Revolutionizing Stock Predictions with ARIMA-SVM Hybrid Models

Bridging Traditional Statistics and Machine Learning for Unmatched Financial Accuracy

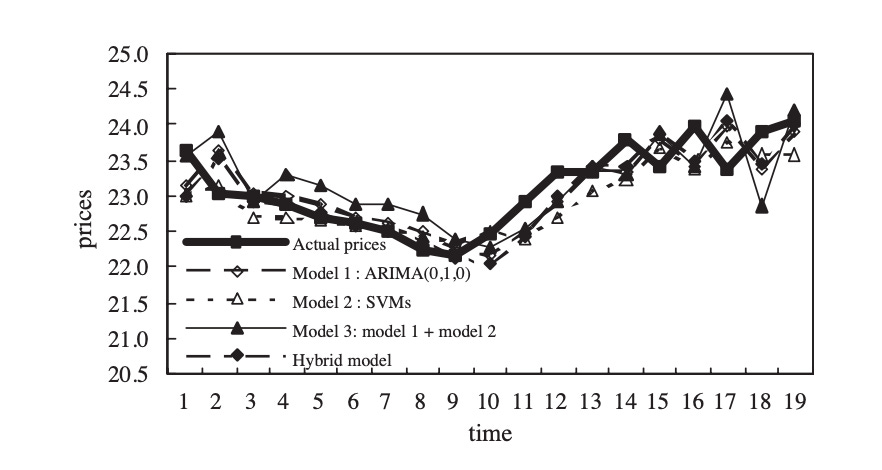

Forecasting stock prices remains one of the most challenging tasks in the realm of financial analysis and investment strategy. The inherent volatility and complexity of financial markets make accurate prediction a formidable endeavor. Effective stock price forecasting is crucial for investors, portfolio managers, and financial institutions as it informs decision-making processes, risk management, and strategic planning. However, the dynamic nature of stock markets, influenced by a myriad of economic indicators, investor sentiment, geopolitical events, and unforeseen market shocks, adds layers of complexity to predictive modeling.

One of the primary challenges in stock price forecasting is the dual nature of the data, which exhibits both linear and nonlinear behaviors. Linear patterns in stock prices can often be attributed to predictable trends and cycles, making them amenable to traditional statistical models. These models, such as the Autoregressive Integrated Moving Average (ARIMA), have long been the cornerstone of time series analysis due to their effectiveness in capturing linear dependencies and forecasting future values based on historical data. ARIMA models excel in modeling and forecasting linear trends, seasonal variations, and other straightforward temporal structures inherent in financial time series data.

Despite their strengths, traditional statistical models like ARIMA face significant limitations when confronted with the nonlinear complexities of stock prices. Financial markets are influenced by a multitude of factors that interact in nonlinear ways, leading to abrupt changes, regime shifts, and patterns that traditional linear models fail to capture accurately. These nonlinear behaviors can stem from sudden economic policy changes, technological advancements, market sentiment shifts, and other exogenous shocks that disrupt the linear continuity assumed by models like ARIMA. As a result, reliance solely on linear models can lead to substantial forecasting errors, reducing the reliability and effectiveness of investment strategies based on such predictions.