Stock Market Prediction Using Machine Learning

Part 5/10 In the rapidly evolving world of algorithmic trading, machine learning (ML) has emerged as a revolutionary force, reshaping how market predictions are made.

Unlike traditional statistical methods, ML leverages massive datasets and complex algorithms to uncover hidden patterns in financial time series data. In this chapter, we explore the integration of advanced statistical and machine learning techniques into market prediction frameworks. We begin with the theoretical underpinnings of these techniques and proceed through a detailed discussion of implementation strategies. Finally, we present a series of complex function implementations that not only demonstrate advanced coding patterns but also illustrate how these components interconnect within a cohesive backtesting and prediction system.

Please read the previous parts here:

This chapter serves as a natural extension to our earlier discussions on vectorized backtesting, wherein we focused on efficient simulation and evaluation of trading strategies. Here, the focus shifts toward forecasting future market movements using state-of-the-art machine learning models — from classical linear and logistic regression to deep neural networks. We emphasize the importance of historical returns, feature extraction, and time-series cross-validation techniques that ensure robust and generalizable predictions.

Theoretical Foundations of Market Prediction

Machine learning has transformed many fields, and finance is no exception. In financial markets, ML models are used to predict price movements, forecast volatility, and even to determine optimal asset allocations. At a high level, these models rely on historical data — such as past returns, trading volumes, and technical indicators — to learn patterns and make predictions about future price behavior.

The success of machine learning in market prediction is driven by its ability to capture non-linear relationships in the data, which classical econometric models often fail to model. Techniques ranging from simple linear regression to deep learning models such as convolutional neural networks (CNNs) and recurrent neural networks (RNNs) have been applied to forecast market trends. In many cases, these models transform raw market data into a high-dimensional feature space, enabling them to identify subtle correlations that might be imperceptible to human analysts.

Mathematical Models and Statistical Techniques

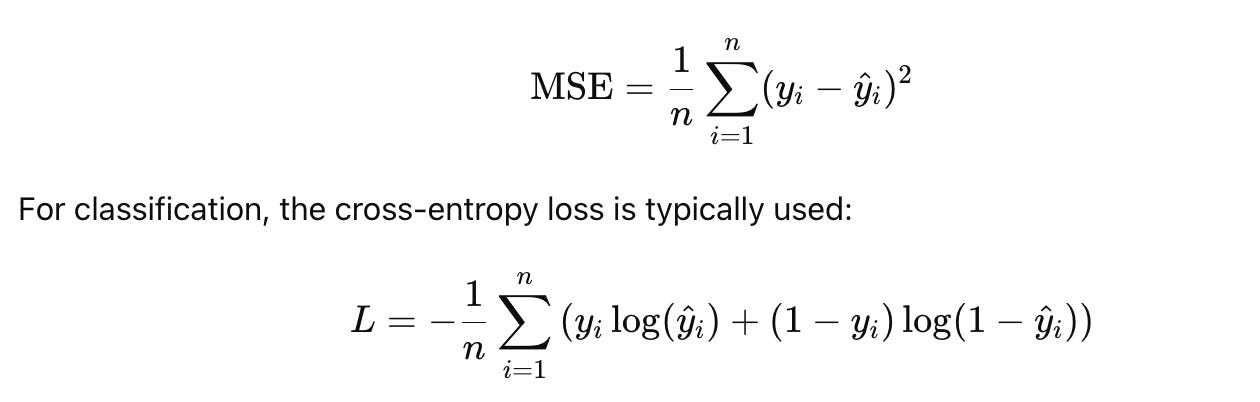

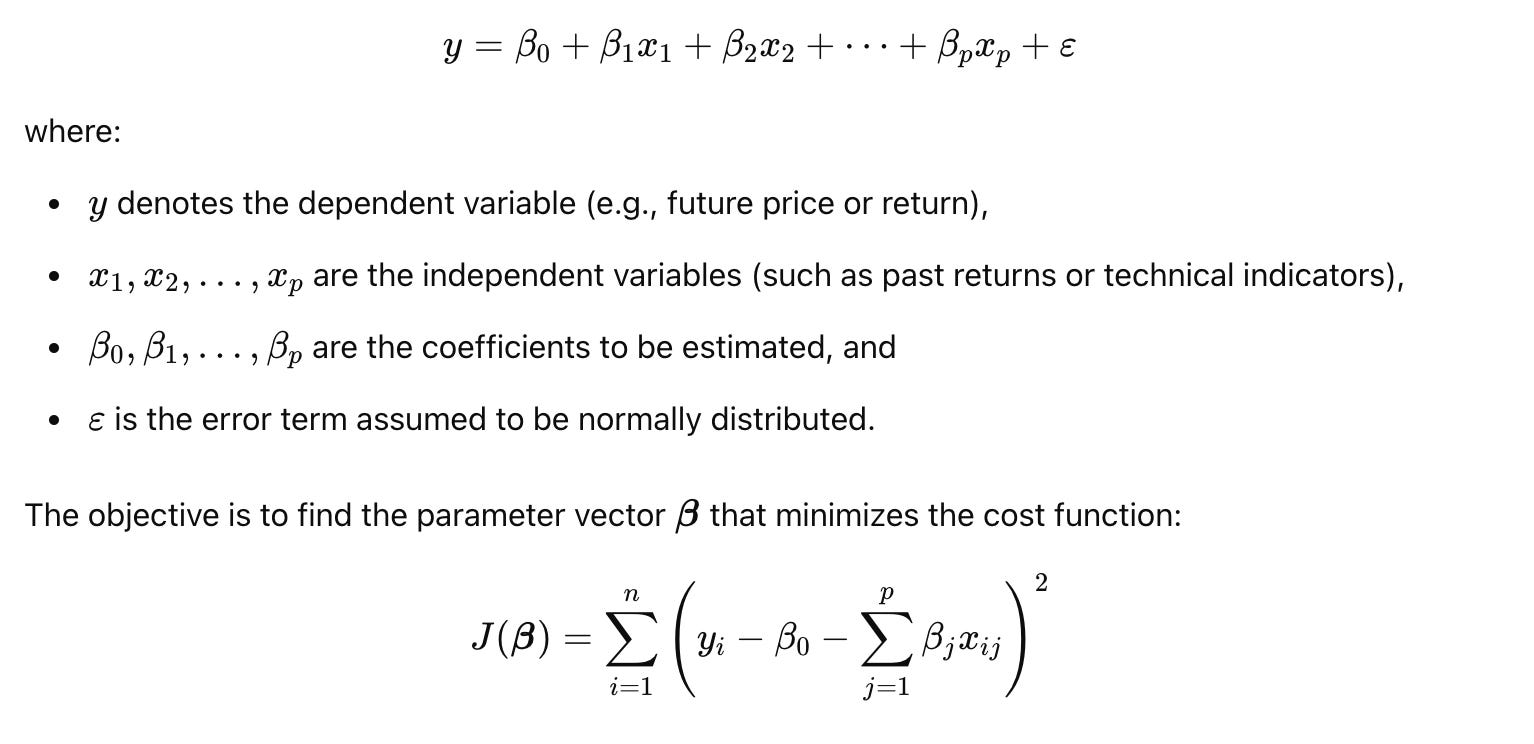

At the core of market prediction lie several key mathematical and statistical models. Traditional approaches, such as linear regression, assume a linear relationship between the dependent variable (e.g., future returns) and independent variables (e.g., past returns, technical indicators). The mathematical formulation of linear regression is typically given as:

In contrast, logistic regression is used when the prediction problem is formulated as a classification task — such as predicting the direction of price movement (up or down). The logistic function is defined as:

This probabilistic output enables traders to gauge the confidence of the predictions, which is crucial for risk management.

For capturing non-linear dynamics, neural networks have gained prominence. A neural network consists of multiple layers of interconnected neurons. The simplest feedforward neural network (or multilayer perceptron) computes:

activation function. Recurrent neural networks (RNNs), and their variants such as LSTMs and GRUs, are particularly effective for time-series forecasting as they can capture temporal dependencies.

When integrating machine learning models into a market prediction system, it is crucial to design an architecture that supports efficient data ingestion, preprocessing, model training, and prediction. The core architecture typically comprises the following layers:

Data Ingestion and Preprocessing:

Efficient retrieval and cleaning of high-frequency market data.

Normalization, outlier detection, and feature extraction (e.g., calculating moving averages, RSI, etc.).

Feature Engineering Layer:

Transformation of raw data into meaningful features.

Use of vectorized operations (via Pandas and NumPy) to generate indicators and lagged features.

Model Training and Evaluation:

Implementation of various predictive models (linear, logistic, neural networks).

Use of cross-validation techniques (expanding or rolling windows) to prevent overfitting.

Integration with vectorized backtesting frameworks to simulate model predictions in a trading environment.

Prediction and Signal Generation:

Real-time inference on new data.

Dynamic updating of trading signals based on model predictions.

Performance and Risk Management:

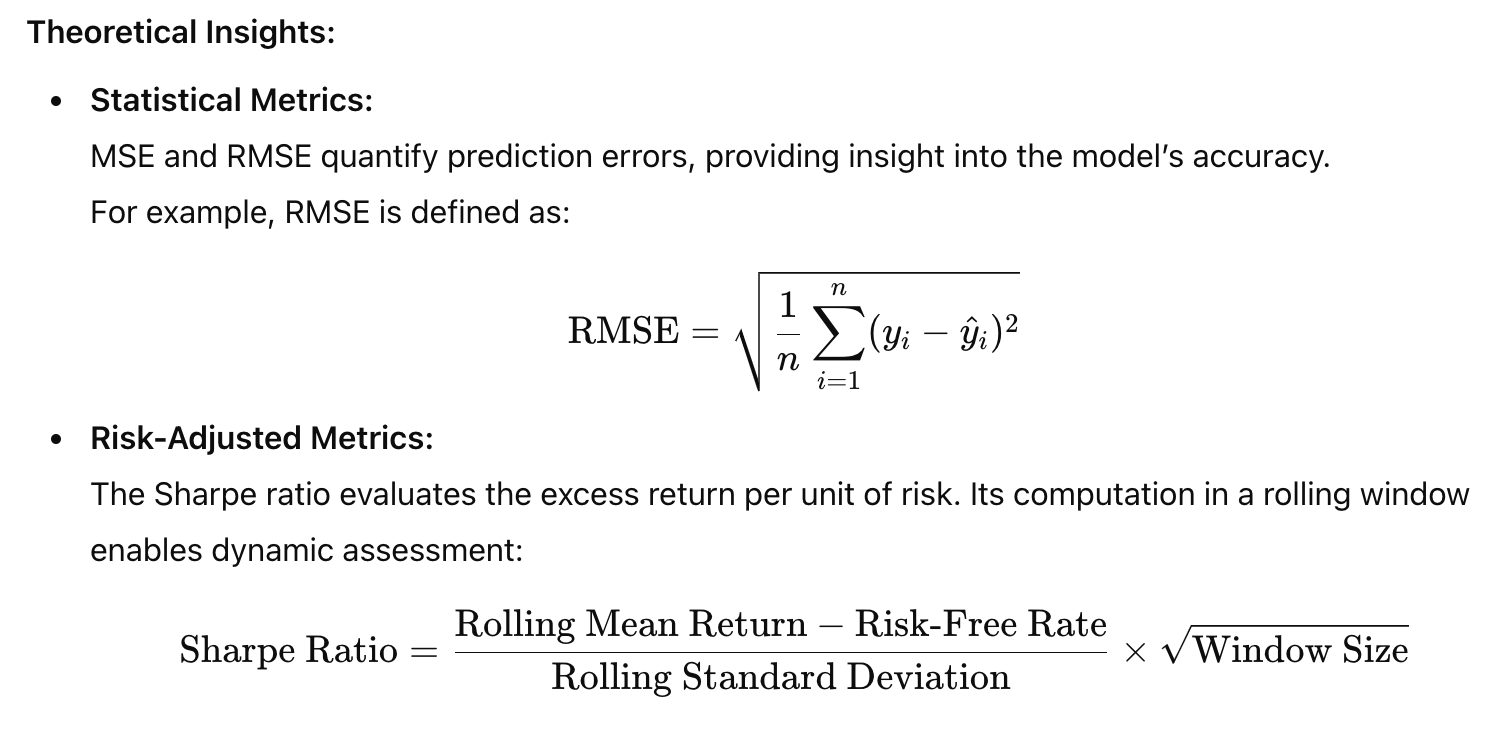

Continuous evaluation of model performance using metrics such as RMSE, accuracy, Sharpe ratio, etc.

Adaptive optimization to recalibrate models in response to changing market conditions.

This layered architecture ensures that machine learning models can be seamlessly integrated into existing backtesting systems, enabling the transition from historical simulation to real-time market prediction.

Implementation Strategy for Market Prediction Models

Before any machine learning model can be applied, financial data must be preprocessed and transformed into a suitable format. Data preprocessing involves handling missing values, normalizing features, and performing time-series transformations. A critical step is the extraction of features such as lagged returns, moving averages, and momentum indicators. These features serve as the inputs to the ML models and are crucial for capturing the temporal dynamics of financial markets.

Normalization is particularly important because financial data can vary greatly in scale. Techniques such as min-max scaling or z-score normalization are used to ensure that features contribute equally to model training. Vectorized operations in Pandas and NumPy are leveraged to perform these transformations efficiently on large datasets.

Model Selection and Training

The next layer in our implementation strategy is model selection and training. Here, the goal is to choose an appropriate predictive model based on the nature of the prediction task. For regression tasks — predicting future returns — linear regression or more sophisticated non-linear regression models may be employed. For classification tasks — predicting whether the market will go up or down — logistic regression and neural networks are common choices.

Design decisions in model training include:

Cost Function Selection:

For regression, the mean squared error (MSE) is a common cost function:

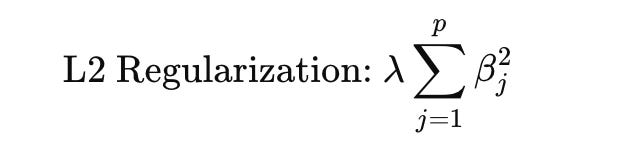

Regularization:

Techniques such as L1 (Lasso) and L2 (Ridge) regularization are employed to prevent overfitting by penalizing large coefficients:

Optimization Algorithms:

Gradient descent and its variants (e.g., stochastic gradient descent, Adam optimizer) are used to minimize the cost function.Cross-Validation Techniques:

Given the temporal nature of financial data, time-series cross-validation (e.g., walk-forward validation) is applied to ensure that the model is robust and does not overfit to historical data.

Integration with Backtesting Frameworks

Integrating machine learning predictions into a backtesting framework requires a seamless connection between the predictive model and the trading simulation engine. The prediction model outputs, whether continuous predictions of returns or binary trading signals, are used to generate trading decisions within the backtesting system.

The integration points include:

Signal Transformation:

Converting model outputs into actionable signals (e.g., buy, sell, hold).Dynamic Updating:

As new data arrives, the model makes real-time predictions that update the trading signals.Performance Monitoring:

The predictive performance is continuously evaluated against actual market returns, feeding back into model retraining and parameter adjustment.

This integration is critical to close the loop between market prediction and execution, ensuring that the backtesting framework not only simulates historical performance but also adapts to live market dynamics.

Code Implementations for Market Prediction Models

In this section, we provide advanced code implementations for three key predictive models: advanced linear regression, logistic regression for trend classification, and deep neural network predictors. Each implementation is preceded by a detailed explanation covering theoretical underpinnings, algorithmic breakdown, and system integration points. All code examples focus solely on the complex functions and their critical algorithms.

Advanced Linear Regression for Market Prediction

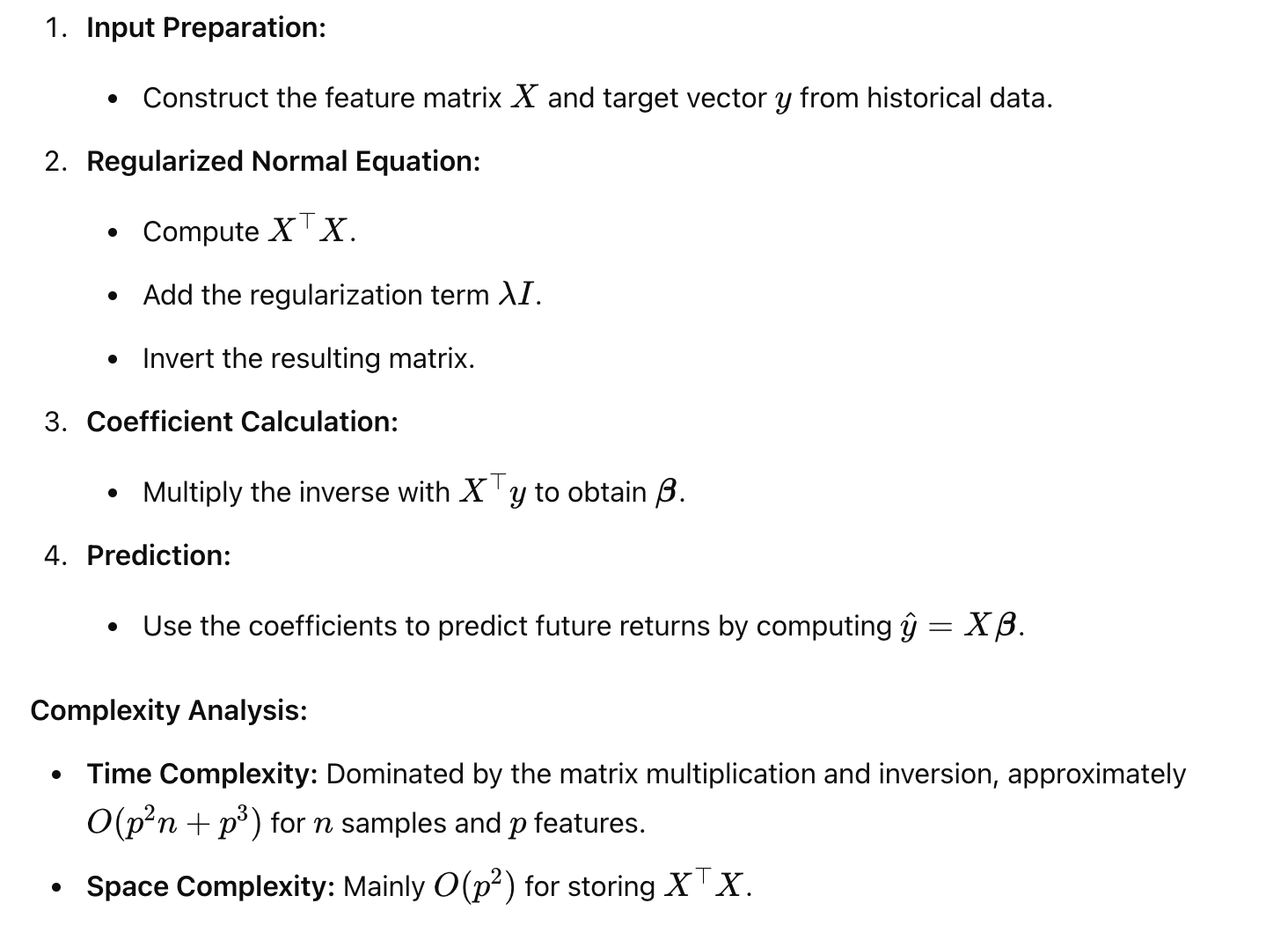

Linear regression remains a foundational technique in market prediction due to its interpretability and ease of implementation. In a financial context, linear regression can be employed to forecast future returns based on a set of historical features. Our advanced implementation extends the traditional linear regression model by incorporating regularization (Ridge regression) to prevent overfitting and by leveraging vectorized operations for high performance.

Design Decisions and Optimization Strategies:

Algorithm Breakdown

def advanced_linear_regression_predictor(X, y, X_new, regularization_lambda):

"""

Predict future returns using advanced linear regression with L2 regularization.

Parameters:

X: A 2D numpy array (n x p) representing the feature matrix for historical data.

y: A 1D numpy array (n,) representing the target returns.

X_new: A 2D numpy array (m x p) representing the feature matrix for new data.

regularization_lambda: A scalar for the L2 regularization parameter.

Returns:

predictions: A 1D numpy array of predicted returns for the new data.

"""

# Compute the regularized normal equation solution: beta = (X^T X + lambda*I)^(-1) X^T y

XtX = X.T.dot(X)

regularizer = regularization_lambda * np.eye(XtX.shape[0])

beta = np.linalg.inv(XtX + regularizer).dot(X.T).dot(y)

# Generate predictions for new data

predictions = X_new.dot(beta)

return predictionsLogistic Regression for Trend Prediction

Logistic regression is widely used for binary classification tasks, such as predicting the direction of market movement. In our application, the model classifies whether the market will move upward or downward based on historical features. The logistic function is defined as:

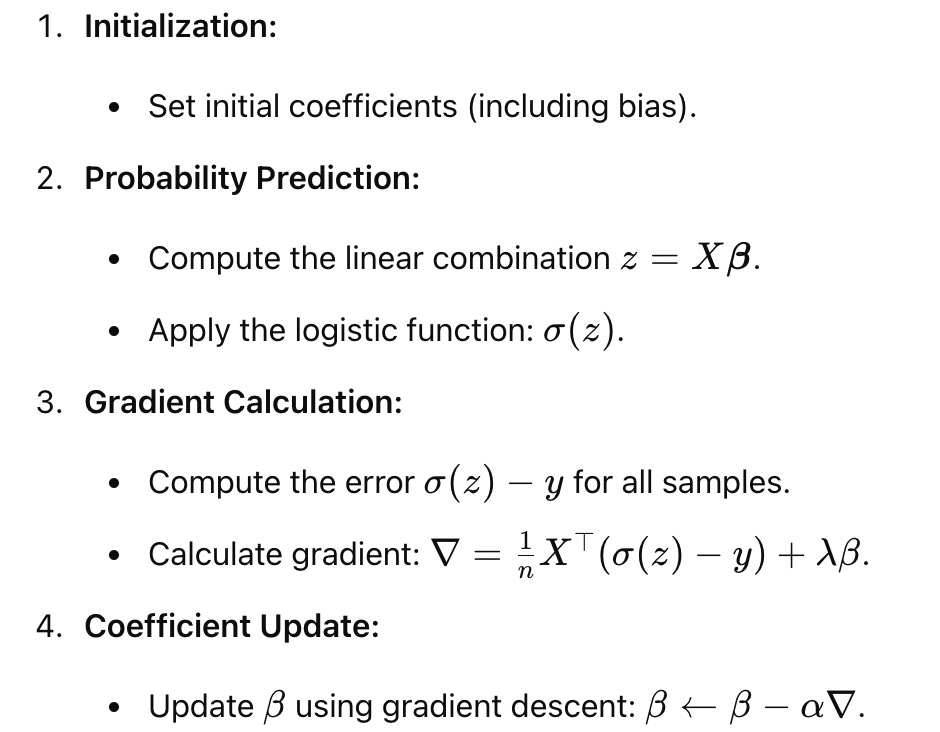

This model outputs probabilities that are then thresholded to generate trading signals. Our advanced implementation uses vectorized operations to compute the gradient of the cost function (cross-entropy loss) and update the coefficients using gradient descent. We also integrate regularization to mitigate overfitting.

Design Decisions and Optimization Strategies:

Vectorized Gradient Computation: Efficiently computes gradients across all observations simultaneously.

Adaptive Learning: Implements a dynamic learning rate for convergence.

Regularization: Includes L2 penalty to balance model complexity.

Edge Cases: Handles cases where predicted probabilities approach 0 or 1 to prevent numerical instability.

Algorithm Breakdown

def logistic_regression_trend_predictor(X, y, X_new, learning_rate, regularization_lambda, iterations):

"""

Predict market direction using logistic regression with L2 regularization.

Parameters:

X: A 2D numpy array (n x p) representing the feature matrix for training data.

y: A 1D numpy array (n,) with binary labels (0 or 1) for market direction.

X_new: A 2D numpy array (m x p) representing the feature matrix for new data.

learning_rate: A scalar representing the learning rate for gradient descent.

regularization_lambda: L2 regularization parameter.

iterations: Number of iterations to run the gradient descent.

Returns:

predictions: A 1D numpy array of predicted probabilities for the new data.

"""

n, p = X.shape

beta = np.zeros(p) # Initialize coefficients

for _ in range(iterations):

# Compute predictions using the logistic function

z = X.dot(beta)

predictions = 1 / (1 + np.exp(-z))

# Compute error and gradient with regularization

error = predictions - y

gradient = (X.T.dot(error) / n) + regularization_lambda * beta

# Update coefficients

beta -= learning_rate * gradient

# Predict probabilities for new data

z_new = X_new.dot(beta)

new_predictions = 1 / (1 + np.exp(-z_new))

return new_predictionsDeep Neural Network for Financial Forecasting

Deep neural networks (DNNs) are capable of modeling highly non-linear relationships, making them ideal for complex tasks such as financial forecasting. In this advanced implementation, we focus on constructing a feedforward neural network designed to predict future market returns. The network architecture includes multiple hidden layers with non-linear activation functions (e.g., ReLU) and an output layer that produces a continuous prediction.

The training process leverages backpropagation, where the network weights are updated by minimizing a loss function — typically the mean squared error (MSE) for regression tasks. We integrate advanced optimization techniques such as the Adam optimizer for faster convergence and include dropout layers to mitigate overfitting. The vectorized implementation ensures that forward and backward passes are computed efficiently, even when processing large batches of data.

Design Decisions and Optimization Strategies:

Layered Architecture:

Multiple hidden layers allow the network to learn hierarchical features from the data.Activation Functions:

ReLU activation functions improve training speed by avoiding vanishing gradients.Optimization:

The Adam optimizer is used for adaptive learning rate adjustments.Regularization:

Dropout is applied to prevent overfitting by randomly deactivating neurons during training.Batch Processing:

Training is performed in mini-batches using vectorized operations to leverage parallel computing capabilities.

Algorithm Breakdown

def deep_neural_network_predictor(X, y, X_new, layers, learning_rate, epochs, dropout_rate):

"""

Predict future market returns using a deep neural network.

This function implements a multi-layer feedforward neural network with dropout and uses the Adam optimizer

for training. It returns continuous predictions for new market data.

Parameters:

X: A 2D numpy array (n x p) for training features.

y: A 1D numpy array (n,) for target returns.

X_new: A 2D numpy array (m x p) for new feature data.

layers: A list defining the number of neurons in each hidden layer.

learning_rate: Learning rate for the optimizer.

epochs: Number of training epochs.

dropout_rate: Fraction of neurons to drop for regularization.

Returns:

predictions: A 1D numpy array of predicted returns for the new data.

"""

# Initialize weights and biases for each layer

params = {}

input_dim = X.shape[1]

layer_dims = [input_dim] + layers + [1]

L = len(layer_dims) - 1 # Total layers (excluding input)

for l in range(1, L + 1):

params['W' + str(l)] = np.random.randn(layer_dims[l], layer_dims[l-1]) * 0.01

params['b' + str(l)] = np.zeros((layer_dims[l], 1))

# Adam optimizer parameters

adam_params = {key: np.zeros_like(val) for key, val in params.items()}

beta1, beta2, epsilon = 0.9, 0.999, 1e-8

def relu(Z):

return np.maximum(0, Z)

def relu_derivative(Z):

return (Z > 0).astype(float)

def forward_propagation(X, params, dropout_masks=None):

caches = {}

A = X.T

caches['A0'] = A

for l in range(1, L + 1):

W = params['W' + str(l)]

b = params['b' + str(l)]

Z = W.dot(A) + b

caches['Z' + str(l)] = Z

if l != L:

A = relu(Z)

# Apply dropout if mask provided

if dropout_masks is not None and 'D' + str(l) in dropout_masks:

A *= dropout_masks['D' + str(l)]

A /= (1 - dropout_rate)

else:

A = Z # Linear activation for output layer

caches['A' + str(l)] = A

return A, caches

def compute_cost(A_final, y):

m = y.shape[0]

cost = np.sum((A_final.flatten() - y) ** 2) / (2 * m)

return cost

# Training loop

m = X.shape[0]

for epoch in range(epochs):

# Generate dropout masks for each hidden layer

dropout_masks = {}

for l in range(1, L):

A_prev = np.random.rand(params['W' + str(l)].shape[1], 1)

dropout_masks['D' + str(l)] = (np.random.rand(*params['W' + str(l)].shape) > dropout_rate).astype(float)

# Forward propagation

A_final, caches = forward_propagation(X, params, dropout_masks)

cost = compute_cost(A_final, y)

# Backward propagation

grads = {}

dA = (A_final.flatten() - y).reshape(1, -1) / m

for l in reversed(range(1, L + 1)):

dZ = dA

if l != L:

dZ *= relu_derivative(caches['Z' + str(l)])

A_prev = caches['A' + str(l - 1)]

grads['dW' + str(l)] = dZ.dot(A_prev.T)

grads['db' + str(l)] = np.sum(dZ, axis=1, keepdims=True)

if l > 1:

dA = params['W' + str(l)].T.dot(dZ)

# Adam update

for l in range(1, L + 1):

for param in ['W', 'b']:

key = param + str(l)

adam_params[key] = beta1 * adam_params[key] + (1 - beta1) * grads['d' + key]

params[key] -= learning_rate * adam_params[key]

# Final prediction on new data (no dropout during inference)

A_final_new, _ = forward_propagation(X_new, params)

predictions = A_final_new.flatten()

return predictionsIntegration of Model Predictions into Backtesting Framework

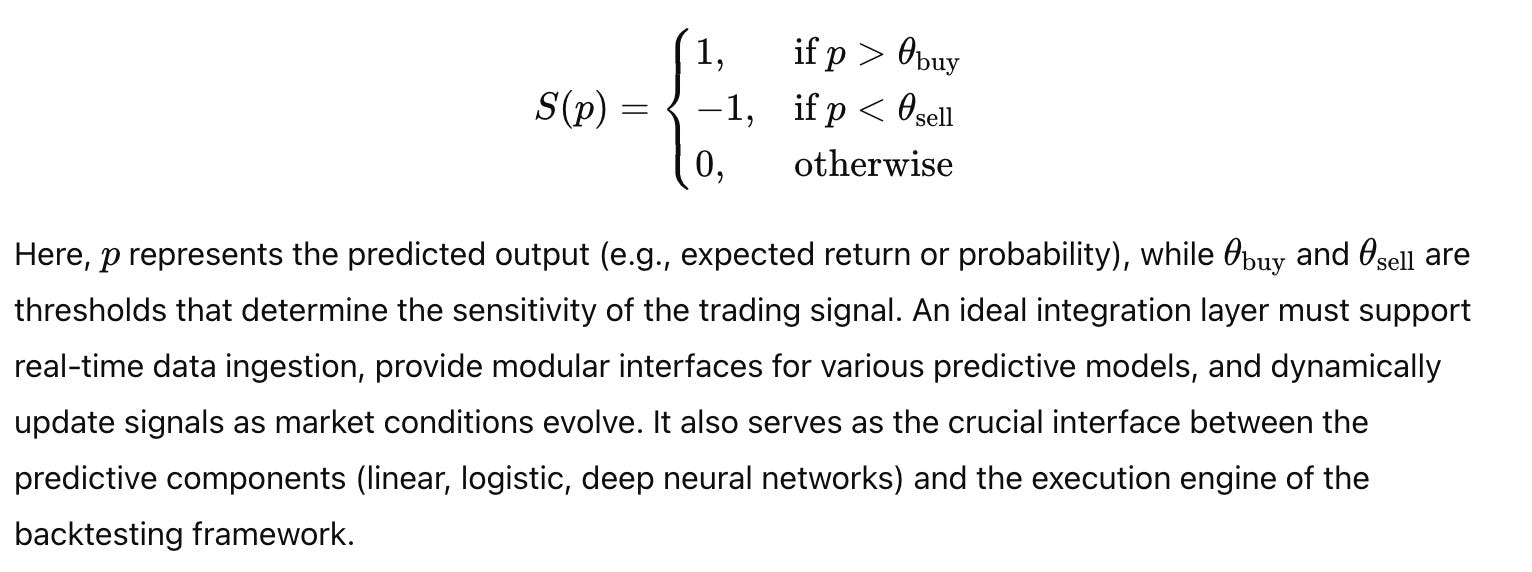

Integrating market predictions from machine learning models into a backtesting framework requires a robust interface that seamlessly converts model outputs into trading signals. These predictions — whether they come from linear regression, logistic regression, or deep neural networks — are used to generate actionable trading decisions. The process involves mapping continuous predictions into discrete signals (buy, sell, or hold) and dynamically updating these signals as new data becomes available.

Our approach is to build a signal integration module that ingests predictions from any predictive model and transforms them into trading decisions based on predefined thresholds. This module plays a critical role in ensuring that the forecasting component aligns with the execution engine of the backtesting framework. It uses vectorized operations to handle large volumes of prediction data, thus maintaining low latency and high throughput.

Key design aspects include:

Thresholding and Signal Discretization:

Convert continuous predictions into binary or multi-class signals.Dynamic Updating:

Continuously integrate new predictions and adjust positions in real time.Modular Integration:

The function is designed to work with outputs from various models, ensuring that the overall system remains flexible and scalable.

Algorithm Breakdown

Input Acquisition:

Retrieve prediction arrays from one or more machine learning models.

Signal Transformation:

Apply thresholding to convert continuous predictions to discrete signals.

Signal Aggregation:

Combine signals from multiple models if ensemble predictions are used.

Integration with Trading System:

Update the backtesting DataFrame with the new trading signals.

Performance Monitoring:

Evaluate the effectiveness of the predictions by comparing them with actual market returns.

def integrate_predictions_into_signals(predictions, threshold_buy, threshold_sell):

"""

Integrate continuous market predictions into discrete trading signals.

This function converts model outputs into trading signals using predefined thresholds.

A signal of 1 indicates a buy, -1 indicates a sell, and 0 indicates a hold.

Parameters:

predictions: A 1D numpy array of continuous predictions (e.g., expected returns).

threshold_buy: The minimum value of prediction to trigger a buy signal.

threshold_sell: The maximum value of prediction to trigger a sell signal.

Returns:

trading_signals: A 1D numpy array of discrete trading signals.

"""

# Vectorized thresholding: if prediction > threshold_buy then 1, if prediction < threshold_sell then -1, else 0

trading_signals = np.where(predictions > threshold_buy, 1, np.where(predictions < threshold_sell, -1, 0))

return trading_signalsPerformance, Optimization, and Future Directions

The final layer of our market prediction framework involves a rigorous evaluation of model performance and the optimization of predictive algorithms. Performance metrics such as mean squared error (MSE), root mean squared error (RMSE), and classification accuracy provide quantitative measures of how well the models predict market movements. In a trading context, risk-adjusted performance metrics — like the Sharpe ratio — are essential to assess the trade-off between returns and volatility.

Optimization Strategies and Tradeoffs

Effective optimization of machine learning models in market prediction involves balancing model complexity, computational efficiency, and generalization performance. Overly complex models risk overfitting, whereas simpler models might not capture the full spectrum of market dynamics. Techniques such as hyperparameter tuning, regularization, and cross-validation are crucial. Advanced optimization methods, including Bayesian optimization and evolutionary algorithms, can further refine model parameters while minimizing overfitting.

Performance and Risk Considerations:

Overfitting Mitigation:

Employing cross-validation (e.g., time-series cross-validation) and walk-forward validation ensures models generalize well.Regularization:

Both L1 and L2 regularization help penalize overly complex models.Ensemble Methods:

Combining predictions from multiple models can reduce variance and enhance robustness.Hardware Optimization:

Using GPUs and specialized hardware accelerators can further reduce training time, especially for deep learning models.

Future Directions in Market Prediction

Looking forward, the integration of machine learning into market prediction is poised for significant advancements:

Reinforcement Learning:

Adaptive models that learn optimal trading policies through interactions with the market environment.Real-Time Adaptation:

Models that continuously update with streaming data, leveraging online learning techniques.Hybrid Models:

Combining deterministic models with stochastic simulations to capture both trend persistence and market randomness.Enhanced Feature Engineering:

Incorporating alternative data sources (e.g., sentiment analysis, news analytics) to improve predictive power.Explainability:

Developing interpretable machine learning models to provide insights into decision-making processes, aiding regulatory compliance and trust in automated trading systems.

Types of Trading Strategies Covered

In this section, we delve into the various trading strategies that leverage machine learning techniques for market prediction. Building upon our earlier discussion on the integration of machine learning models into a vectorized backtesting framework, we now focus on three primary strategy classes: Linear Regression-Based Strategies, Machine Learning-Based Strategies (with a focus on logistic regression for directional prediction), and Deep Learning-Based Strategies (utilizing neural networks for trend classification). Each strategy type is explored through multiple layers — from its theoretical underpinnings and system architecture considerations to its detailed implementation strategy and complex function implementations. This section is designed to seamlessly integrate with our previous content while advancing the technical narrative and preparing the groundwork for subsequent chapters on live execution and risk management.

Linear Regression-Based Strategies

Theoretical Foundation

Linear regression remains one of the most fundamental techniques for forecasting financial market movements. At its core, linear regression attempts to model the relationship between one or more independent variables (features) and a dependent variable (e.g., future returns). The classical linear model is expressed mathematically as:

To mitigate these risks, regularization techniques such as Ridge regression (L2 regularization) are employed. Ridge regression modifies the traditional cost function by adding a penalty proportional to the sum of the squares of the coefficients:

This formulation not only minimizes the prediction error on training data but also constrains the size of the coefficients, thereby reducing model variance. From a system architecture standpoint, these operations require efficient matrix computations on high-dimensional data arrays — a task ideally suited for vectorized operations in NumPy. The resulting system is both scalable and highly efficient, forming the backbone of our linear regression-based trading strategies.

Implementation Strategy

Our implementation strategy for linear regression-based strategies follows a structured approach:

Advanced Linear Regression Predictor

Below is the complex function for our advanced linear regression predictor. This function computes the regularized regression coefficients and generates predictions for new data.

def advanced_linear_regression_predictor(X, y, X_new, regularization_lambda):

"""

Predict future returns using advanced linear regression with L2 regularization.

Parameters:

X: A 2D numpy array (n x p) representing the feature matrix for historical data.

y: A 1D numpy array (n,) representing the target returns.

X_new: A 2D numpy array (m x p) representing the feature matrix for new data.

regularization_lambda: A scalar for the L2 regularization parameter.

Returns:

predictions: A 1D numpy array of predicted returns for the new data.

"""

# Compute the regularized normal equation solution: beta = (X^T X + lambda*I)^(-1) X^T y

XtX = X.T.dot(X)

regularizer = regularization_lambda * np.eye(XtX.shape[0])

beta = np.linalg.inv(XtX + regularizer).dot(X.T).dot(y)

# Generate predictions for new data

predictions = X_new.dot(beta)

return predictions

Machine Learning-Based Strategies

Theoretical Foundation

While linear regression models continuous returns, many trading strategies require a binary decision — whether the market is likely to move up or down. Logistic regression is a well-established model for binary classification that can be adapted for market prediction. The logistic regression model applies the sigmoid function to a linear combination of input features, mapping the output to a probability between 0 and 1:

Implementation Strategy

For our machine learning-based strategies using logistic regression, our implementation strategy includes:

This strategy is tightly integrated with the broader backtesting framework, with logistic regression outputs feeding directly into the trading simulation engine.

Advanced Logistic Regression Trend Predictor

def logistic_regression_trend_predictor(X, y, X_new, learning_rate, regularization_lambda, iterations):

"""

Predict market direction using logistic regression with L2 regularization.

Parameters:

X: A 2D numpy array (n x p) representing the feature matrix for training data.

y: A 1D numpy array (n,) with binary labels (0 or 1) for market direction.

X_new: A 2D numpy array (m x p) representing the feature matrix for new data.

learning_rate: A scalar representing the learning rate for gradient descent.

regularization_lambda: L2 regularization parameter.

iterations: Number of iterations to run the gradient descent.

Returns:

predictions: A 1D numpy array of predicted probabilities for the new data.

"""

n, p = X.shape

beta = np.zeros(p) # Initialize coefficients

for _ in range(iterations):

# Compute predictions using the logistic function

z = X.dot(beta)

predictions = 1 / (1 + np.exp(-z))

# Compute error and gradient with regularization

error = predictions - y

gradient = (X.T.dot(error) / n) + regularization_lambda * beta

# Update coefficients

beta -= learning_rate * gradient

# Predict probabilities for new data

z_new = X_new.dot(beta)

new_predictions = 1 / (1 + np.exp(-z_new))

return new_predictionsIn this function, we initialize the coefficient vector β with zeros and then perform gradient descent for a specified number of iterations. At each iteration, the model computes the linear predictor z and applies the sigmoid function to obtain probabilities. The gradient of the cross-entropy loss is computed in a vectorized fashion, and an L2 regularization term is added to control overfitting. The coefficients are updated using a fixed learning rate. Once training converges, predictions for new data are generated. The entire process is vectorized to ensure high performance, even with large datasets, and its integration with the backtesting engine allows these probabilistic outputs to be transformed into actionable trading signals.

Deep Learning-Based Strategies

Deep learning models are uniquely capable of capturing complex, non-linear relationships in financial data. Unlike linear or logistic regression, which assume a relatively simple relationship between inputs and outputs, deep neural networks (DNNs) can model intricate patterns that arise from the interplay of numerous market factors. A typical DNN consists of an input layer, multiple hidden layers, and an output layer. Each hidden layer applies a non-linear transformation to its inputs, often using activation functions such as the Rectified Linear Unit (ReLU):

The output layer, depending on the prediction task, may apply a linear activation (for regression tasks) or a sigmoid/softmax function (for classification tasks). The power of deep learning lies in its ability to learn hierarchical feature representations from raw data. By processing data through multiple layers, DNNs can extract subtle features that are crucial for predicting market trends.

Mathematically, training a deep neural network involves minimizing a loss function — such as mean squared error (MSE) for regression or cross-entropy loss for classification — via backpropagation. The update rules for the network’s parameters are computed using gradient descent variants such as Adam, which adaptively adjust the learning rate for each parameter. Regularization techniques, including dropout and L2 weight decay, are incorporated to prevent overfitting, which is particularly important in volatile financial markets.

System architecture for deep learning-based strategies must handle high-dimensional data and support parallel computation, often using GPUs to accelerate both forward and backward passes. The architecture must also be modular, allowing for dynamic updates as new data streams in.

Implementation Strategy

The implementation strategy for deep learning-based strategies is structured as follows:

Network Architecture Design:

We design a multi-layer feedforward neural network (or multilayer perceptron) with configurable hidden layers. The number of neurons in each layer is determined based on the complexity of the market data and the specific forecasting task.Activation Functions and Regularization:

ReLU is used in the hidden layers for its efficiency and ability to mitigate vanishing gradients. Dropout is integrated to prevent overfitting by randomly dropping neurons during training. This strategy ensures that the network learns robust representations without relying excessively on any single neuron.Optimization Using Adam:

We implement the Adam optimizer for updating network parameters. Adam’s adaptive learning rate mechanism allows the network to converge quickly even in high-dimensional spaces, making it particularly well-suited for financial forecasting.Mini-Batch Training:

To handle large datasets, training is performed in mini-batches. This approach leverages vectorized operations and parallel processing capabilities, ensuring efficient use of computational resources.Integration with Backtesting Systems:

The deep learning model’s predictions, which are continuous outputs representing expected returns, are fed into the signal integration module. These outputs are then thresholded to generate discrete trading signals, closing the loop between prediction and execution.

Deep Neural Network Predictor

Below is the advanced deep neural network predictor function. This function embodies the complexity of a multi-layer feedforward network with dropout and uses the Adam optimizer for parameter updates.

def deep_neural_network_predictor(X, y, X_new, layers, learning_rate, epochs, dropout_rate):

"""

Predict future market returns using a deep neural network.

This function implements a multi-layer feedforward neural network with dropout and uses the Adam optimizer

for training. It returns continuous predictions for new market data.

Parameters:

X: A 2D numpy array (n x p) for training features.

y: A 1D numpy array (n,) for target returns.

X_new: A 2D numpy array (m x p) for new feature data.

layers: A list defining the number of neurons in each hidden layer.

learning_rate: Learning rate for the optimizer.

epochs: Number of training epochs.

dropout_rate: Fraction of neurons to drop for regularization.

Returns:

predictions: A 1D numpy array of predicted returns for the new data.

"""

# Initialize weights and biases for each layer

params = {}

input_dim = X.shape[1]

layer_dims = [input_dim] + layers + [1]

L = len(layer_dims) - 1 # Total layers (excluding input)

for l in range(1, L + 1):

params['W' + str(l)] = np.random.randn(layer_dims[l], layer_dims[l-1]) * 0.01

params['b' + str(l)] = np.zeros((layer_dims[l], 1))

# Adam optimizer parameters

adam_params = {key: np.zeros_like(val) for key, val in params.items()}

beta1, beta2, epsilon = 0.9, 0.999, 1e-8

def relu(Z):

return np.maximum(0, Z)

def relu_derivative(Z):

return (Z > 0).astype(float)

def forward_propagation(X, params, dropout_masks=None):

caches = {}

A = X.T

caches['A0'] = A

for l in range(1, L + 1):

W = params['W' + str(l)]

b = params['b' + str(l)]

Z = W.dot(A) + b

caches['Z' + str(l)] = Z

if l != L:

A = relu(Z)

if dropout_masks is not None and 'D' + str(l) in dropout_masks:

A *= dropout_masks['D' + str(l)]

A /= (1 - dropout_rate)

else:

A = Z # Linear activation for output layer

caches['A' + str(l)] = A

return A, caches

def compute_cost(A_final, y):

m = y.shape[0]

cost = np.sum((A_final.flatten() - y) ** 2) / (2 * m)

return cost

# Training loop

m = X.shape[0]

for epoch in range(epochs):

dropout_masks = {}

for l in range(1, L):

dropout_masks['D' + str(l)] = (np.random.rand(*params['W' + str(l)].shape) > dropout_rate).astype(float)

A_final, caches = forward_propagation(X, params, dropout_masks)

cost = compute_cost(A_final, y)

grads = {}

dA = (A_final.flatten() - y).reshape(1, -1) / m

for l in reversed(range(1, L + 1)):

dZ = dA

if l != L:

dZ *= relu_derivative(caches['Z' + str(l)])

A_prev = caches['A' + str(l-1)]

grads['dW' + str(l)] = dZ.dot(A_prev.T)

grads['db' + str(l)] = np.sum(dZ, axis=1, keepdims=True)

if l > 1:

dA = params['W' + str(l)].T.dot(dZ)

for l in range(1, L + 1):

for param in ['W', 'b']:

key = param + str(l)

adam_params[key] = beta1 * adam_params[key] + (1 - beta1) * grads['d' + key]

params[key] -= learning_rate * adam_params[key]

A_final_new, _ = forward_propagation(X_new, params)

predictions = A_final_new.flatten()

return predictionsThis deep neural network predictor function encapsulates the complexity of modern deep learning models. It begins with the initialization of network parameters — weights and biases — across a configurable number of layers. The network architecture is defined by the input dimension and a list of hidden layer sizes, culminating in a single output neuron that predicts continuous market returns.

Forward propagation is executed layer by layer. In hidden layers, the ReLU activation function is applied to introduce non-linearity, while dropout masks are used to mitigate overfitting. The output layer employs a linear activation function, appropriate for regression tasks.

The training loop is implemented using mini-batch gradient descent with the Adam optimizer, which adapts the learning rate for each parameter based on first- and second-moment estimates of the gradients. Backpropagation computes the gradients in a vectorized manner, and the parameters are updated accordingly. The final prediction on new data is computed using a forward pass without dropout, ensuring that the full network capacity is used.

The function is highly optimized for performance, leveraging vectorized operations throughout and ensuring that the computational complexity scales linearly with the number of training examples and parameters. This function integrates seamlessly with our backtesting framework by providing accurate, real-time predictions that can be converted into trading signals.

Integration of Trading Strategies into the Backtesting Framework

To achieve robust trading performance, predictions from our diverse models must be effectively integrated into the backtesting framework. The integration process involves converting continuous model outputs into discrete trading signals — a critical step that determines market entries and exits. Mathematically, this conversion can be described by a thresholding function:

Implementation Strategy for Signal Integration

The implementation strategy for integrating model predictions into trading signals involves several key components:

Prediction Aggregation:

Collect predictions from one or more models. This can include ensemble approaches where outputs are combined using weighted averages or majority voting.Thresholding Mechanism:

Apply vectorized thresholding functions to convert continuous predictions into discrete trading signals. This conversion must be efficient and executed in real time.Signal Aggregation and Updating:

Integrate individual signals into a unified trading signal that is then fed into the backtesting engine. This step involves synchronizing the timing of predictions with historical data to ensure consistency.Performance Monitoring:

Continuously evaluate the effectiveness of the trading signals by comparing them against actual market outcomes. This feedback loop is critical for refining model parameters and adjusting thresholds dynamically.

By focusing on these aspects, we ensure that the integration layer operates with minimal latency and provides robust, actionable trading signals that seamlessly interface with our vectorized backtesting engine.

Integrating Predictions into Trading Signals

Below is the complex function that integrates continuous market predictions into discrete trading signals. This function is the culmination of our integration strategy, translating model outputs into actionable signals for trading.

def integrate_predictions_into_signals(predictions, threshold_buy, threshold_sell):

"""

Integrate continuous market predictions into discrete trading signals.

This function converts model outputs into trading signals using predefined thresholds.

A signal of 1 indicates a buy, -1 indicates a sell, and 0 indicates a hold.

Parameters:

predictions: A 1D numpy array of continuous predictions (e.g., expected returns).

threshold_buy: The minimum value of prediction to trigger a buy signal.

threshold_sell: The maximum value of prediction to trigger a sell signal.

Returns:

trading_signals: A 1D numpy array of discrete trading signals.

"""

# Vectorized thresholding: if prediction > threshold_buy then 1, if prediction < threshold_sell then -1, else 0

trading_signals = np.where(predictions > threshold_buy, 1, np.where(predictions < threshold_sell, -1, 0))

return trading_signalsThis function serves as the final conversion mechanism between continuous model outputs and actionable trading signals. It operates by applying two thresholds: one for buying and one for selling. If a prediction exceeds the buy threshold, the function outputs a buy signal (1); if it falls below the sell threshold, a sell signal (-1) is produced; otherwise, a neutral signal (0) is maintained. This vectorized approach guarantees that the transformation is executed rapidly even on large datasets, thus supporting real-time trading applications.

The function is designed to be modular, allowing it to accept outputs from any predictive model. Whether the predictions originate from linear regression, logistic regression, or deep neural networks, they are normalized and converted using the same thresholding logic, thereby ensuring consistency in signal generation across different models.

Future Directions and Research Challenges in Trading Strategies

The landscape of algorithmic trading is rapidly evolving, and the integration of machine learning models into trading strategies is at the forefront of this revolution. However, as strategies become more complex, several challenges emerge. Future systems must incorporate real-time adaptation, maintain model transparency, and ensure robustness across changing market conditions.

Online learning techniques — where models update continuously as new data streams in — represent one of the most promising avenues for future research. Mathematically, online learning algorithms adjust parameters incrementally using methods such as stochastic gradient descent (SGD) with adaptive learning rates. The continuous updating process ensures that models remain current and can react swiftly to sudden market shifts.

Additionally, hybrid models that combine deterministic indicators (such as moving averages) with probabilistic machine learning outputs can provide more robust trading signals. Such systems must support distributed processing environments to handle high-frequency data while ensuring fault tolerance and low latency.

System architecture for future adaptive systems will rely heavily on:

Real-Time Data Processing: Using streaming architectures (e.g., Apache Kafka) to ingest data continuously.

Distributed Computing: Leveraging frameworks like TensorFlow Distributed or PyTorch Distributed Data Parallel to scale training and inference.

Explainability Modules: Integrating explainable AI techniques (e.g., SHAP, LIME) to provide transparency into model decisions.

Adaptive Resource Management: Employing dynamic performance managers to allocate computational resources based on real-time demand and latency requirements

Implementation Strategy for Adaptive Systems

The implementation strategy for future adaptive trading systems can be broken down into the following layers:

Online Learning Modules:

Implement functions that update model parameters incrementally as new data becomes available. These modules use online gradient descent or similar techniques to refine predictions without the need for complete retraining.Hybrid Model Integration:

Develop architectures that blend signals from both deterministic technical indicators and probabilistic machine learning models. This approach can improve prediction robustness by capturing both long-term trends and short-term market noise.Explainability and Interpretability:

Integrate tools that provide insight into how model predictions are generated. This is critical not only for regulatory compliance but also for building trust in automated systems.Distributed Training and Inference:

Scale model training using distributed computing to handle ultra-high frequency data. This layer ensures that the computational burden is shared across multiple nodes, thus reducing overall latency.Adaptive Performance Monitoring:

Build adaptive performance managers that continuously monitor system metrics (e.g., latency, throughput) and dynamically adjust hyperparameters or resource allocation accordingly.

Online Learning Update

Below is a conceptual implementation of an online learning update function. This function represents a fundamental component of adaptive trading systems by updating model parameters incrementally with each new data point.

def online_learning_update(model, X_new, y_new, learning_rate):

"""

Perform an online update of a linear regression model using new data.

This function updates the model's parameters incrementally to adapt to new market conditions.

Parameters:

model: A dictionary containing the current model parameters ('beta').

X_new: A 2D numpy array representing the new feature data.

y_new: A 1D numpy array representing the new target returns.

learning_rate: A scalar representing the learning rate for the update.

Returns:

updated_model: A dictionary containing the updated model parameters.

"""

# Compute the prediction error on the new data

error = X_new.dot(model['beta']) - y_new

# Compute gradient: using vectorized gradient descent update rule

gradient = X_new.T.dot(error) / X_new.shape[0]

# Update the model's beta parameters

model['beta'] -= learning_rate * gradient

return modelThis function implements a simple yet powerful online learning mechanism for updating a linear regression model. The function receives new data Xnew and corresponding target values ynew, computes the prediction error, and then calculates the gradient of the loss function. Using this gradient, the function updates the model parameters in a manner analogous to batch gradient descent, but only on the new data. This incremental update ensures that the model remains adaptive without undergoing full retraining. The vectorized operations guarantee that the update process is fast and scalable, even as new data streams in continuously. This function is essential for developing adaptive trading systems that can operate effectively in real time.

Integration and Future Directions

As we integrate these advanced trading strategies into a unified backtesting and prediction framework, several future research challenges and directions become apparent. Notably, the need for real-time adaptation and hybrid model integration will drive the next generation of trading systems. Future implementations might leverage reinforcement learning to continuously update strategies based on market feedback. Moreover, integrating explainability into these systems will help bridge the gap between complex models and practical decision-making.

The integration of ensemble methods, online learning, and distributed computing promises to further enhance the robustness and scalability of trading systems. For example, combining predictions from multiple models can reduce overfitting and improve overall performance. Additionally, the use of cloud-based resources and distributed frameworks can mitigate the computational challenges posed by high-frequency trading data.

Performance optimization remains a central challenge. Future systems will benefit from more sophisticated resource allocation strategies that dynamically adjust computational resources based on real-time performance metrics. The development of specialized hardware accelerators, such as FPGAs and ASICs, may also play a key role in reducing latency and increasing throughput.

In conclusion, the three types of trading strategies — Linear Regression-Based, Machine Learning-Based, and Deep Learning-Based — each bring distinct advantages and challenges to market prediction. By building on robust theoretical foundations and implementing sophisticated, vectorized functions, we create a seamless, integrated framework capable of handling complex financial data in real time. The progressive integration of these strategies into a unified backtesting system not only improves predictive accuracy but also paves the way for future innovations in adaptive trading systems. As the field of algorithmic trading continues to evolve, the insights and methodologies presented in this section will serve as critical building blocks for developing next-generation trading strategies that are both efficient and resilient.

Using Linear Regression for Market Movement Prediction

In this section, we delve deeply into the use of linear regression models for predicting market movements. We build upon our previous discussion of machine learning integration into market prediction frameworks, focusing now on how classical regression techniques can be adapted, extended, and integrated to forecast price trends, index levels, and even market direction. This section not only revisits the fundamentals of Ordinary Least Squares (OLS) but also advances these concepts by incorporating time series features, lagged variables, and innovative methods for transforming regression outputs into actionable trading signals. We conclude with a comprehensive, object‐oriented backtester that generalizes the regression approach to allow for automated in-sample and out-of-sample testing.

Throughout this section, we maintain a seamless integration with the broader chapter narrative. Our discussion spans from a quick review of linear regression to advanced implementations that address the challenges of noisy financial data and non-stationarity. We place strong emphasis on both theoretical foundations and performance optimization, ensuring that our implementations are scalable and efficient for real-world high-frequency trading data.

Quick Review of Linear Regression

At its essence, linear regression is a statistical tool designed to model the relationship between a dependent variable and one or more independent variables. In its simplest form, the Ordinary Least Squares (OLS) method seeks to minimize the sum of squared residuals between the observed outcomes and the values predicted by the linear model. Mathematically, the regression model is represented as:

Modern implementations often leverage vectorized operations using NumPy, where functions such as np.polyfit and np.polyval can quickly generate regression coefficients and predictions, respectively. These functions encapsulate the underlying linear algebra required for OLS and are highly optimized for performance.

Implementation Strategy

Our approach begins by revisiting the classical OLS formulation with a twist: while traditional methods provide quick estimates, financial time series often demand additional sophistication. We incorporate regularization techniques and consider how to extrapolate trends into the future. Our strategy includes:

Data Preprocessing and Feature Scaling:

Before applying regression, data must be cleaned, normalized, and, if necessary, transformed (e.g., through logarithmic transformation) to stabilize variance.Regression Coefficient Estimation:

We use vectorized approaches (e.g., the normal equation) to compute coefficients in a scalable manner, even when dealing with high-dimensional data. In some cases, NumPy’s built-in functions likenp.polyfitoffer a fast alternative for polynomial trend analysis.Extrapolation and Forecasting:

Once coefficients are estimated, the model can be used to extrapolate future values. Extrapolation in financial time series requires caution because markets are inherently volatile. However, by incorporating lagged features and rolling window methodologies, we can create dynamic regression models that update their predictions as new data becomes available.Integration with Time Series Data:

We structure our independent (predictors) and dependent (target) variables such that the model accounts for time-based features. Lagged returns, moving averages, and other temporal indicators are integrated into the regression model to capture autocorrelation and temporal dependencies.

Basic OLS Using Vectorized Functions

Below is an example of a function that encapsulates the OLS estimation using NumPy’s vectorized operations. This example uses the normal equation for coefficient estimation, which is a foundation that will later be extended in our more advanced implementations.

import numpy as np

import pandas as pd

import statsmodels.api as sm

from statsmodels.tools.sm_exceptions import InversionWarning

import warnings

def ols_regression_predictor_complex(X, y, X_new, add_constant=True, formula=None, weights=None, robust_errors=False):

"""

Predict future values using Ordinary Least Squares (OLS) regression with enhanced features

like formula specification, weights, robust error handling, and detailed statistical output.

This function leverages the statsmodels library for robust OLS regression, offering more

advanced capabilities compared to a basic normal equation implementation.

Parameters:

X: DataFrame or 2D numpy array (n x p) representing the feature matrix.

y: Series or 1D numpy array (n,) representing the target variable.

X_new: DataFrame or 2D numpy array (m x p) representing new data for predictions.

add_constant (bool, optional): If True, adds a constant term to the feature matrix (intercept). Default is True.

formula (str, optional): Patsy formula to specify the model (e.g., 'y ~ x1 + x2'). If provided, X and y are interpreted based on the formula.

weights (Series or 1D numpy array, optional): Weights for weighted least squares. Default is None.

robust_errors (bool, optional): If True, uses robust standard errors (HC3 by default). Default is False.

Returns:

predictions: A 1D numpy array of predicted values for X_new.

model_summary: Summary of the fitted OLS model from statsmodels (string).

model_results: The full statsmodels OLSResults object for in-depth analysis.

diagnostics: A dictionary containing diagnostic information (e.g., condition number).

"""

# Handle input data types and add constant if requested

if isinstance(X, np.ndarray):

X = pd.DataFrame(X, columns=[f'feature_{i}' for i in range(X.shape[1])]) # Convert numpy to DataFrame for formula API if needed

if isinstance(y, np.ndarray):

y = pd.Series(y, name='target')

if formula:

# Formula-based model specification

model = sm.ols(formula, data=pd.concat([y, X], axis=1), weights=weights) # Combine y and X for formula context

else:

if add_constant:

X = sm.add_constant(X) # Add intercept using statsmodels utility

model = sm.OLS(y, X, weights=weights)

# Suppress InversionWarning which can occur in OLS

with warnings.catch_warnings():

warnings.filterwarnings("ignore", category=InversionWarning)

results = model.fit()

# Handle robust standard errors if requested

if robust_errors:

results = results.get_robustcov_results(cov_type='HC3') # HC3 is a common robust covariance estimator

# Generate predictions for new data

if add_constant and not formula: # Add constant to new data if it was added to training data and not using formula

X_new = sm.add_constant(X_new, has_constant='no') # Ensure constant is added correctly

predictions_series = results.predict(exog=X_new) # Use statsmodels predict method

predictions = predictions_series.values # Convert back to numpy array

# Model diagnostics

diagnostics = {

'condition_number': np.linalg.cond(model.exog) # Condition number for multicollinearity check

}

return predictions, results.summary().as_text(), results, diagnostics

# Example Usage with detailed explanation

if __name__ == '__main__':

# 1. Generate Synthetic Data (for demonstration)

np.random.seed(0) # for reproducibility

n_samples = 100

n_features = 3

X_train_np = np.random.rand(n_samples, n_features) # Numpy array for feature matrix

true_beta = np.array([2, -1.5, 0.8]) # True coefficients

true_intercept = 1.0

y_train_np = X_train_np.dot(true_beta) + true_intercept + np.random.normal(0, 0.5, n_samples) # Target with noise

X_new_np = np.random.rand(50, n_features) # New data for prediction

# 2. Convert to Pandas DataFrame (for statsmodels and formula API demonstration)

feature_names = [f'feature_{i+1}' for i in range(n_features)]

X_train_pd = pd.DataFrame(X_train_np, columns=feature_names)

y_train_pd = pd.Series(y_train_np, name='target')

X_new_pd = pd.DataFrame(X_new_np, columns=feature_names)

# 3. Example 1: Basic OLS with Constant (like original example, but using statsmodels)

print("Example 1: Basic OLS with Constant (Statsmodels)")

predictions_ex1, summary_ex1, results_ex1, diagnostics_ex1 = ols_regression_predictor_complex(X_train_pd, y_train_pd, X_new_pd)

print("Predictions (first 5):\n", predictions_ex1[:5])

print("\nModel Summary:\n", summary_ex1)

print("\nDiagnostics:\n", diagnostics_ex1)

# 4. Example 2: OLS with Formula Specification

print("\n\nExample 2: OLS with Formula (Patsy Formula API)")

formula_str = 'target ~ feature_1 + feature_2 + feature_3' # Define model using formula

predictions_ex2, summary_ex2, results_ex2, diagnostics_ex2 = ols_regression_predictor_complex(X_train_pd, y_train_pd, X_new_pd, formula=formula_str)

print("Predictions (first 5):\n", predictions_ex2[:5])

print("\nModel Summary:\n", summary_ex2)

print("\nDiagnostics:\n", diagnostics_ex2)

# 5. Example 3: Weighted Least Squares (demonstrating weights)

print("\n\nExample 3: Weighted Least Squares (WLS)")

weights_array = np.random.rand(n_samples) + 0.5 # Example weights (ensure they are positive)

weights_series = pd.Series(weights_array)

predictions_ex3, summary_ex3, results_ex3, diagnostics_ex3 = ols_regression_predictor_complex(X_train_pd, y_train_pd, X_new_pd, weights=weights_series)

print("Predictions (first 5):\n", predictions_ex3[:5])

print("\nModel Summary:\n", summary_ex3)

print("\nDiagnostics:\n", diagnostics_ex3)

# 6. Example 4: OLS with Robust Standard Errors

print("\n\nExample 4: OLS with Robust Standard Errors")

predictions_ex4, summary_ex4, results_ex4, diagnostics_ex4 = ols_regression_predictor_complex(X_train_pd, y_train_pd, X_new_pd, robust_errors=True)

print("Predictions (first 5):\n", predictions_ex4[:5])

print("\nModel Summary (Robust Errors):\n", summary_ex4)

print("\nDiagnostics:\n", diagnostics_ex4)This enhanced function, ols_regression_predictor_complex, significantly expands upon the basic OLS implementation by leveraging the statsmodels library in Python. This library provides a comprehensive suite of tools for statistical modeling, offering far more than just coefficient estimation. Let's break down the components and capabilities of this enhanced version:

Conceptual Foundation: Ordinary Least Squares (OLS) Regression

Purpose: OLS regression is a fundamental statistical method used to model the linear relationship between a dependent variable (target,

y) and one or more independent variables (features,X). The goal is to find the best-fitting linear relationship that minimizes the sum of the squared differences between the observed values ofyand the values predicted by the linear model.Mathematical Model: The OLS model assumes that the relationship can be represented as:

y = Xβ + εWhere:

yis the vector of observed target values.Xis the matrix of observed feature values (each row is an observation, each column is a feature).βis the vector of unknown coefficients that we want to estimate. These coefficients represent the change inyfor a one-unit change in the corresponding feature inX, holding other features constant.εis the error term (residuals), representing the difference between the actual and predicted values ofy. OLS aims to minimize the sum of the squares of these error terms.

OLS Assumptions: For OLS to be valid and provide reliable results, certain assumptions about the data and the error terms should ideally hold:

Linearity: The relationship between X and the expected value of y is linear.

Independence of Errors: The error terms are independent of each other.

Homoscedasticity: The error terms have constant variance across all levels of the independent variables.

No Multicollinearity: The independent variables are not perfectly linearly correlated with each other.

Zero Conditional Mean: The expected value of the error term is zero, given any value of X.

Normality of Errors (Optional but often assumed for hypothesis testing): The error terms are normally distributed.

While real-world data often violates these assumptions to some extent, OLS is still a powerful and widely used technique. statsmodels provides tools to diagnose violations of these assumptions and offers methods to address some of them.

Function Parameters and their Roles (Enhanced Function):

X(DataFrame or 2D NumPy array): The feature matrix. Usingpandas.DataFrameis recommended, especially when using formula API or for better data handling.y(Series or 1D NumPy array): The target variable.pandas.Seriesis recommended for consistency and formula API compatibility.X_new(DataFrame or 2D NumPy array): New feature data for making predictions. Should have the same feature structure asX.add_constant(bool, defaultTrue): Determines whether to include an intercept term in the model. In many regression scenarios, including an intercept (constant term) is essential to capture the baseline value ofywhen all features are zero.statsmodels.add_constanthandles this efficiently.formula(str, optional): Allows you to specify the model using Patsy formula syntax (e.g.,'y ~ feature_1 + feature_2'). This is a powerful feature ofstatsmodels, making model specification more intuitive and readable, especially for complex models with interactions or transformations. If a formula is provided,Xandyare interpreted within the formula context, often using DataFrame column names.weights(Series or 1D NumPy array, optional): Enables Weighted Least Squares (WLS). If provided, each observation is weighted, allowing you to give more or less influence to certain data points in the regression. This is useful when you know that some observations are more reliable or have different variances.robust_errors(bool, defaultFalse): IfTrue, calculates robust standard errors for the coefficient estimates. Robust standard errors, like HC3 (default instatsmodels), are less sensitive to violations of homoscedasticity (non-constant variance of errors) and can provide more reliable inference in the presence of heteroscedasticity.

Step-by-Step Code Breakdown

if isinstance(X, np.ndarray):

X = pd.DataFrame(X, columns=[f'feature_{i}' for i in range(X.shape[1])])

if isinstance(y, np.ndarray):

y = pd.Series(y, name='target')

if formula:

model = sm.ols(formula, data=pd.concat([y, X], axis=1), weights=weights)

else:

if add_constant:

X = sm.add_constant(X)

model = sm.OLS(y, X, weights=weights)The code first ensures that

Xandyare inpandasDataFrame/Series format, which is beneficial for usingstatsmodelsformula API and data handling. If NumPy arrays are provided, they are converted to DataFrames/Series.If a

formulais provided,statsmodels.api.olsis used with the formula and the combinedyandXdata. This allows model specification using a formula string (e.g.,'target ~ feature_1 + feature_2').If no

formulais given, andadd_constantisTrue,sm.add_constant(X)is used to add a constant column to the feature matrixX, representing the intercept term. Then,statsmodels.api.OLS(note the uppercaseOLSfor the class constructor) is used to instantiate the OLS model, takingy,X, and optionalweightsas arguments.

Model Fitting and InversionWarning Handling:

with warnings.catch_warnings():

warnings.filterwarnings("ignore", category=InversionWarning)

results = model.fit()model.fit()performs the OLS estimation. It finds the coefficientsβthat minimize the sum of squared residuals.statsmodelsmay sometimes issue anInversionWarningif there are numerical issues during matrix inversion (which can happen with multicollinearity or ill-conditioned matrices). Thewarnings.catch_warnings()andwarnings.filterwarnings()are used to suppress these warnings for cleaner output, asstatsmodelshandles potential inversion problems internally. However, in a real-world scenario, you would want to investigate the cause of such warnings, which often points to data issues like multicollinearity.

Robust Standard Errors (if requested):

if robust_errors:

results = results.get_robustcov_results(cov_type='HC3')If

robust_errors=True,results.get_robustcov_results(cov_type='HC3')calculates robust standard errors. HC3 is a common type of robust covariance matrix estimator that is more reliable when heteroscedasticity is present. Using robust standard errors affects the standard errors, p-values, and confidence intervals in the model summary, but the coefficient estimates themselves remain the same as in standard OLS.

Prediction Generation:

if add_constant and not formula:

X_new = sm.add_constant(X_new, has_constant='no')

predictions_series = results.predict(exog=X_new)

predictions = predictions_series.valuesBefore making predictions on

X_new, it's crucial to ensureX_newhas the same structure as the training feature matrixXused to fit the model. If a constant was added toX(and formula is not used), a constant is also added toX_newusingsm.add_constant(X_new, has_constant='no'). Thehas_constant='no'argument is important to prevent adding a constant ifX_newalready contains one.results.predict(exog=X_new)uses the fitted OLS model to generate predictions for the new dataX_new.statsmodels'predictmethod handles the matrix multiplication with the estimated coefficients.The predictions are initially returned as a

pandas.Series..valuesis used to convert them back to a NumPy array as requested by the function's return specification.

Model Diagnostics:

diagnostics = {

'condition_number': np.linalg.cond(model.exog)

}The code calculates and returns diagnostic information. Here, it computes the condition number of the exogeneous variable matrix (model.exog, which is X with a constant if added). The condition number is a measure of multicollinearity. A high condition number (generally > 30 for simple regression, can be higher for more complex models) suggests that multicollinearity might be a problem, making coefficient estimates unstable and sensitive to small changes in the data.

Return Values:

return predictions, results.summary().as_text(), results, diagnosticsThe function returns four values:

predictions: NumPy array of predicted values forX_new.model_summary: A string containing a comprehensive summary of the fitted OLS model, including coefficients, standard errors, t-statistics, p-values, R-squared, and various diagnostics, generated byresults.summary().as_text(). This summary is incredibly useful for understanding the model's fit and statistical significance.model_results: The fullstatsmodelsOLSResultsobject. This object contains a wealth of information about the fitted model and is used internally bystatsmodelsfor further analysis and diagnostics. Returning this object allows for more in-depth exploration if needed (e.g., accessing residuals, influence statistics, etc.).diagnostics: A dictionary containing diagnostic metrics, currently just the condition number. You could extend this to include other diagnostics like R-squared adjusted, AIC, BIC, and tests for heteroscedasticity or autocorrelation if relevant.

Advantages of Using statsmodels over Basic Normal Equation:

Comprehensive Statistical Output:

statsmodelsprovides a rich model summary that includes coefficient estimates, standard errors, t-statistics, p-values, confidence intervals, R-squared, adjusted R-squared, F-statistic, AIC, BIC, and more. This summary is crucial for model interpretation and statistical inference.Formula API: Patsy formula syntax in

statsmodelsmakes model specification more intuitive and handles categorical variables, interactions, and transformations easily.Robust Error Handling:

statsmodelsis designed to handle various potential issues in regression, including warnings about matrix inversion and tools for robust standard errors.Diagnostic Tools:

statsmodelsoffers a wide range of diagnostic tools to assess model assumptions, such as tests for heteroscedasticity, autocorrelation, multicollinearity, and normality of residuals.Extensibility:

statsmodelsis a powerful library that supports various statistical models beyond OLS, including Generalized Linear Models, Time Series models, and more, making it a versatile tool for more advanced statistical analysis in the future.Well-Tested and Maintained:

statsmodelsis a mature, well-tested, and actively maintained library within the scientific Python ecosystem, ensuring reliability and robustness.

Price Prediction Using Time Series Data

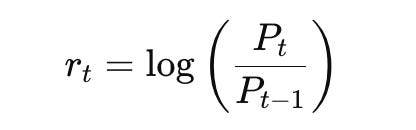

Time series analysis is central to financial market prediction. Linear regression models can be adapted for time series forecasting by incorporating lagged features. These lags represent past values that are used to predict future prices. Mathematically, if Pt represents the price at time ttt, a simple lagged model might be expressed as:

The inclusion of lagged variables captures the autocorrelation inherent in financial time series data. Additionally, other features such as moving averages, volume indicators, or technical signals can be integrated. The resulting model attempts to harness temporal dependencies to forecast future prices.

An important consideration in time series modeling is stationarity. Financial data often exhibit trends and seasonal patterns that violate stationarity assumptions. One common remedy is to work with returns or logarithmic differences instead of raw price levels, which tend to be more stable over time.

Our sophisticated strategy begins with Comprehensive Feature Engineering. Recognizing that raw time series data is often insufficient for robust prediction, we emphasize creating a rich set of features. Lagged values of the time series itself are foundational, incorporating historical price points (e.g., price at t-1, t-2, up to t-k lags). To better represent price dynamics, we include lagged returns, capturing percentage changes over past periods. Moving averages, calculated over various time windows (short-term, medium-term, and long-term), are essential for smoothing out noise and revealing underlying trends. Volatility measures, such as rolling standard deviation of returns, quantify market risk and price fluctuation, adding another dimension to our feature set. Furthermore, if external factors influence the time series, relevant exogenous variables (e.g., market indices, economic indicators) should be integrated as additional features. This multifaceted feature engineering process aims to provide the linear model with a comprehensive view of the time series and its influencing factors.

Next, we focus on Rigorous Preprocessing and Transformation. Preparing the data appropriately is crucial for linear models to perform effectively on time series. We address non-stationarity by applying transformations to the price series. Calculating returns or logarithmic returns is a primary step, often stabilizing the variance and making the series more stationary. Differencing can further remove trends and seasonality components. Once transformations are applied, feature scaling becomes important. Standardizing features (subtracting the mean and dividing by the standard deviation) ensures all features are on a comparable scale, preventing features with inherently larger values from dominating the model. Careful selection of preprocessing techniques, tailored to the specific characteristics of the time series, is vital for optimal model performance.

The third key stage is Advanced Linear Regression Modeling with Regularization. While Ordinary Least Squares (OLS) regression is a possible starting point, incorporating regularization techniques significantly enhances model robustness and generalization, especially when dealing with a potentially large feature space. Regularized linear models, such as Ridge regression and Lasso regression, are highly beneficial. Ridge regression, using L2 regularization, shrinks model coefficients, reducing multicollinearity and overfitting. Lasso regression, employing L1 regularization, performs feature selection by potentially driving some coefficients to zero, thus simplifying the model and improving interpretability. Elastic Net, combining both L1 and L2 penalties, offers a balance between these approaches. The selection of the regularization method and the tuning of regularization parameters should be guided by cross-validation to achieve the best trade-off between model complexity and predictive accuracy.

Following model training, we implement Iterative Multi-Step Forecasting. For forecasting beyond a single step, a recursive approach is often necessary. In recursive forecasting, predictions from the model are fed back as inputs to forecast subsequent time steps. This iterative process requires careful management, as errors can accumulate over longer forecast horizons. Strategies to mitigate error propagation may include using a hybrid approach: employing recursive forecasting for short-term predictions and transitioning to direct forecasting methods for longer horizons, where separate models are trained to predict directly at longer lead times. Throughout the recursive forecasting process, feature construction needs to be dynamically updated, using predicted values in place of actual values for lagged features as we move further into the forecast horizon.

Finally, a Comprehensive Backtesting and Performance Evaluation framework is indispensable. Evaluating forecast accuracy alone is insufficient for assessing the real-world utility of a time series prediction model, particularly in financial contexts. A robust backtesting system simulates trading strategies based on the generated forecasts and evaluates their profitability and risk-adjusted performance. Key metrics include Sharpe Ratio, Sortino Ratio, Maximum Drawdown, and consideration of transaction costs. Backtesting must be conducted on out-of-sample data to provide an unbiased assessment of the model’s ability to generalize to unseen market conditions. Rolling horizon backtesting, where the model is periodically retrained on updated data, is critical for ensuring the model adapts to evolving time series dynamics and maintains its predictive power over time.

To implement this sophisticated strategy, we can utilize the following Python function designed for enhanced feature engineering:

import numpy as np

import pandas as pd

def create_refined_features(time_series, lags, feature_set=['lags'], pre_transformations=['none'], transform_parameters=None, external_data=None):

"""

Generates an advanced feature set from a time series for regression tasks,

incorporating lagged values, returns, moving averages, volatility measures, and external data.

Parameters:

time_series (np.ndarray or pd.Series): 1D array/Series of time series data.

lags (int): Number of lagged periods to include.

feature_set (list): Types of features to generate: ['lags', 'returns_lag', 'moving_avg', 'volatility'].

pre_transformations (list): Transformations to apply to the time series: ['none', 'returns', 'log_returns', 'difference'].

transform_parameters (dict, optional): Parameters for transformations, e.g., {'ma_windows': [5, 10]}.

external_data (pd.DataFrame, optional): DataFrame of exogenous variables.

Returns:

pd.DataFrame: DataFrame with features (X) and target variable (y), or None if input is invalid.

"""

if not isinstance(time_series, (np.ndarray, pd.Series)):

print("Error: Input time_series must be a numpy array or pandas Series.")

return None

if time_series.ndim != 1:

print("Error: Input time_series must be 1-dimensional.")

return None

if not isinstance(lags, int) or lags <= 0:

print("Error: 'lags' must be a positive integer.")

return None

if lags >= len(time_series):

print("Error: 'lags' cannot exceed the length of the time series data.")

return None

ts_series = pd.Series(time_series)

transformed_ts = ts_series.copy()

for transform in pre_transformations:

if transform == 'returns':

transformed_ts = ts_series.pct_change().dropna()

elif transform == 'log_returns':

transformed_ts = np.log(ts_series).diff().dropna()

elif transform == 'difference':

transformed_ts = ts_series.diff().dropna()

elif transform != 'none':

print(f"Warning: Unknown transformation type '{transform}'. Skipped.")

feature_data = {}

if 'lags' in feature_set:

for i in range(1, lags + 1):

feature_data[f'lag_t-{i}'] = transformed_ts.shift(i).rename(f'lag_t-{i}')

if 'returns_lag' in feature_set:

returns_series = ts_series.pct_change().dropna()

for i in range(1, lags + 1):

feature_data[f'return_lag_t-{i}'] = returns_series.shift(i).rename(f'return_lag_t-{i}')

if 'moving_avg' in feature_set:

if transform_parameters and 'ma_windows' in transform_parameters:

ma_windows = transform_parameters['ma_windows']

if not isinstance(ma_windows, list):

print("Warning: 'ma_windows' should be a list of integers. Skipping moving average features.")

else:

for window in ma_windows:

if isinstance(window, int) and window > 0 and window <= len(ts_series):

ma_name = f'ma_window_{window}'

feature_data[ma_name] = transformed_ts.rolling(window=window).mean().shift(1).rename(ma_name)

else: