections, where each component is examined in detail and every reconstruction decision is identified.

2. What Can Actually Be Reproduced?

The paper separates two decisions: forecasting proposes when a trade might be useful, while position management proposes how much capital to deploy. Before implementing those components, distinguish a direct implementation from a reconstruction or an illustrative example.

A paper-to-code project can contain clean Python and still fail to reproduce the original experiment. Reproduction requires the same data, timestamps, preprocessing, model definition, decision rules, execution assumptions, and evaluation protocol. Several of those ingredients are missing or ambiguous here.

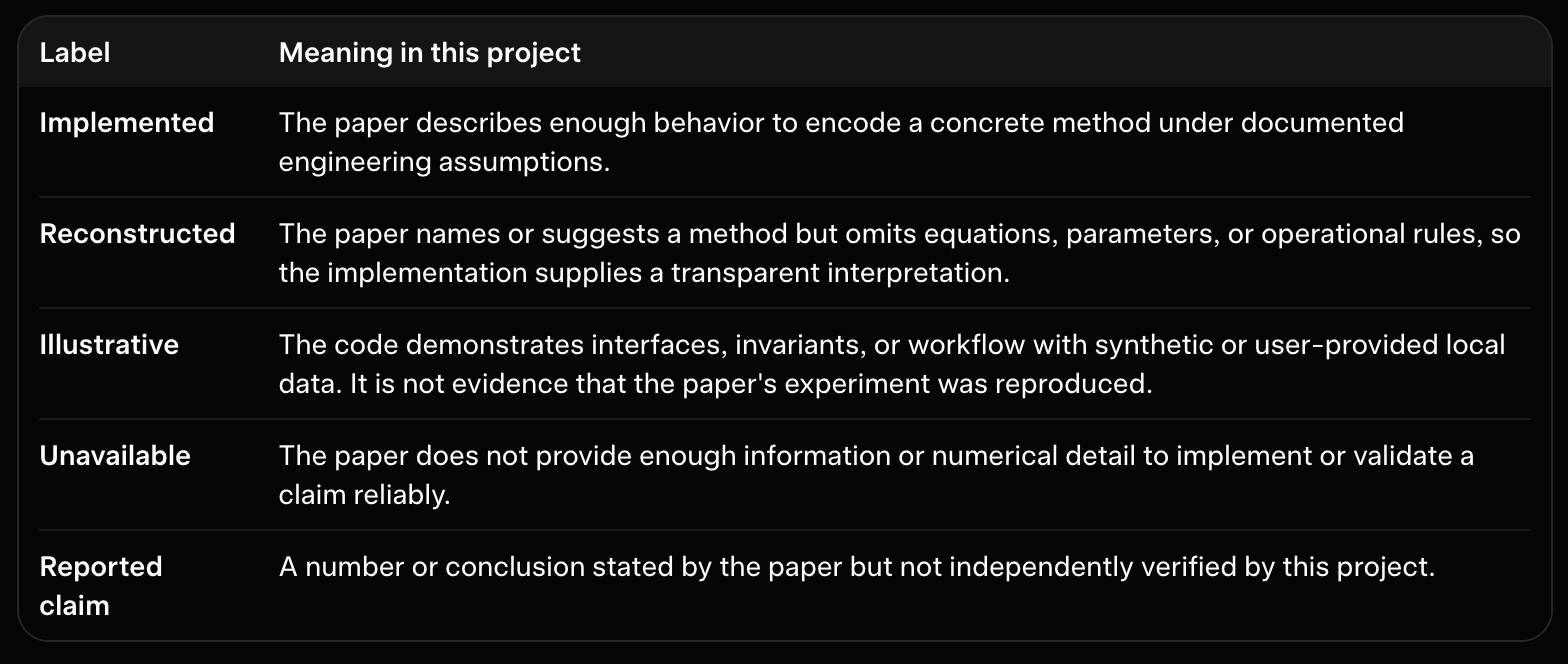

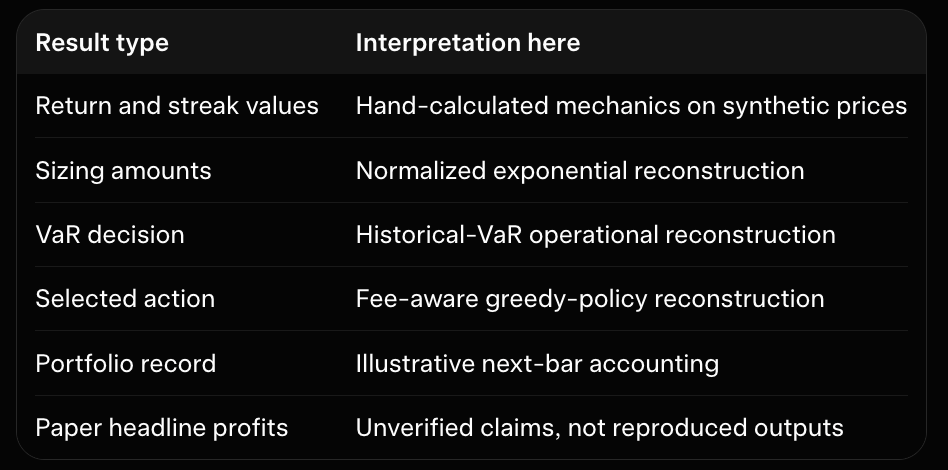

The project uses five status labels, consistent with docs/reproduction_matrix.md:

These labels determine how results should be interpreted and whether a value may legitimately be used as a test expectation. A hand-calculated fee or accounting invariant can be tested. The paper's final portfolio values cannot be treated that way because their inputs and protocol are unknown.

2.1 What the paper specifies clearly

Several elements are concrete enough to guide implementation:

overlapping historical windows of length 100 with stride 1;

an attention-enhanced bidirectional LSTM as the primary forecasting model;

comparisons with LSTM, GRU, BiLSTM, Holt-Winters, ARIMA, HMM, and XGBoost;

a stated dropout setting of 20%;

MAE as the training loss;

RMSprop as the intended optimizer after correcting the paper's terminology;

dot-product attention, softmax normalization, and a weighted temporal sum;

transaction-fee scenarios for gold and Bitcoin.

For example, src/quantitative_trading_model/models/attention.py can implement the displayed attention equations without knowing the authors' complete source code. Similarly, the configuration modules can preserve paper-inspired values as visible settings. This still does not guarantee numerical reproduction: the data, model dimensions, initialization, and training schedule remain unknown.

Configuration provenance is deliberately split across modules rather than concentrated in ForecastConfig:

DataConfigcontains the window length, stride, cleaning, and data conventions;ForecastConfigcontains model and training settings such as horizon, dropout, loss, optimizer, and hidden dimensions;SizingConfigcontains the reconstructed position-sizing settings;VaRConfigcontains risk-estimation and action settings;ExecutionConfigandBacktestConfigcontain fees, slippage, cash, leverage, and liquidation assumptions;FeeSensitivityConfigcontains the gold and Bitcoin fee grids.

This separation prevents unrelated assumptions from being hidden behind a misleading single model configuration.

2.2 Missing data and experiment identity

The largest reproducibility gap is the input data. The paper refers to historical gold and Bitcoin prices but does not identify enough information to establish exactly what those series represent. Missing details include:

the data vendor or source;

the specific gold instrument and Bitcoin market or index;

currency and unit conventions;

sampling frequency;

start and end dates;

timezone and timestamp rules;

the selected price field, such as close or adjusted close;

treatment of missing observations and duplicate timestamps;

market closures, splits, or other instrument-specific adjustments;

whether the assets were processed independently or jointly.

“Gold price” and “Bitcoin price” are not unique datasets. Two valid historical series can have different timestamps, gaps, price fields, and price levels. A model trained on either series may be reasonable while producing metrics that cannot be compared with the paper's table.

README.md, data.py, and cli.py therefore require local inputs rather than silently selecting an unidentified market-data source. Synthetic data are available only for demonstrations. This makes provenance explicit and avoids implying that an arbitrary local or synthetic series is equivalent to the paper's input.

2.3 Missing preprocessing and target definition

The paper does not fully state what the forecasting model predicts. Plausible interpretations include:

a raw next-day price;

a normalized price level;

a one-day return or percentage change;

a vector of the next three prices;

a day-three price produced by a multi-step procedure.

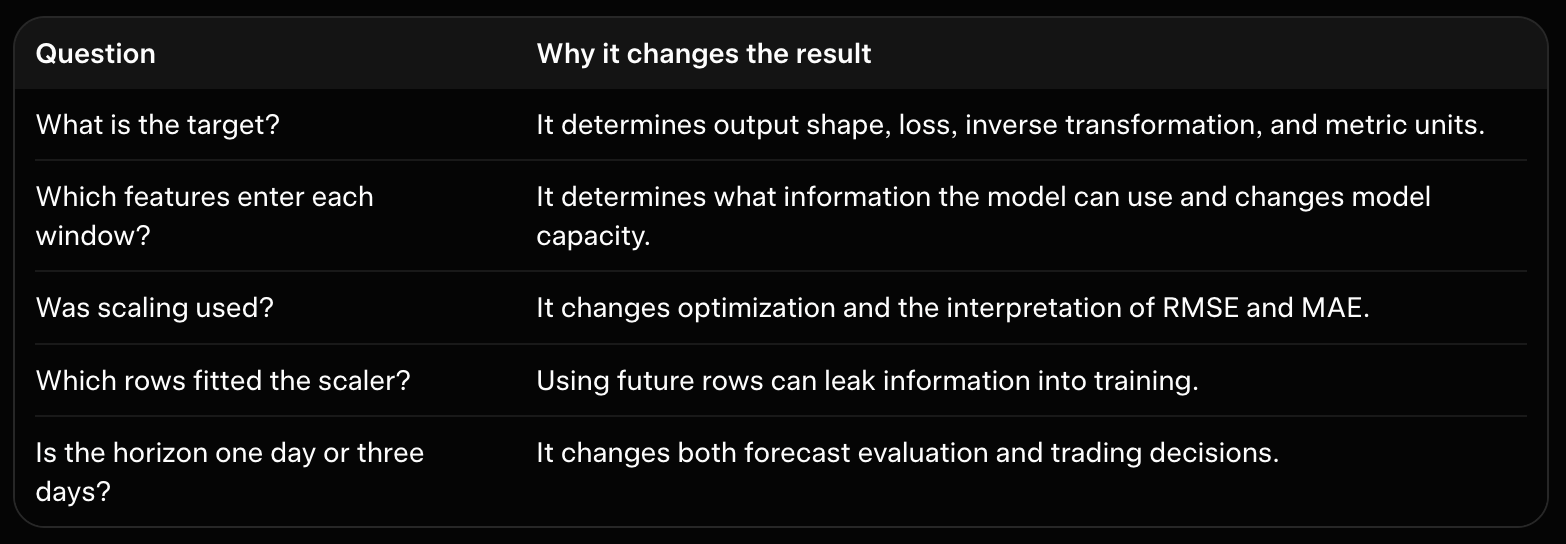

The prediction discussion is compatible with one-step forecasting, while the conclusion refers to forecasts over the next three days. These are different supervised-learning problems with different target shapes, losses, inverse transformations, and trading signals.

Preprocessing is also unclear. The paper does not specify whether prices were scaled, whether scaling used training observations only, or whether features such as volume, technical indicators, or macroeconomic variables were included. The implementation defaults to a price-based setup but exposes the target representation and horizon so that this ambiguity remains visible.

A reproduction must record at least:

2.4 Missing Att-BiLSTM architecture details

Att-BiLSTM identifies a model family, not a complete architecture. The paper does not reliably specify:

the number of recurrent layers;

hidden-state dimensions;

whether attention receives concatenated forward and backward states;

how the query vector is constructed;

dense-layer dimensions and activations;

output shape and activation;

recurrent versus ordinary dropout;

initialization;

learning-rate and optimizer settings;

batch size, epoch count, and stopping rule;

random seed;

whether each asset receives a separate model.

models/forecasters.py consequently provides a configurable paper-inspired model. Its learned attention query is an explicit reconstruction: the paper supplies a symbol q but does not say how that vector is obtained. The implementation is useful and inspectable, but it is not a verified transcription of the authors' architecture.

The same caution applies to the benchmarks. Listing LSTM, GRU, BiLSTM, Holt-Winters, ARIMA, HMM, and XGBoost does not establish that their feature sets, capacities, tuning procedures, and horizons were comparable. The paper's statement about “consistent parameters” is insufficient to reconstruct a fair benchmark protocol.

2.5 The position-sizing equations are incomplete

Equations (5) through (8) in the position-management section are not reliably recoverable from the extracted material. Important ambiguities include:

whether

p_idenotes cash, asset units, or notional exposure;the meaning of the maximum addition count

x;whether fees apply to one transaction or both sides;

whether decline statistics are signed or expressed as positive loss magnitudes;

the independent variable in the exponential expression;

whether additions follow every decline or only a forecast-confirmed condition.

src/quantitative_trading_model/sizing.py therefore does not claim to transcribe the equations. It implements a normalized exponential schedule with finite addition levels, cash limits, and exposure caps. This is a reconstructed exponential position-sizing rule: it captures the apparent idea that later additions receive larger weights, but it does not establish that the paper used the same formula or calibration.

Keeping this reconstruction in one module is useful. If the original equation images or source become available, the sizing implementation can be replaced without changing data preparation, forecasting, risk, or portfolio accounting.

2.6 VaR is named but not operationally defined

The paper says that VaR contributes to trading decisions but does not supply the settings needed for a unique procedure. Missing choices include:

confidence level;

horizon;

estimation-window length;

historical, parametric, or Monte Carlo method;

portfolio-level versus asset-level returns;

treatment of overlapping multi-day returns;

maximum acceptable loss;

whether VaR blocks, scales, or merely reports a trade.

src/quantitative_trading_model/risk.py provides a rolling historical VaR reconstruction with explicit confidence, lookback, horizon, and action settings. It supports leakage-aware use, but it cannot independently guarantee temporal provenance: HistoricalVaR accepts caller-provided returns and does not infer timestamps. The surrounding caller or backtest must supply only returns known before the decision and must exclude the current or future return when appropriate.

Thus, a VaR value means “the result of this configured historical quantile on this supplied return window.” It is not a hidden setting recovered from the paper, and it should not be described as the paper's exact VaR method.

2.7 The modified greedy algorithm is not reproducible from its name

“Modified greedy algorithm” describes a family of procedures, not one precise policy. Reproduction would require the paper to define:

candidate actions;

whether actions are buy, sell, hold, or additions;

the objective being maximized;

how forecasts become expected gains;

how fees enter the objective;

cash, exposure, and addition constraints;

how VaR affects feasibility;

whether one action or a multi-step plan is selected;

tie-breaking behavior.

src/quantitative_trading_model/strategy.py implements a transparent reconstruction: enumerate feasible candidates, estimate forecast-based benefit after fees, apply documented constraints, and select the highest-scoring candidate with deterministic tie-breaking. It must not be described as the paper's verified algorithm.

There is also an unresolved static integration issue. The generated GreedyPolicy adapter currently does not match the generated VaRTradeFilter interface: it attempts to pass proposed_notional and omits required exposure-related arguments, while the filter expects proposed_quantity together with current exposure and portfolio value. This boundary must be repaired before runtime integration is attempted. Until then, the strategy and risk modules should be treated as separately documented reconstructions rather than a verified end-to-end combination.

The temporal rule remains essential: realized future returns must never score a candidate. A decision may use forecasts, current cash, current holdings, current exposure, and pre-decision risk history, but not the price that will be observed after execution.

2.8 Why the headline profits are not test targets

The paper reports approximately:

$646 from an initial $500 gold allocation;

$215,487 from an initial $500 Bitcoin allocation;

approximately $216,133 from the combined $1,000 allocation.

These are reported claims, not reproduced results. src/quantitative_trading_model/experiments.py records the values as unverified references rather than using them as test assertions or expected outputs from synthetic demonstrations.

A test target is appropriate when its input and protocol are specified. For example, a hand-calculated accounting test can assert the cash effect of a purchase with a known fee. The paper's Bitcoin figure cannot be tested this way because the historical period, asset series, signal timestamps, sizing triggers, reinvestment rules, exposure limits, fee convention, slippage, and liquidation policy are unknown.

A local result that happens to resemble one of those values would not prove reproduction unless the underlying data and all decision and accounting rules also matched. The unusually large Bitcoin result may depend on a particular historical period, aggressive compounding, repeated averaging down, leverage-like exposure, or optimistic execution assumptions. It should not be generalized as evidence of future profitability.

2.9 Benchmark metrics and fee figures are also unverified

The paper reports forecast metrics such as RMSE, MAE, MAPE, and R-squared, and shows transaction-fee sensitivity figures. Those values cannot be confirmed from the extracted text alone.

Forecast metrics depend on the exact test observations, target scale, transformations, timestamps, MAPE zero policy, architecture, trained parameters, random seed, and stopping rule. Fee figures additionally depend on trade dates and quantities, fee side conventions, spread, slippage, action feasibility, initial holdings, reinvestment, and liquidation.

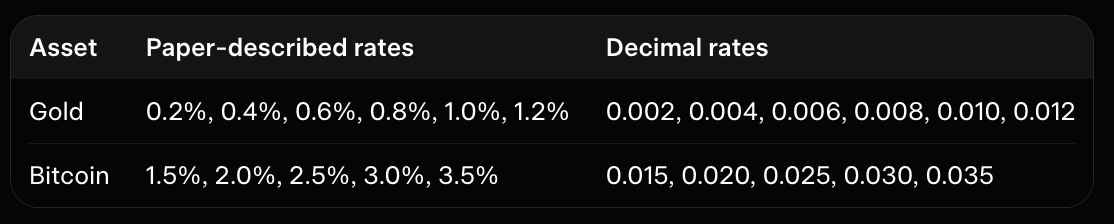

The implementation preserves the paper-inspired fee grids as inputs: gold rates from 0.2% through 1.2%, and Bitcoin rates from 1.5% through 3.5%. It cannot infer the missing y-values from the figures. A new fee sweep using identified local data is a valid experiment under the project's assumptions, not a recovered copy of the paper's chart.

2.10 How to read the reproduction matrix

docs/reproduction_matrix.md records status at the method and claim level. Its distinctions are important:

This matrix prevents every function from being presented with the same level of authority when some functions implement displayed equations and others embody missing decisions.

2.11 Static review is not empirical reproduction

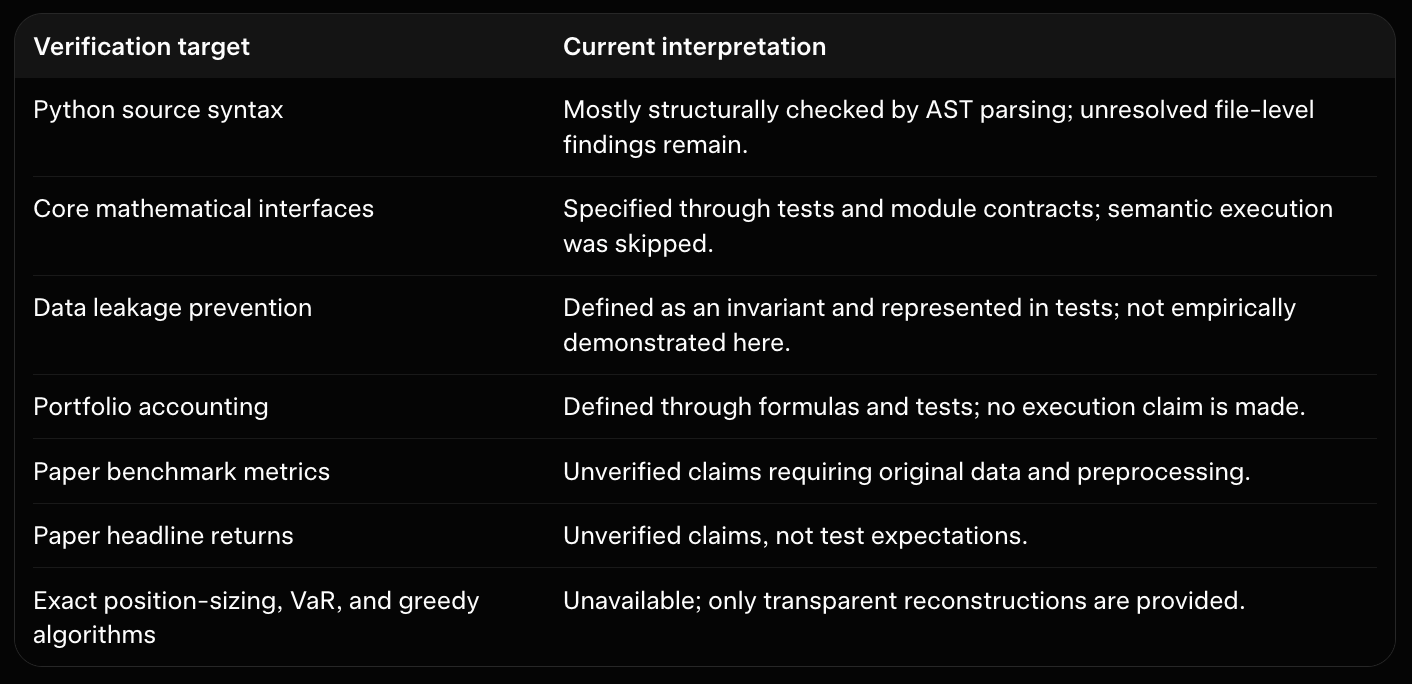

The project raises two different verification questions:

Does the generated artifact appear structurally reviewable?

Does the implementation reproduce the paper's empirical behavior?

Static and semantic review can address parts of the first question. It can inspect Python parsing, expected symbols, configuration validation, tensor-shape contracts, attention normalization, temporal boundaries, budget invariants, and accounting formulas. It cannot establish that the paper's data, model, or financial results were reproduced.

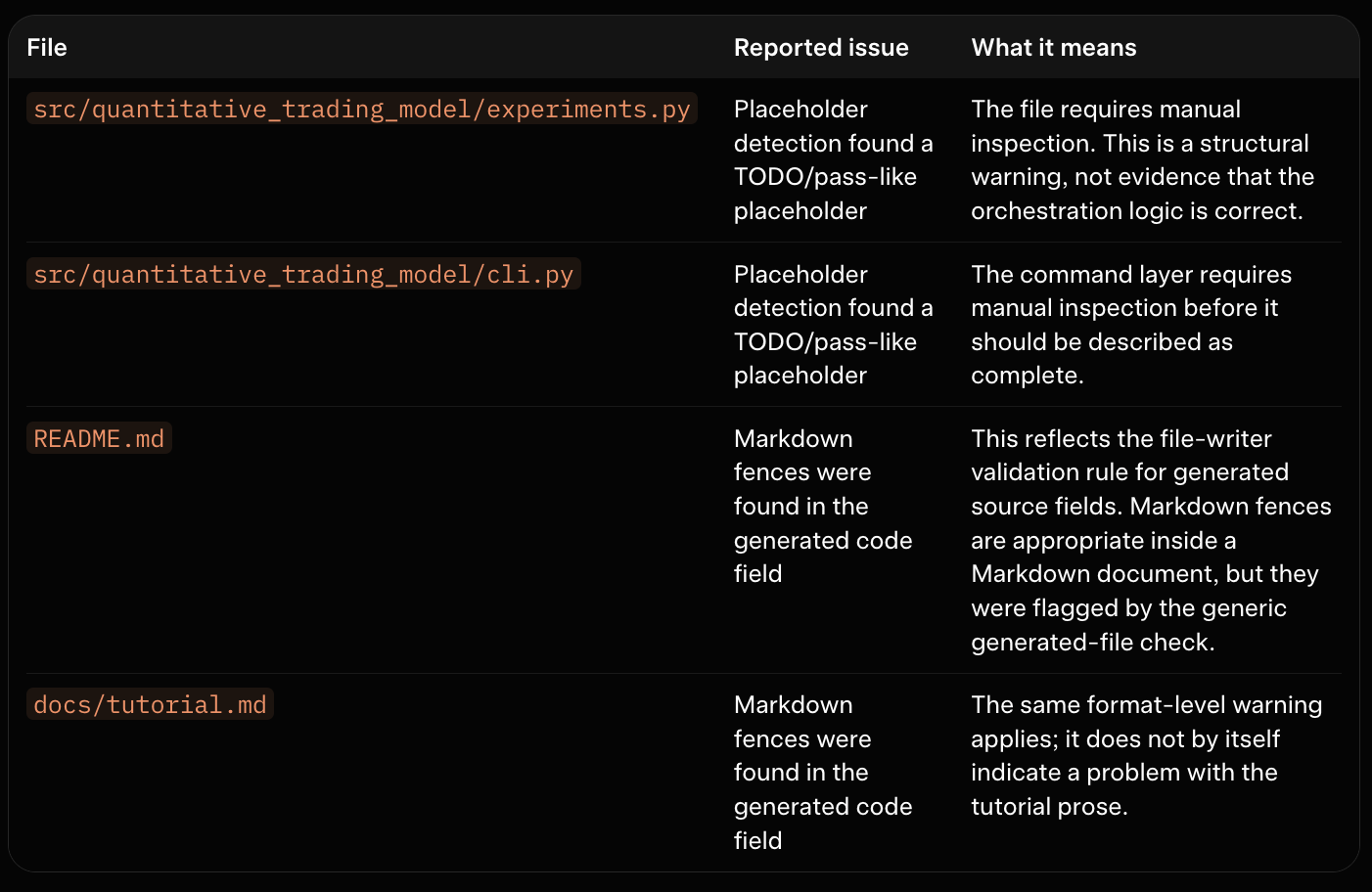

The supplied local verification record did not pass completely. It reported placeholder-detection findings for experiments.py and cli.py, and Markdown-fence findings for the generated README.md and docs/tutorial.md code fields. These are generated-artifact quality findings. They are not runtime results and do not by themselves demonstrate a Python syntax failure or a financial-model failure.

Semantic code verification was skipped. Runtime execution and test-suite success therefore must not be claimed. In addition, some generated tests and orchestration functions appear to use APIs that are not fully aligned with the generated modules, including the strategy/VaR boundary described above. Those inconsistencies require a software-maintenance pass before execution is attempted.

The appropriate conclusion is limited: the project documents intended interfaces, assumptions, and invariants, but it is not an executed or empirically validated reproduction.

2.12 Responsible interpretation policy

When describing results from this project:

say implemented for mechanics supported by the paper and the code contract;

say reconstructed for normalized sizing, historical VaR, the greedy policy, and other interpretations of missing details;

say illustrative for synthetic data and hand-calculated workflows;

say unavailable when the source lacks the information needed for implementation or validation;

say reported claim when quoting the paper's profits or metrics without independent validation;

do not call a run on a different local dataset an exact reproduction;

keep forecast metrics separate from portfolio metrics;

report dates, data provenance, target definition, fees, slippage, turnover, drawdown, and liquidation rules with every backtest;

treat static review as artifact evidence, not proof of execution, profitability, or paper fidelity.

The next sections can discuss setup and implementation without blurring these categories. A modular reconstruction can still teach attention-based forecasting, streak statistics, bounded sizing, risk filtering, and fee-aware accounting while making clear which conclusions require the original data and experimental protocol.

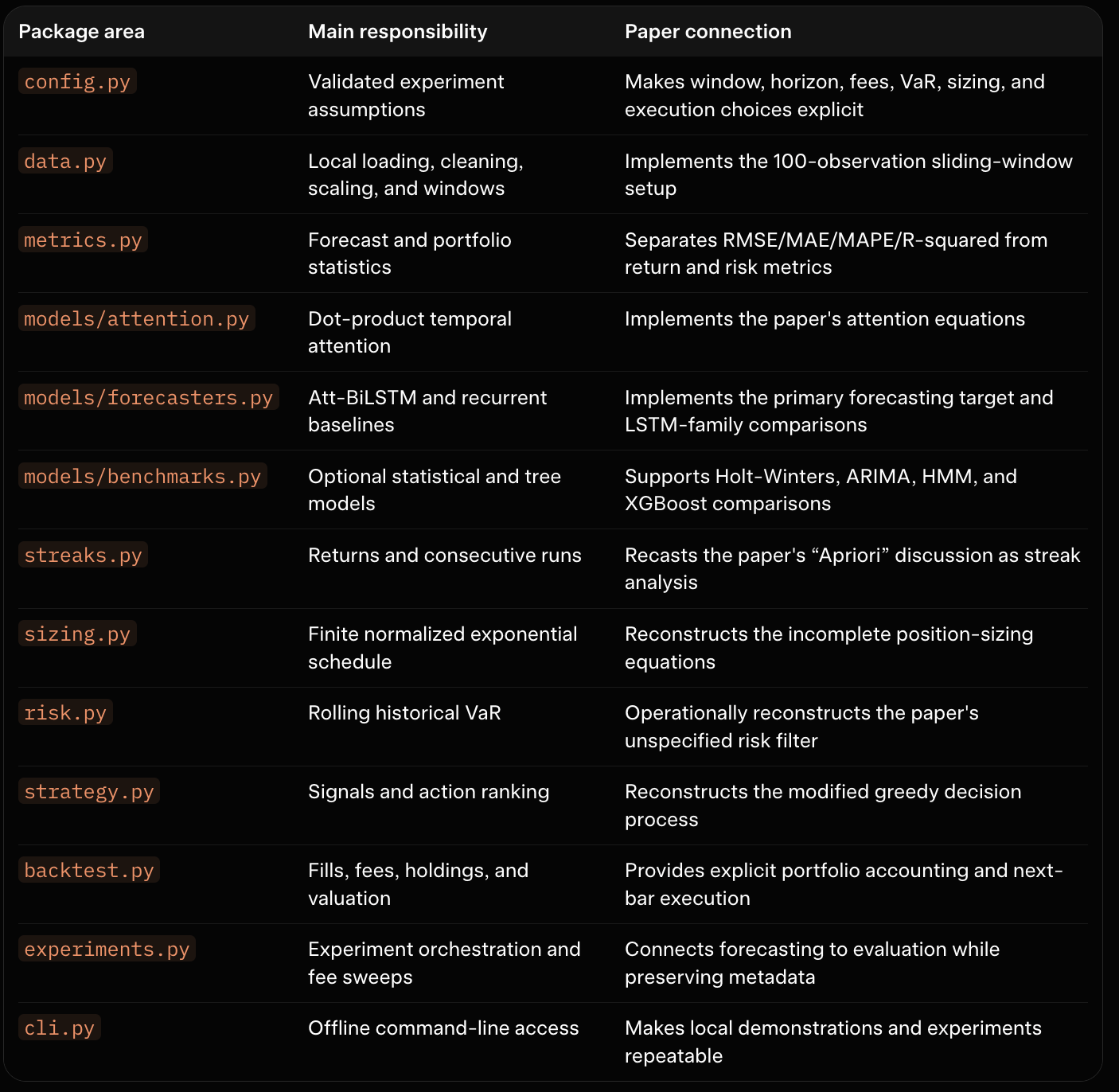

3. Project Setup and the Implementation Map

The implementation is organized as a normal Python package rather than as one large research script. That choice matters because the paper combines several different responsibilities: data preparation, neural forecasting, benchmark models, streak analysis, position sizing, risk filtering, trading decisions, execution, and evaluation. Keeping those responsibilities in separate modules makes it easier to inspect assumptions and replace incomplete reconstructions later.

The project is also deliberately offline. It accepts local files or generated demonstration data, but it does not connect to an exchange, download market data, store credentials, or submit orders. The resulting code is suitable for educational research and backtest prototyping, not for live trading.

3.1 The src layout

The package uses the conventional src layout:

quantitative-trading-model/

├── pyproject.toml

├── README.md

├── src/

│ └── quantitative_trading_model/

│ ├── __init__.py

│ ├── config.py

│ ├── data.py

│ ├── metrics.py

│ ├── streaks.py

│ ├── sizing.py

│ ├── risk.py

│ ├── strategy.py

│ ├── backtest.py

│ ├── experiments.py

│ ├── cli.py

│ └── models/

│ ├── attention.py

│ ├── forecasters.py

│ └── benchmarks.py

├── tests/

└── docs/

├── tutorial.md

└── reproduction_matrix.mdWith this layout, the importable package lives under src/quantitative_trading_model, while documentation and tests remain outside the runtime package. The pyproject.toml file tells setuptools where to find the package:

[tool.setuptools]

package-dir = { "" = "src" }

include-package-data = true

[tool.setuptools.packages.find]

where = ["src"]This avoids a common development problem in which tests accidentally import a loose source directory instead of the package that users will install. It also gives the project a clear boundary: files under src/quantitative_trading_model are implementation modules, while the root-level documentation explains how to use and interpret them.

3.2 Core dependencies and optional model dependencies

The package keeps its required dependencies small:

[project]

requires-python = ">=3.10"

dependencies = [

"numpy>=1.24",

"pandas>=2.0"

]NumPy and pandas support the parts of the project that do not require a deep-learning framework: local price tables, timestamp handling, return calculations, streak statistics, metrics, risk calculations, and portfolio accounting.

The heavier forecasting libraries are optional:

[project.optional-dependencies]

deep-learning = [

"torch>=2.0"

]

classical = [

"statsmodels>=0.14",

"pmdarima>=2.0",

"hmmlearn>=0.3",

"xgboost>=2.0"

]This split reflects the paper's structure. The Att-BiLSTM requires PyTorch, but a reader who only wants to study the return convention, normalized exponential sizing reconstruction, historical VaR, or portfolio accounting should not need to install PyTorch. Similarly, Holt-Winters, ARIMA, HMM, and XGBoost benchmarks can be enabled only when those comparisons are needed.

The optional dependency design also makes missing capabilities visible. A benchmark adapter should report that a library is unavailable rather than silently substituting a different model. That distinction matters when comparing results with the paper: an omitted benchmark is not the same as a benchmark that produced a poor score.

The package metadata also defines a console entry point:

[project.scripts]

quant-trading-model = "quantitative_trading_model.cli:main"After local installation, this exposes the offline command-line interface as quant-trading-model. The CLI can validate local CSV files, generate deterministic synthetic demonstrations, and dispatch configured research experiments. It does not create a network client or read credentials.

3.3 Side-effect-free package imports

The package initializer intentionally exposes only lightweight metadata and configuration types:

"""Offline research components for the quantitative trading model paper."""

from importlib import metadata

try:

__version__ = metadata.version("quantitative-trading-model")

except metadata.PackageNotFoundError:

__version__ = "0.1.0"

from .config import (

BacktestConfig,

DataConfig,

ExecutionConfig,

FeeSensitivityConfig,

ForecastConfig,

SizingConfig,

SplitConfig,

VaRConfig,

validate_config,

)Importing the package does not load a CSV, train a model, create a portfolio, or contact an external service. The initializer also does not import PyTorch, statsmodels, hmmlearn, or XGBoost. Those imports are deferred to the modules that need them.

That design has two practical benefits:

Lightweight use: core modules remain usable in an environment without optional modeling libraries.

Predictable imports: simply writing import quantitative_trading_model cannot start a computation or produce an external side effect.

The public exports are deliberately narrow:

__all__ = [

"__version__",

"BacktestConfig",

"DataConfig",

"ExecutionConfig",

"FeeSensitivityConfig",

"ForecastConfig",

"SizingConfig",

"SplitConfig",

"VaRConfig",

"validate_config",

]The model, data, strategy, and backtest classes are imported from their own modules when required. This keeps the top-level API stable without forcing every user to install every optional dependency.

3.4 Where each research responsibility lives

The package map follows the paper's conceptual pipeline:

This separation is not merely a software-style preference. It prevents an ambiguous paper detail from being hidden inside an unrelated function. For example, the return denominator belongs in streaks.py, while the execution fee convention belongs in backtest.py. A reader can therefore change one assumption without accidentally changing every layer of the research pipeline.

3.5 Documentation, tests, and the reproduction matrix

The non-runtime files serve different purposes:

`README.md` gives installation instructions, local CSV conventions, CLI examples, project warnings, and a high-level architecture map.

`docs/tutorial.md` explains the paper-to-code translation in detail, including equations, tensor shapes, timing rules, and reconstruction decisions.

`docs/reproduction_matrix.md` tracks each paper component as implemented, reconstructed, illustrative, unavailable, or an unverified reported claim.

`tests/` contains hand-calculable checks for data boundaries, streak semantics, sizing budgets, VaR decisions, model shapes, transaction fees, and portfolio-value identity.

The reproduction matrix is especially useful for this paper because the source does not fully specify equations (5)–(8), VaR operation, the greedy policy, or the original backtest protocol. Instead of allowing those gaps to disappear into code, the matrix records what the implementation can support and what still requires the original data or source material.

For example, the matrix treats the following differently:

the 100-step window as a directly implementable paper detail;

the learned attention query as a reconstruction;

synthetic prices as an illustration;

the reported

$646gold and$215,487Bitcoin outcomes as unverified claims.

That classification should remain visible in experiment output and documentation. A clean package installation does not establish empirical reproduction, and static code checks do not establish that the paper's financial results are correct.

3.6 A practical installation boundary

A typical local setup is:

python -m venv .venv

python -m pip install --upgrade pip

python -m pip install -e .The core installation is enough to explore data preparation, streak analysis, risk calculations, sizing, metrics, and portfolio accounting. To use the PyTorch forecasters, install the deep-learning extra:

python -m pip install -e '.[deep-learning]'The classical benchmark dependencies are declared under the classical extra in pyproject.toml:

python -m pip install -e '.[classical]'The exact installed command surface can be inspected with:

quant-trading-model --helpThese commands install or invoke local research tooling only. They do not download the paper's missing gold or Bitcoin data. The user must supply a provenance-documented local dataset before treating any result as an empirical experiment.

3.7 What this structure does—and does not—guarantee

The package structure provides useful engineering guarantees:

optional modeling libraries do not prevent core imports;

configuration choices are visible rather than scattered through scripts;

data, forecast, strategy, execution, and evaluation responsibilities are separated;

documentation can distinguish direct implementation from reconstruction;

tests can check local invariants without requiring the paper's unavailable data.

It does not guarantee that the paper's reported results can be reproduced. The missing dataset, dates, preprocessing, exact model architecture, VaR parameters, greedy rules, position-sizing equations, and execution protocol remain external requirements. The next sections use this package structure to examine those components one at a time, beginning with validated configuration and local data preparation.

4. Make Ambiguity Explicit with Validated Configuration

A research paper can name an algorithm without specifying every value required to run it. This paper gives some concrete settings, including a 100-observation history, one-observation stride, 20% dropout, MAE loss, RMSprop optimization, and several transaction-fee scenarios. It leaves other choices unclear, including the forecast horizon, recurrent-layer dimensions, attention query, VaR policy, position-sizing parameters, execution timing, and liquidation rule.

The implementation records these choices in dataclasses defined in src/quantitative_trading_model/config.py. Centralized configuration does not recover the paper's missing data or prove that its reported results can be reproduced. It does make assumptions visible, validates basic invariants, and provides metadata that can be saved with an experiment.

There are three important categories of settings:

Paper-inspired settings are stated directly or strongly suggested by the paper.

Reconstruction settings are operational choices needed because the paper is incomplete.

Implementation safety settings constrain this educational simulator even when the paper does not describe equivalent controls.

The distinction matters because a field can be present in configuration without being fully wired into every generated runtime module. The status of each important setting should therefore be checked against both config.py and the module that consumes it.

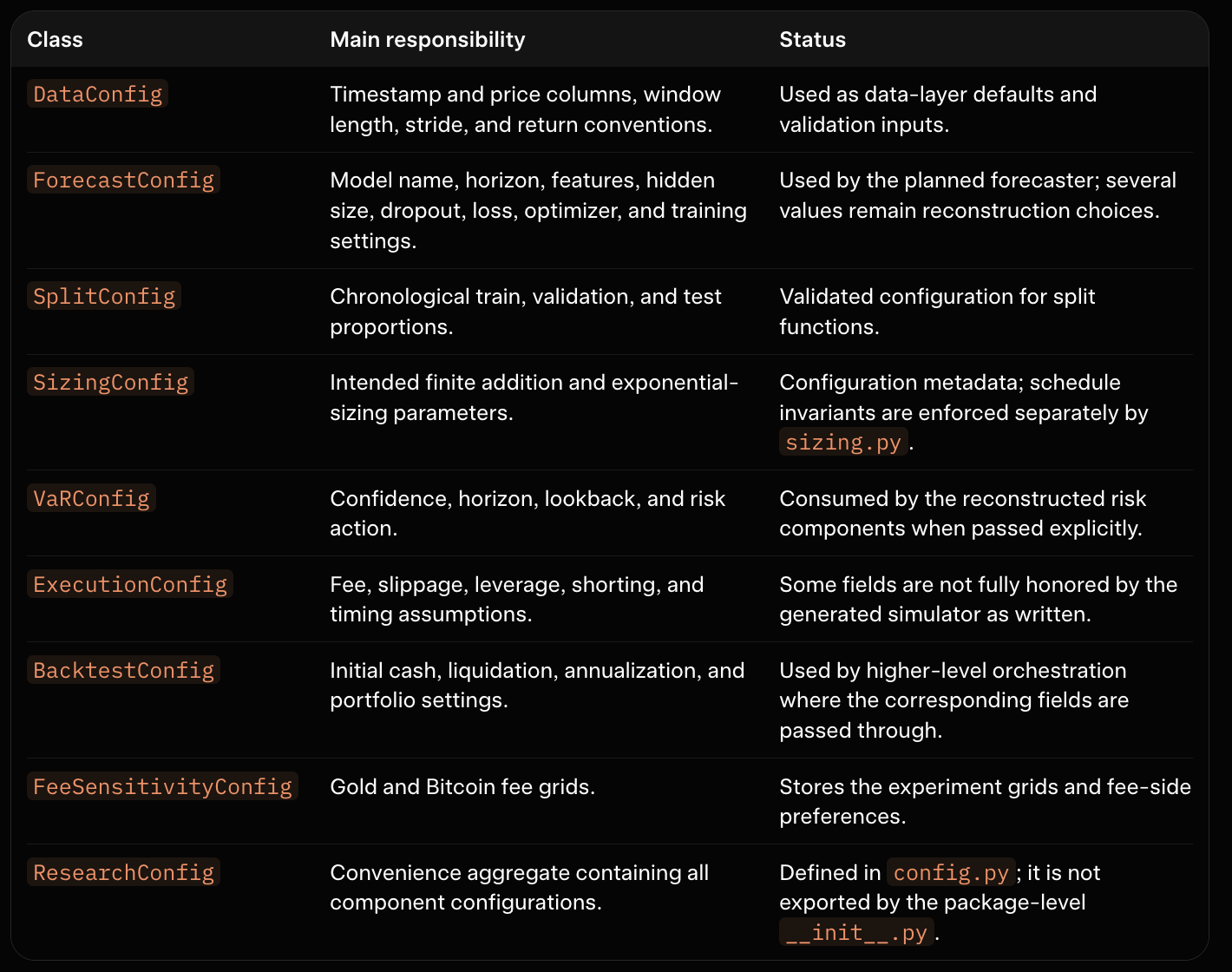

4.1 Configuration objects and their responsibilities

The configuration module defines separate dataclasses for the main layers of the pipeline:

For example, the paper-inspired data and forecasting defaults are:

@dataclass

class DataConfig:

timestamp_column: str = "timestamp"

price_column: str = "price"

window_length: int = 100

stride: int = 1

return_definition: str = "simple"

@dataclass

class ForecastConfig:

model_name: str = "att_bilstm"

horizon: int = 1

target_type: str = "scaled_price"

hidden_size: int = 32

num_layers: int = 1

dropout: float = 0.20

learning_rate: float = 0.001

optimizer: str = "rmsprop"

loss: str = "mae"

learned_attention_query: bool = TrueThe values with the clearest connection to the paper are:

window_length=100: the reported historical window length;stride=1: the reported one-observation shift between windows;dropout=0.20: the paper-inspired dropout rate;loss="mae": the reported training loss;optimizer="rmsprop": a correction to the paper's terminology, since RMSprop is an optimizer rather than an activation function;model_name="att_bilstm": the paper's claimed primary forecasting model.

The hidden size, number of layers, learning rate, batch size, epoch count, early-stopping policy, and learned-query choice are not established by the paper. They are configurable reconstruction choices and should be recorded with any result.

4.2 Make the forecast horizon explicit

The paper's prediction discussion is not consistent about horizon. Its model description and metric table can be read as a one-step forecasting setup, while the conclusion refers to forecasts for the next three days. The source does not establish whether this means a three-element output vector, repeated one-step forecasts, or a single prediction for the third day.

The configuration makes the choice visible:

one_day = ForecastConfig(horizon=1)

three_days = ForecastConfig(horizon=3)The horizon affects more than the output layer. It changes target construction, prediction metrics, signal aggregation, and execution timing. A one-step model should not be called a three-day model merely because its output is used repeatedly. The selected horizon should be stored in experiment metadata.

target_type is similarly uncertain. The paper does not clearly say whether it predicts raw prices, scaled prices, returns, or percentage changes. The generated default, "scaled_price", is a practical implementation choice and not a verified transcription.

4.3 Position-sizing configuration: metadata versus enforcement

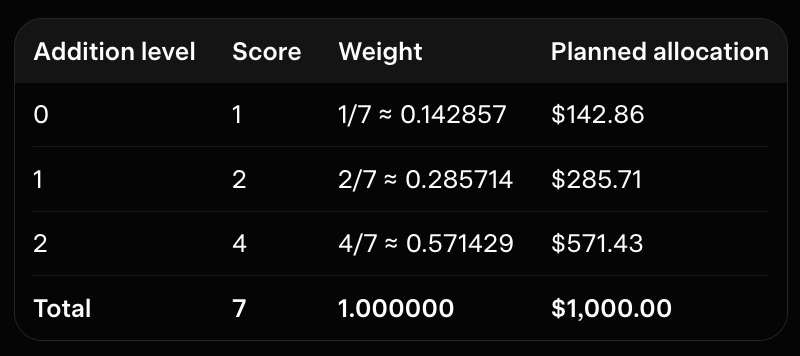

The position-management equations are among the least reproducible parts of the paper. Equations (5) and (6) appear to describe recursive additions intended to compensate for declines and fees, but their notation is corrupted. Equation (7) does not clearly identify the independent variable of the exponential, and Equation (8) appears to normalize position scores into allocations.

SizingConfig records a possible reconstruction:

@dataclass

class SizingConfig:

maximum_additions: int = 5

initial_level: int = 1

growth_rate: float = 0.50

score_scale: float = 1.0

allocation_fraction: float = 1.0

initial_position_fraction: float = 0.20

maximum_exposure_fraction: float = 1.0

allow_reuse: bool = False

calibrate_from_percentiles: bool = False

recovery_percentile: float = 0.50

decline_percentile: float = 0.10

fee_buffer: float = 0.0The intended normalized reconstruction is:

score_i = score_scale * exp(growth_rate * i)

weight_i = score_i / sum(score_j)

allocation_i = budget * weight_iHowever, these configuration fields should not be confused with runtime guarantees. In the generated project, sizing.py builds schedules through build_exponential_schedule() and enforces schedule-level properties through SizingSchedule, including finite allocations, normalized weights, a total budget, and one-time level consumption. validate_config() validates maximum_additions and related fractions, but it does not construct a schedule or verify its normalized weights.

Likewise, allocation_fraction, maximum_exposure_fraction, allow_reuse, and fee_buffer are currently configuration or documentation choices rather than completely wired controls in the generated sizing path. The schedule builder receives its own budget and growth arguments. It does not automatically read every corresponding field from SizingConfig, and fee_buffer is not applied to an allocation. A caller must pass the intended values into the sizing module explicitly or add the missing integration before treating them as active controls.

The safe interpretation is therefore:

maximum_additionsdocuments the intended finite schedule size;schedule normalization and budget checks belong to

SizingScheduleandsizing.py;reuse prevention is enforced when a constructed schedule marks a level as used;

exposure and cash caps must be applied by the sizer, strategy, or simulator that receives them;

the incomplete paper equations remain a reconstruction, not an exact implementation.

4.4 VaR configuration is an operational reconstruction

The paper names VaR but does not define its confidence level, horizon, estimation window, return distribution, or action threshold. A usable risk filter must choose all of these values, so VaRConfig makes them explicit:

@dataclass

class VaRConfig:

enabled: bool = True

confidence: float = 0.95

horizon: int = 1

lookback: int = 100

method: str = "historical"

action: str = "scale"

max_var_fraction: float = 0.05

insufficient_history: str = "allow"

min_observations: int = 30These defaults describe a rolling historical-VaR interpretation, not the paper's verified settings:

confidence=0.95selects a 95% lower-tail confidence convention;horizon=1uses one period by default;lookback=100limits the estimation history;method="historical"avoids assuming normally distributed returns;action="scale"permits reducing an order when projected risk is too high;max_var_fraction=0.05expresses the risk limit as a fraction of portfolio value;insufficient_history="allow"defines behavior before enough observations exist.

The generated risk.py contains the actual historical estimator and filter. It must receive returns that were available before the decision timestamp. Configuration alone cannot enforce timestamp ordering. Also, because the paper provides no numerical VaR settings, every backtest should report these values as reconstruction metadata.

A stricter configuration can block trades until sufficient history exists:

risk = VaRConfig(

confidence=0.99,

lookback=252,

min_observations=100,

action="block",

insufficient_history="block",

)4.5 Execution and liquidation: record the intended contract carefully

The paper does not specify whether a signal uses the same closing price, the next opening price, or another execution price. It also does not say clearly whether a fee applies to purchases, sales, or both. The intended execution configuration is:

@dataclass

class ExecutionConfig:

fee_rate: float = 0.002

fee_on_buy: bool = True

fee_on_sell: bool = True

slippage_rate: float = 0.0

allow_fractional_units: bool = True

allow_short: bool = False

max_leverage: float = 1.0

execute_next_bar: bool = True

reject_insufficient_cash: bool = TrueThese fields describe the desired research contract, but the generated backtest.py does not fully honor all of them as written. In particular:

the simulator applies

fee_rateto both buys and sells unconditionally; it does not consultfee_on_buyorfee_on_sell;unaffordable buys are clipped to the affordable quantity rather than being controlled by

reject_insufficient_cash;the simulator uses its own

allow_leveragebehavior and does not enforcemax_leveragefromExecutionConfig;the default simulator is nevertheless long-only and non-leveraged through its separate defaults, so cash and holdings are intended to remain nonnegative;

next-bar execution is enforced by requiring the fill timestamp to be strictly later than the signal timestamp.

This distinction is important. A configuration field is not proof that the current runtime path consumes it. Until the wiring is corrected, results should state the simulator's actual behavior: two-sided fees, optional slippage, clipping of unaffordable buys, no shorting by default, and strict later-bar execution.

BacktestConfig contains additional lifecycle choices:

@dataclass

class BacktestConfig:

initial_cash: float = 500.0

initial_quantity: float = 0.0

liquidate_at_end: bool = True

risk_free_rate: float = 0.0

periods_per_year: int = 252

currency: str = "USD"The $500 default resembles the paper's stated per-asset starting allocation, but it does not reproduce the paper's final values. Dates, trades, fees, holdings, and liquidation accounting remain unspecified. liquidate_at_end=True is an explicit implementation choice: it may sell remaining holdings and charge the simulator's sell-side fee. A mark-to-market result without liquidation would be different.

4.6 Fee grids use decimal conventions

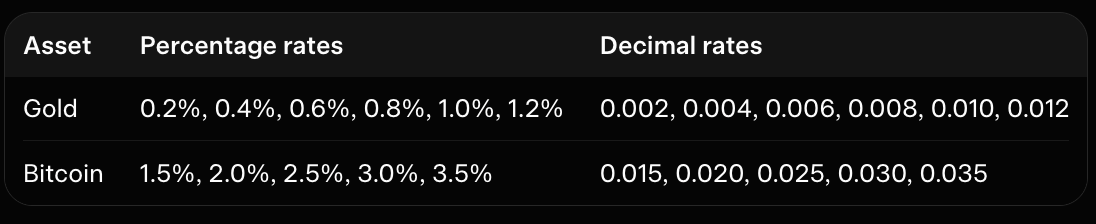

The paper lists percentages, while the configuration stores decimal rates:

The conversion is:

0.2% = 0.2 / 100 = 0.002

1.5% = 1.5 / 100 = 0.015The corresponding defaults are:

@dataclass

class FeeSensitivityConfig:

gold_rates: tuple[float, ...] = (

0.002, 0.004, 0.006, 0.008, 0.010, 0.012

)

bitcoin_rates: tuple[float, ...] = (

0.015, 0.020, 0.025, 0.030, 0.035

)

apply_to_buys: bool = True

apply_to_sells: bool = True

hold_signals_fixed: bool = TrueUsing 0.2 for a 0.2% fee would represent a 20% rate. The validator checks that rates are finite and lie in the interval [0, 1], but it cannot determine whether a user has confused percentage points with decimal rates. In other words, 0.2 is accepted as a numerically valid rate even though it is probably a unit mistake for this experiment. The decimal convention must therefore be documented and reviewed by the caller.

The fee-side flags are also not fully honored by the generated simulator, which currently charges both sides. hold_signals_fixed describes the sensitivity protocol rather than changing the backtest automatically. If fees affect feasibility or greedy ranking, actions may need to be regenerated for each fee scenario.

4.7 What validate_config() checks

The public validator accepts a complete aggregate or individual components:

from quantitative_trading_model.config import (

ResearchConfig,

ForecastConfig,

validate_config,

)

config = ResearchConfig(

forecast=ForecastConfig(

model_name="att_bilstm",

horizon=3,

dropout=0.20,

loss="mae",

optimizer="rmsprop",

)

)

validate_config(config)Component validators check basic constraints such as:

_require(config.window_length > 0, "data.window_length must be positive")

_require(0 <= config.dropout < 1, "forecast.dropout must be in [0, 1)")

_require(0 < config.confidence < 1, "var.confidence must be in (0, 1)")

_require(config.fee_rate >= 0, "execution.fee_rate cannot be negative")

_require(config.maximum_additions > 0, "sizing.maximum_additions must be positive")This validation rejects invalid configuration values such as nonpositive horizons, dropout outside [0, 1), unsupported optimizer or loss names, split fractions that do not sum to one, negative fees or slippage, invalid VaR actions, and empty fee grids.

It does not perform every runtime or semantic check. Specifically:

it does not construct a sizing schedule or check that its weights sum to one;

it does not validate the contents of a price file;

it does not prove that every configuration field is consumed by the backtest;

it does not detect a percentage-unit mistake such as entering

0.2for0.2%;it does not establish that VaR inputs are timestamp-safe;

it does not verify that generated experiments reproduce the paper.

Schedule-level invariants are handled in sizing.py, data invariants in data.py, and accounting invariants in backtest.py. Those layers must be reviewed together with configuration validation.

The validator also rejects supplying both a complete ResearchConfig and individual component overrides. This prevents a caller from validating one configuration while accidentally running another.

4.8 Record a complete experiment configuration

A complete experiment can combine paper-inspired and reconstructed settings:

from quantitative_trading_model.config import (

ResearchConfig,

ForecastConfig,

VaRConfig,

validate_config,

)

config = ResearchConfig(

forecast=ForecastConfig(

model_name="att_bilstm",

horizon=3,

hidden_size=32,

dropout=0.20,

loss="mae",

optimizer="rmsprop",

),

var=VaRConfig(

confidence=0.95,

horizon=1,

lookback=100,

action="scale",

),

)

validate_config(config)

metadata = {

"window_length": config.data.window_length,

"stride": config.data.stride,

"forecast_horizon": config.forecast.horizon,

"dropout": config.forecast.dropout,

"loss": config.forecast.loss,

"optimizer": config.forecast.optimizer,

"var_confidence": config.var.confidence,

"var_lookback": config.var.lookback,

"fee_rate": config.execution.fee_rate,

"liquidate_at_end": config.backtest.liquidate_at_end,

}This record combines direct paper-inspired values with reconstruction choices. It should be saved alongside forecast metrics, portfolio metrics, data provenance, and software-version information.

ResearchConfig is available from quantitative_trading_model.config. It is not currently included in the package-level exports in quantitative_trading_model/__init__.py, so importing it from the configuration module is the reliable documented path.

4.9 Configuration is necessary but not sufficient

The configuration contract solves an engineering problem: it makes assumptions visible, validates basic values, and gives experiments a stable record. It does not solve the paper's missing-information problem. It cannot recover:

the unidentified gold and Bitcoin datasets;

the original dates, frequency, or test boundary;

the exact attention query and network architecture;

the corrupted recursive position-sizing equations;

the paper's VaR settings or action policy;

the modified greedy algorithm's objective;

the original execution, fee, and liquidation protocol;

the numeric values behind the fee-sensitivity figures.

The approximately $646 gold result, approximately $215,487 Bitcoin result, combined approximately $216,133 result, and reported benchmark metrics therefore remain unverified paper claims. Matching visible defaults does not reproduce those results.

The generated project also has known API inconsistencies between some configuration fields and downstream modules, and semantic code verification was skipped. This section consequently describes the intended configuration contract and the actual validation boundaries; it does not claim that the generated code was executed or that every setting passed through the complete runtime pipeline.

The safest interpretation is that configuration turns an incomplete paper into an auditable research specification. It identifies what comes from the source, what is reconstructed, what is merely illustrative, and which safety controls belong to this educational implementation rather than to the original paper.

5. Load Local Prices Without Assuming the Paper’s Missing Dataset

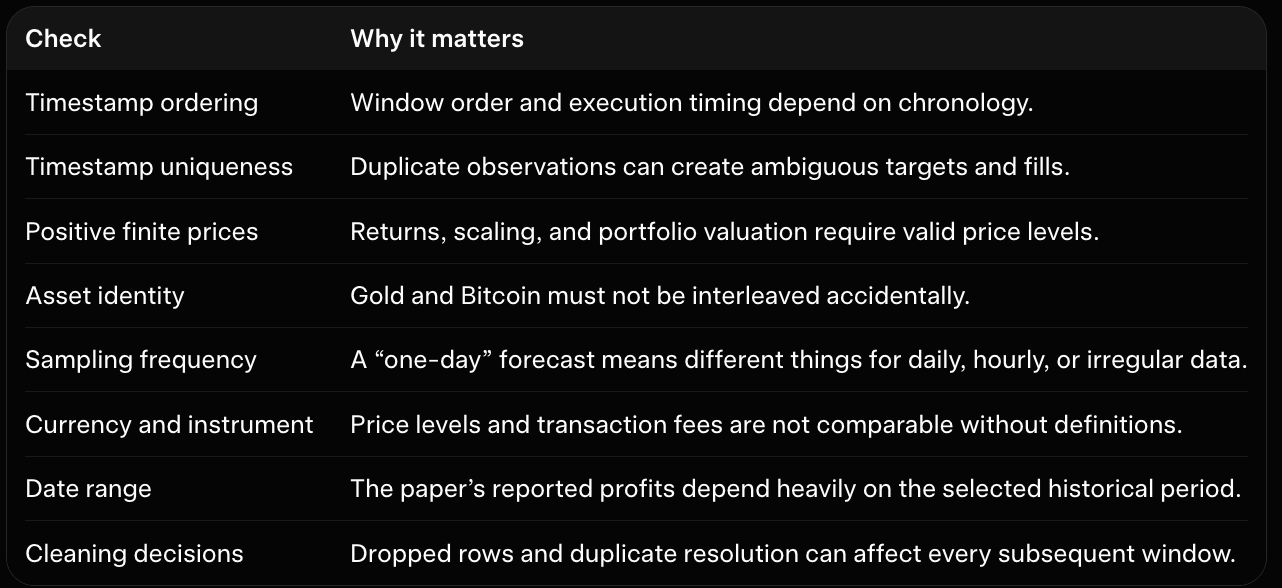

The paper says that it uses historical gold and Bitcoin prices, but it does not identify the data source, instrument, currency, frequency, date range, or exact columns. That omission is important: even a correct implementation can produce different results if it uses a different gold contract, Bitcoin exchange, timezone, sampling interval, or adjusted-price convention.

The generated project therefore does not silently select a market-data provider. Instead, it accepts a local CSV file or a caller-supplied pandas object. This keeps the experiment offline and makes data provenance the reader’s responsibility. Before treating a result as empirical evidence, record where the file came from, which instrument it represents, and how it was prepared.

5.1 The minimum data contract

The implementation reduces each asset to two essential fields:

timestamp: when the price observation was available;price: a finite, strictly positive price.

A minimal CSV looks like this:

timestamp,price

2020-01-01,1518.2

2020-01-02,1523.7

2020-01-03,1511.4The PriceData class in src/quantitative_trading_model/data.py stores the cleaned result and an asset label:

@dataclass(frozen=True)

class PriceData:

frame: pd.DataFrame

asset: str = "asset"

def __post_init__(self) -> None:

required = {"timestamp", "price"}

missing = required.difference(self.frame.columns)

if missing:

raise ValueError(f"PriceData is missing required columns: {sorted(missing)}")

timestamps = pd.to_datetime(self.frame["timestamp"], errors="raise")

prices = pd.to_numeric(self.frame["price"], errors="raise").to_numpy(dtype=float)

if timestamps.duplicated().any():

raise ValueError("PriceData timestamps must be unique")

if not timestamps.is_monotonic_increasing:

raise ValueError("PriceData timestamps must be strictly increasing")

if not np.isfinite(prices).all() or (prices <= 0).any():

raise ValueError("PriceData prices must be finite and strictly positive")PriceData.__post_init__ is a validation boundary. It does not decide whether a price is economically meaningful for every possible instrument, but it enforces the assumptions required by the downstream time-series code. An empty dataset, duplicate timestamp, unsorted timestamp sequence, missing value, infinity, zero, or negative price cannot silently proceed into window construction.

The timestamps and prices properties provide convenient, typed access to the two series:

@property

def timestamps(self) -> pd.DatetimeIndex:

return pd.DatetimeIndex(self.frame["timestamp"])

@property

def prices(self) -> np.ndarray:

return self.frame["price"].to_numpy(dtype=float, copy=True)Returning a copy from prices reduces the chance that a caller accidentally mutates the validated internal frame without re-running validation.

5.2 Standardizing different local column names

Real CSV files often use names such as Date, datetime, Close, or Adj Close. The standardize_prices function accepts explicit column names when necessary, but can also recognize common alternatives:

def standardize_prices(

data: Union[pd.DataFrame, PriceData],

*,

timestamp_column: Optional[str] = None,

price_column: Optional[str] = None,

asset: str = "asset",

drop_invalid: bool = True,

) -> PriceData:The function first copies the input, so cleaning does not mutate the caller’s DataFrame. It then resolves columns through _resolve_column:

timestamp_column = _resolve_column(

frame, timestamp_column,

("timestamp", "datetime", "date", "time"),

"timestamp",

)

price_column = _resolve_column(

frame, price_column,

("price", "close", "adj_close", "adjusted_close"),

"price",

)Explicit names are safer when a file contains several possible price fields. For example, choosing close versus adjusted_close can materially change a historical experiment. Automatic inference is a convenience, not a substitute for documenting the choice.

The selected columns are renamed to the package’s stable internal names:

normalized = frame[[timestamp_column, price_column]].rename(

columns={timestamp_column: "timestamp", price_column: "price"}

)

normalized["timestamp"] = pd.to_datetime(

normalized["timestamp"], errors="coerce", utc=False

)

normalized["price"] = pd.to_numeric(normalized["price"], errors="coerce")Values that cannot be parsed become missing. The function then constructs a validity mask requiring a real timestamp and a finite, positive price:

valid = normalized["timestamp"].notna() & normalized["price"].notna()

valid &= np.isfinite(normalized["price"].to_numpy(dtype=float))

valid &= normalized["price"] > 0By default, invalid rows are removed. If drop_invalid=False, the function raises an error instead. The choice depends on the research context: dropping a corrupted row may be reasonable for a demonstration, but a production-quality study should usually stop and investigate why the row is invalid rather than silently deleting it.

5.3 Sorting and duplicate timestamps

After parsing, the function sorts by timestamp using a stable sort and removes duplicate timestamps by retaining the last source row:

normalized = (

normalized.sort_values("timestamp", kind="mergesort")

.drop_duplicates("timestamp", keep="last")

.reset_index(drop=True)

)This gives the downstream model one price per timestamp. It does not prove that the retained row is the correct observation. If duplicate rows represent separate trades, multiple venues, or different assets, they should be aggregated or separated before calling standardize_prices.

The duplicate policy is therefore an implementation convenience, not a fact recovered from the paper. The paper does not explain how duplicate timestamps or multiple records within one sampling interval were handled.

5.4 Loading a local CSV

load_price_csv is a thin file-system wrapper around standardize_prices:

def load_price_csv(

path: Union[str, Path],

*,

timestamp_column: Optional[str] = None,

price_column: Optional[str] = None,

asset: str = "asset",

drop_invalid: bool = True,

) -> PriceData:

source = Path(path)

if not source.exists() or not source.is_file():

raise FileNotFoundError(f"Price CSV does not exist: {source}")

if source.suffix.lower() != ".csv":

raise ValueError("load_price_csv accepts a local .csv file")

return standardize_prices(

pd.read_csv(source),

timestamp_column=timestamp_column,

price_column=price_column,

asset=asset,

drop_invalid=drop_invalid,

)The function deliberately accepts only a local .csv path. There are no HTTP requests, exchange clients, credentials, or hidden downloads. This is consistent with the project’s educational and offline scope.

The CLI exposes the same idea through the validate-data subcommand. Its local-path helper rejects URL-like strings before loading them:

def _safe_input_path(value: str) -> Path:

if "://" in value:

raise CLIError(

"Only local files are supported; URLs and network paths are not accepted"

)

path = Path(value).expanduser()

if not path.exists():

raise CLIError(f"Input file does not exist: {path}")

if not path.is_file():

raise CLIError(f"Input path is not a regular file: {path}")

return path.resolve()A local validation command can therefore be written as:

quant-trading-model validate-data prices.csv \

--timestamp-column timestamp \

--price-column close \

--asset goldThe command prints or writes a compact summary rather than training a model. This makes data inspection a separate step from forecasting and backtesting.

5.5 Keeping gold and Bitcoin separate

The PriceData representation is intentionally single-asset. A file may contain multiple assets, but the research pipeline should filter it into one chronologically ordered series per asset before creating windows. Gold and Bitcoin have different price scales, trading calendars, liquidity characteristics, and likely data sources. Combining them accidentally into one price sequence would make the next observation after a gold row appear to be a Bitcoin movement.

A multi-asset table can be filtered explicitly:

raw = pd.read_csv("historical_prices.csv")

gold = standardize_prices(

raw.loc[raw["asset"].eq("gold")],

timestamp_column="timestamp",

price_column="price",

asset="gold",

)

bitcoin = standardize_prices(

raw.loc[raw["asset"].eq("bitcoin")],

timestamp_column="timestamp",

price_column="price",

asset="bitcoin",

)Each result can then be passed independently to the window builder and forecasting experiment. This also makes it possible to record asset-specific provenance and fee assumptions. The paper’s headline results allocate $500 to each asset, but the extracted text does not identify whether the assets were sampled on matching dates or evaluated with identical calendars.

5.6 Synthetic data are for interfaces, not validation

Because the paper’s original datasets are unavailable, the project includes generate_synthetic_prices. It creates deterministic, positive price paths using a seeded random generator:

def generate_synthetic_prices(

*,

asset: str = "synthetic",

periods: int = 500,

start: Union[str, pd.Timestamp] = "2020-01-01",

seed: int = 7,

initial_price: Optional[float] = None,

) -> PriceData:The function chooses different illustrative drift and volatility defaults for labels containing gold or bitcoin, then constructs a positive path from exponentiated random shocks. The seed makes the example repeatable for teaching and invariant checks.

For example:

from quantitative_trading_model.data import generate_synthetic_prices

prices = generate_synthetic_prices(

asset="gold",

periods=500,

seed=7,

)

print(prices.asset)

print(prices.frame.head())The label-specific behavior is only a teaching convenience. A “Bitcoin-like” synthetic path is not Bitcoin data, and a “gold-like” path is not a gold instrument. Synthetic data can demonstrate that timestamps, windows, attention tensors, sizing budgets, and portfolio accounting have compatible interfaces. It cannot validate the paper’s forecast metrics, fee curves, or reported final values.

5.7 Data checks before modeling

Before moving to sliding windows, record at least the following:

The generated tests in tests/test_data_and_streaks.py are intended to check these kinds of invariants with small hand-built fixtures. They are static artifacts in this project review; no claim is made here that the generated test suite was executed successfully.

The essential principle is simple: clean only what the data contract justifies, preserve timestamps, separate assets, and document every assumption before training. Once the local series is trustworthy and its provenance is recorded, the next step is to construct the paper’s 100-observation windows without allowing scaling or temporal partitioning to leak future information.

6. Build Leakage-Safe Sliding Windows

The paper describes a sliding-window forecasting setup with a history of 100 observations and a stride of one. The model reads the latest 100 observations, predicts a later value, advances one observation, and creates the next overlapping example.

The important issue is not only the window size. Every forecast must use information available at its decision timestamp. The target must occur after the input window, scaling parameters must be fitted without future observations, and evaluation must preserve chronological order.

6.1 The one-step relationship

Let z_t denote a transformed price or feature value at time t. With a window length of 100, a one-step sample is:

\[ Xt = [z{t-99}, z{t-98}, \ldots, z{t-1}, zt], \qquad yt = z_{t+1}. \]

The final value in X_t is the latest information available when the forecast is generated. The target belongs to the next observation.

The paper-inspired window settings are represented by DataConfig:

@dataclass

class DataConfig:

timestamp_column: str = "timestamp"

price_column: str = "price"

window_length: int = 100

stride: int = 1window_length=100 and stride=1 come from the paper. The paper does not clearly state whether the model uses raw prices, normalized prices, returns, or additional features, so the representation remains an explicit implementation choice.

6.2 How make_windows constructs samples

The central function is make_windows in src/quantitative_trading_model/data.py. It accepts a cleaned PriceData object, a DataFrame, or a numeric array. For timestamp-aware inputs, it stores the start, end, and target timestamps alongside the arrays.

The core operation is equivalent to:

for start in range(0, last_start + 1, stride):

end = start + window_length - 1

X.append(transformed[start : end + 1])

targets.append(transformed[end + 1 : end + 1 + horizon, 0])

target_times.append(timestamps[end + horizon])With the defaults, the first sample contains observations 0 through 99 and targets observation 100. The next sample contains observations 1 through 100 and targets observation 101.

The returned WindowedDataset includes temporal metadata:

@dataclass(frozen=True)

class WindowedDataset:

X: np.ndarray

y: np.ndarray

window_start: pd.DatetimeIndex

window_end: pd.DatetimeIndex

y_timestamp: pd.DatetimeIndex

feature_names: Tuple[str, ...] = ("price",)Its invariant check requires every target timestamp to follow the corresponding input window:

if n and not (self.y_timestamp > self.window_end).all():

raise ValueError("Every target timestamp must be after its input window")This timestamp guarantee applies when the input carries timestamps, such as PriceData or a cleaned DataFrame. For a raw numeric array, the current implementation has no timestamp argument in that code path and creates placeholder daily timestamps beginning at 1970-01-01. Those generated timestamps preserve array alignment for shape-based demonstrations, but they are not source-market timestamps. A trading experiment should therefore use PriceData or a timestamp-aware DataFrame.

6.3 One-day versus three-day targets

The paper is ambiguous about the forecast horizon. Its prediction discussion is compatible with one-step forecasting, while its conclusion refers to forecasts for the next three days. The implementation exposes horizon rather than silently choosing one interpretation.

For horizon=1:

X.shape = (samples, 100, features)

y.shape = (samples,)For horizon=3:

\[ yt = [z{t+1}, z{t+2}, z{t+3}]. \]

The shape is then:

X.shape = (samples, 100, features)

y.shape = (samples, 3)The final target timestamp is the timestamp of z_{t+3}. Converting a three-value forecast into a buy, sell, or hold decision belongs to the strategy layer. Possible rules include using the terminal forecast, the mean forecast, or a separately specified multi-day signal.

For a series of N observations, the number of stride-one windows is:

N−100−h+1,

where h is the forecast horizon. The final window must leave enough observations for every target value.

6.4 Overlapping windows and temporal partitions

Stride one creates heavily overlapping samples:

window 1: [0, 1, 2, ..., 99] -> target 100

window 2: [1, 2, 3, ..., 100] -> target 101This overlap is normal for sliding-window forecasting. The risk comes from treating neighboring samples as independent random observations. If windows are randomly shuffled before splitting, almost identical histories can appear in both partitions, producing optimistic estimates.

The generated recurrent training code therefore uses non-shuffled batches:

train_loader = DataLoader(

TensorDataset(torch.from_numpy(x_train), torch.from_numpy(y_train)),

batch_size=batch_size,

shuffle=False,

)chronological_split also preserves sample order. This prevents random cross-partition mixing, but it does not guarantee that raw input histories are disjoint at the boundary. The final training window and first test window may still share observations because the windows overlap by design. That dependence should be acknowledged when interpreting metrics; walk-forward evaluation and a documented gap can provide a stricter protocol.

6.5 Fit scaling on training observations only

Scaling can make neural-network optimization easier, but fitting a scaler on the complete series leaks future distribution information. For example, a full-series min-max scaler exposes the training process to the future minimum and maximum.

The repository provides ChronologicalScaler:

scaler = ChronologicalScaler()

scaler.fit(training_values) # training rows only

train_scaled = scaler.transform(train_values)

test_scaled = scaler.transform(test_values)The safe sequence is:

Clean and sort the complete local file.

Establish the chronological raw-row training boundary.

Fit the scaler only on rows before that boundary.

Transform later rows with the fitted scaler.

Build windows and retain their timestamps.

Inverse-transform predictions before reporting price-level metrics when appropriate.

make_windows accepts an already fitted scaler. Its fit_scaler option is intended for controlled demonstrations; setting fit_scaler=True on the complete dataset before an out-of-sample experiment would leak future information. The window builder does not know whether the caller selected a valid training boundary and cannot enforce this policy automatically.

A safer pattern is:

train_rows = price_data.frame.iloc[:training_row_count]

scaler = ChronologicalScaler().fit(

train_rows[["price"]].to_numpy(dtype=float)

)

windows = make_windows(

price_data,

window_length=100,

horizon=1,

stride=1,

scaler=scaler,

fit_scaler=False,

)Here, training_row_count must be determined from a documented chronological rule, such as a date boundary or a fixed initial training period. It must not be chosen after inspecting test performance. If windows are built from the entire transformed series and then split, the scaler remains training-fitted, but boundary overlap still exists; a stricter workflow can build or select partitions around an explicit raw-row boundary.

6.6 Chronological 70:30 splitting

The paper reports a 70:30 train/test split. The implementation provides chronological_split for a paper-style comparison:

train, test = chronological_split(

dataset,

train_fraction=0.70,

validation_fraction=0.0,

)The function slices ordered samples rather than randomly selecting indices. With validation data, the order is:

training windows -> validation windows -> test windowsThe metadata-preserving helper is conceptually:

def dataset_slice(dataset, start, stop):

return WindowedDataset(

X=dataset.X[start:stop],

y=dataset.y[start:stop],

window_start=dataset.window_start[start:stop],

window_end=dataset.window_end[start:stop],

y_timestamp=dataset.y_timestamp[start:stop],

feature_names=dataset.feature_names,

)A useful ordering check is:

train_times = train.y_timestamp

test_times = test.y_timestamp

assert train_times.max() < test_times.min()This confirms that target timestamps are ordered across the sample split. It does not prove that the corresponding input histories are disjoint, because stride-one windows can overlap at the boundary.

The exact boundary remains a reconstruction. The paper does not specify the split date or whether it splits raw observations before window construction or partitions already-created windows. Those choices can produce different edge behavior and should be recorded in experiment metadata.

6.7 Walk-forward evaluation for trading conclusions

A single 70:30 split answers only how one fixed training period performs on one later period. It does not show how results change as new observations arrive.

An expanding walk-forward procedure repeatedly preserves the information boundary:

train on [0, ..., t]

forecast the next block

advance the boundary

expand the training set

forecast the next block

repeatThe walk_forward_splits generator is used like this:

for train, validation, test in walk_forward_splits(

dataset,

initial_train_size=500,

validation_size=0,

test_size=20,

step=20,

):

# Fit only on train, optionally tune on validation,

# then evaluate on the later test block.

passEach test block follows its training block. The training set expands over time; a rolling fixed-length training window would be another explicit choice.

The paper does not report walk-forward results, so such results are not reproductions of its tables. They are a more appropriate protocol for trading conclusions because they repeatedly test the model on observations that follow the fitting period.

6.8 What the generated test artifact actually demonstrates

The generated tests/test_data_and_streaks.py uses a compatibility helper with a numeric price array and a separate timestamp object. In the current make_windows implementation, the numeric-array path does not accept or preserve that separate timestamp argument; it creates placeholder daily timestamps. Therefore, the test's meaningful checks are the numeric window boundaries and target values, while its timestamp behavior should not be interpreted as validation of real source timestamps.

A timestamp-aware illustrative example, using the public data contract directly, is:

prices = np.arange(10.0, 17.0)

timestamps = pd.date_range(

"2024-01-01", periods=len(prices), freq="D"

)

price_data = PriceData(

pd.DataFrame({"timestamp": timestamps, "price": prices})

)

dataset = make_windows(

price_data,

window_length=3,

horizon=1,

stride=1,

)

np.testing.assert_allclose(dataset.y, prices[3:])